PNC Bank 2010 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

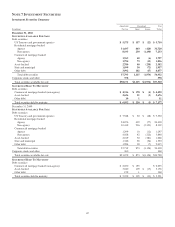

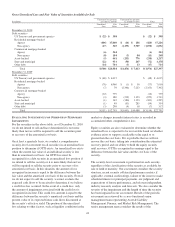

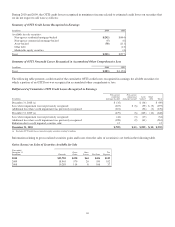

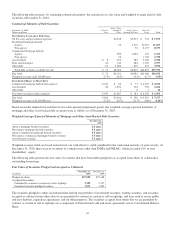

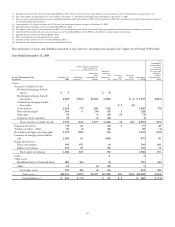

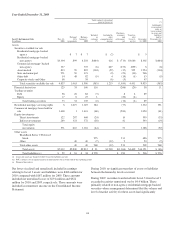

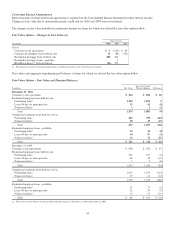

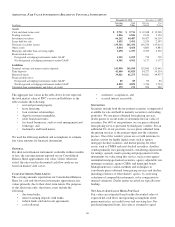

|

|

N

OTE

8F

AIR

V

ALUE

F

AIR

V

ALUE

M

EASUREMENT

Fair value is defined in GAAP as the price that would be

received to sell an asset or the price paid to transfer a liability

on the measurement date. The standard focuses on the exit

price in the principal or most advantageous market for the

asset or liability in an orderly transaction between market

participants. GAAP establishes a fair value reporting

hierarchy to maximize the use of observable inputs when

measuring fair value and defines the three levels of inputs as

noted below.

Level 1

Quoted prices in active markets for identical assets or

liabilities. Level 1 assets and liabilities may include debt

securities, equity securities and listed derivative contracts that

are traded in an active exchange market and certain US

government agency securities that are actively traded in

over-the-counter markets.

Level 2

Observable inputs other than Level 1 such as: quoted prices

for similar assets or liabilities in active markets, quoted prices

for identical or similar assets or liabilities in markets that are

not active, or other inputs that are observable or can be

corroborated to observable market data for substantially the

full term of the asset or liability. Level 2 assets and liabilities

may include debt securities, equity securities and listed

derivative contracts with quoted prices that are traded in

markets that are not active, and certain debt and equity

securities and over-the-counter derivative contracts whose fair

value is determined using a pricing model without significant

unobservable inputs. This category generally includes agency

residential and commercial mortgage-backed debt securities,

asset-backed securities, corporate debt securities, residential

mortgage loans held for sale, and derivative contracts.

Level 3

Unobservable inputs that are supported by minimal or no

market activity and that are significant to the fair value of the

assets or liabilities. Level 3 assets and liabilities may include

financial instruments whose value is determined using pricing

models with internally developed assumptions, discounted

cash flow methodologies, or similar techniques, as well as

instruments for which the determination of fair value requires

significant management judgment or estimation. This category

generally includes certain available for sale and trading

securities, commercial mortgage loans held for sale, private

equity investments, residential mortgage servicing rights,

BlackRock Series C Preferred Stock and certain financial

derivative contracts. The available for sale and trading

securities within Level 3 include non-agency residential

mortgage-backed securities, auction rate securities, certain

private-issuer asset-backed securities and corporate debt

securities. Nonrecurring items, primarily certain nonaccrual

and other loans held for sale, commercial mortgage servicing

rights, equity investments and other assets are also included in

this category.

We characterize active markets as those where transaction

volumes are sufficient to provide objective pricing

information, with reasonably narrow bid/ask spreads and

where dealer quotes received do not vary widely and are based

on current information. Inactive markets are typically

characterized by low transaction volumes, price quotations

which vary substantially among market participants or are not

based on current information, wide bid/ask spreads, a

significant increase in implied liquidity risk premiums, yields,

or performance indicators for observed transactions or quoted

prices compared to historical periods, a significant decline or

absence of a market for new issuance, or any combination of

the above factors. We also consider nonperformance risks

including credit risk as part of our valuation methodology for

all assets and liabilities measured at fair value.

Any models used to determine fair values or to validate dealer

quotes based on the descriptions below are subject to review

and independent testing as part of our model validation and

internal control testing processes. Our Model Validation

Committee tests significant models on at least an annual basis.

In addition, we have teams, independent of the traders, verify

marks and assumptions used for valuations at each period end.

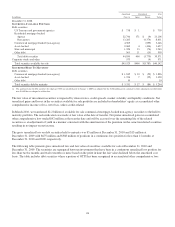

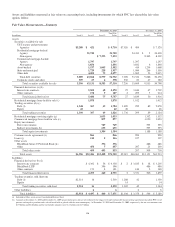

Securities Available for Sale and Trading Securities

Securities accounted for at fair value include both the

available for sale and trading portfolios. We use prices

obtained from pricing services, dealer quotes or recent trades

to determine the fair value of securities. For 59% of our

positions, we use prices obtained from pricing services

provided by third party vendors. For an additional 9% of our

positions, we use prices obtained from the pricing services as

the primary input into the valuation process. One of the

vendors’ prices are set with reference to market activity for

highly liquid assets such as agency mortgage-backed

securities, and matrix pricing for other assets, such as CMBS

and asset-backed securities. Another vendor primarily uses

pricing models considering adjustments for ratings, spreads,

matrix pricing and prepayments for the instruments we value

using this service, such as non-agency residential mortgage-

backed securities, agency adjustable rate mortgage securities,

agency CMOs and municipal bonds. Management uses

various methods and techniques to corroborate prices obtained

from pricing services and dealers, including reference to other

dealer or market quotes, by reviewing valuations of

comparable instruments, or by comparison to internal

valuations. Dealer quotes received are typically non-binding.

In circumstances where relevant market prices are limited or

unavailable, valuations may require significant management

judgments or adjustments to determine fair value. In these

cases, the securities are classified as Level 3.

The valuation techniques used for securities classified as

Level 3 include using a discounted cash flow approach or, in

133