PNC Bank 2010 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

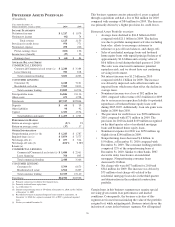

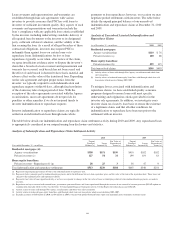

|

|

R

ESIDENTIAL

M

ORTGAGE

B

ANKING

(Unaudited)

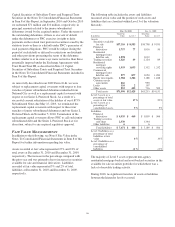

Year ended December 31

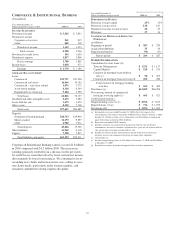

Dollars in millions, except as noted 2010 2009

I

NCOME

S

TATEMENT

Net interest income $ 267 $ 332

Noninterest income

Loan servicing revenue

Servicing fees 242 222

Net MSR hedging gains 245 355

Loan sales revenue 231 435

Other 18 (16)

Total noninterest income 736 996

Total revenue 1,003 1,328

Provision for (recoveries of) credit losses 5(4)

Noninterest expense 565 632

Pretax earnings 433 700

Income taxes 158 265

Earnings $ 275 $ 435

A

VERAGE

B

ALANCE

S

HEET

Portfolio loans $2,649 $1,957

Loans held for sale 1,322 2,204

Mortgage servicing rights (MSR) 1,017 1,297

Other assets 4,259 2,962

Total assets $9,247 $8,420

Deposits $2,716 $4,135

Borrowings and other liabilities 2,823 2,924

Capital 1,200 1,359

Total liabilities and equity $6,739 $8,418

P

ERFORMANCE

R

ATIOS

Return on average capital 23% 32%

Return on average assets 2.97 5.17

Noninterest income to total revenue 73 75

Efficiency 56 48

R

ESIDENTIAL

M

ORTGAGE

S

ERVICING

P

ORTFOLIO

(in billions)

Beginning of period $ 145 $ 173

Acquisitions/additions 10 20

Repayments/transfers (30) (40)

Servicing sale (8)

End of period $ 125 $ 145

Servicing portfolio statistics: (a)

Fixed rate 89% 88%

Adjustable rate/balloon 11% 12%

Weighted average interest rate 5.62% 5.82%

MSR capitalized value (in billions) $ 1.0 $ 1.3

MSR capitalization value (in basis points) 82 91

Weighted average servicing fee (in basis

points) 30 30

O

THER

I

NFORMATION

Loan origination volume (in billions) $ 10.5 $ 19.1

Percentage of originations represented by:

Agency and government programs 99% 97%

Refinance volume 74% 72%

Total nonperforming assets (a) (b) $ 349 $ 370

Impaired loans (a) (c) $ 161 $ 369

(a) As of December 31.

(b) Includes nonperforming loans of $109 million at December 31, 2010 and $215

million at December 31, 2009.

(c) Recorded investment of purchased impaired loans related to acquisitions.

Residential Mortgage Banking earned $275 million for 2010

compared with $435 million in 2009. The decline in earnings

was driven by a decrease in loan sales revenue from lower

origination volumes and lower net hedging gains on mortgage

servicing rights.

Residential Mortgage Banking overview:

• Total loan originations were $10.5 billion for 2010

compared with $19.1 billion for 2009. Lower

mortgage rates in the first half of 2009 resulted in

higher loan origination volumes. Loans continued to

be primarily originated through direct channels under

FNMA, FHLMC and FHA/Veterans’ Administration

(VA) agency guidelines.

• Investors may request PNC to indemnify them

against losses on certain loans or to repurchase loans

that they believe do not comply with applicable

representations. At December 31, 2010, the liability

for estimated losses on loan indemnification and

repurchase claims for the Residential Mortgage

Banking business segment was $144 million

compared with $229 million at December 31, 2009.

See the Recourse and Repurchase Obligations section

of this Item 7 and Note 23 Commitments and

Guarantees in the Notes To Consolidated Financial

Statements included in Item 8 of this Report for

additional information.

• Residential mortgage loans serviced for others totaled

$125 billion at December 31, 2010 compared with

$145 billion at December 31, 2009. Payoffs

continued to outpace new direct loan origination

volume during 2010.

• Net interest income was $267 million for 2010

compared with $332 million for 2009. The decrease

resulted from lower escrow deposit balances and

residential mortgage loans held for sale.

• Noninterest income was $736 million in 2010

compared with $996 million in 2009. The decline

was due to reduced loan sales revenue, net of

additional repurchase reserves, reflective of strong

loan origination refinance volume in 2009, and lower

net hedging gains on mortgage servicing rights.

• Noninterest expense declined to $565 million in 2010

compared with $632 million in 2009 as lower loan

origination volume drove a reduction in expense,

partially offset by higher foreclosure costs in 2010.

• The fair value of mortgage servicing rights was $1.0

billion at December 31, 2010 compared with $1.3

billion at December 31, 2009. The decline in fair

value resulted from lower mortgage rates at

December 31, 2010 and a smaller servicing portfolio.

56