PNC Bank 2010 Annual Report Download - page 123

Download and view the complete annual report

Please find page 123 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

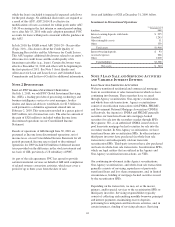

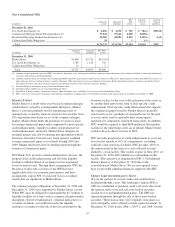

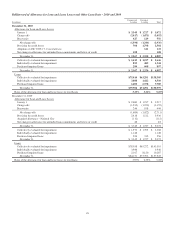

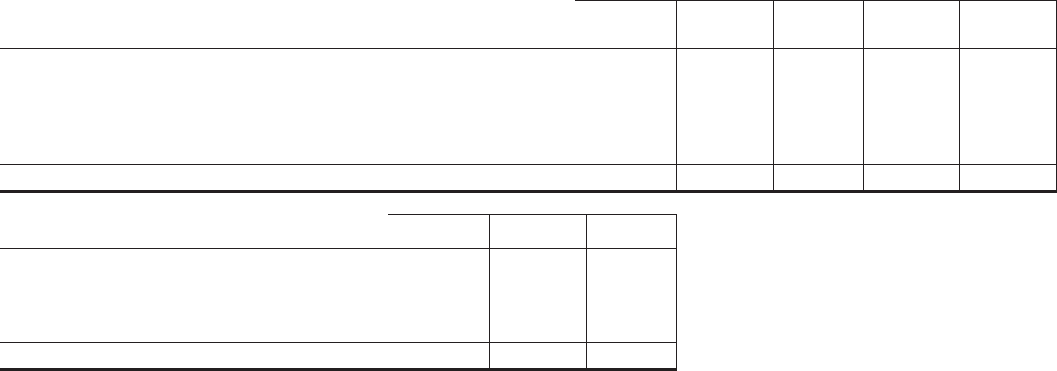

Non-Consolidated VIEs

In millions

Aggregate

Assets

Aggregate

Liabilities

PNC

Risk

of Loss

Carrying

Value of

Assets

Carrying

Value of

Liabilities

December 31, 2010

Tax Credit Investments (a) $ 4,086 $ 2,258 $ 782 $ 782(c) $301(d)

Commercial Mortgage-Backed Securitizations (b) 79,142 79,142 2,068 2,068(e)

Residential Mortgage-Backed Securitizations (b) 42,986 42,986 2,203 2,199(e) 4 (d)

Collateralized Debt Obligations 18 1 1 (c)

Total $126,232 $124,386 $5,054 $5,050 $305

In millions

Aggregate

Assets

Aggregate

Liabilities

PNC Risk

of Loss

December 31, 2009

Market Street $3,698 $3,718 $6,155(f)

Tax Credit Investments (a) 1,786 1,156 743

Collateralized Debt Obligations 23 2

Total $5,507 $4,874 $6,900

(a) Amounts reported primarily represent LIHTC investments. Aggregate assets and aggregate liabilities represent estimated balances due to limited availability of financial information

associated with certain acquired partnerships.

(b) Amounts reported reflect involvement with securitization SPEs where PNC transferred to and/or services loans for a SPE and we hold securities issued by that SPE. We also invest in

other mortgage and asset-backed securities issued by third-party VIEs with which we have no continuing involvement. Further information on these securities is included in Note 7

Investment Securities and values disclosed represent our maximum exposure to loss for those securities’ holdings.

(c) Included in Equity investments on our Consolidated Balance Sheet.

(d) Included in Other liabilities on our Consolidated Balance Sheet.

(e) Included in Trading securities, Investment securities, Other intangible assets, and Other assets on our Consolidated Balance Sheet.

(f) PNC’s risk of loss consisted of off-balance sheet liquidity commitments to Market Street of $5.6 billion and other credit enhancements of $.6 billion at December 31, 2009.

M

ARKET

S

TREET

Market Street is a multi-seller asset-backed commercial paper

conduit that is owned by an independent third party. Market

Street’s activities primarily involve purchasing assets or

making loans secured by interests in pools of receivables from

US corporations that desire access to the commercial paper

market. Market Street funds the purchases of assets or loans

by issuing commercial paper and is supported by pool-specific

credit enhancements, liquidity facilities and program-level

credit enhancement. Generally, Market Street mitigates its

potential interest rate risk by entering into agreements with its

borrowers that reflect interest rates based upon its weighted

average commercial paper cost of funds. During 2010 and

2009, Market Street met all of its funding needs through the

issuance of commercial paper.

PNC Bank, N.A. provides certain administrative services, the

program-level credit enhancement and all of the liquidity

facilities to Market Street in exchange for fees negotiated

based on market rates. Through these arrangements, PNC has

the power to direct the activities of the SPE that most

significantly affect its economic performance and these

arrangements expose PNC to expected losses or residual

returns that are significant to Market Street.

The commercial paper obligations at December 31, 2010 and

December 31, 2009 were supported by Market Street’s assets.

While PNC may be obligated to fund under the $5.7 billion of

liquidity facilities for events such as commercial paper market

disruptions, borrower bankruptcies, collateral deficiencies or

covenant violations, our credit risk under the liquidity

facilities is secondary to the risk of first loss provided by the

borrower such as by the over-collateralization of the assets or

by another third party in the form of deal-specific credit

enhancement. Deal-specific credit enhancement that supports

the commercial paper issued by Market Street is generally

structured to cover a multiple of expected losses for the pool

of assets and is sized to generally meet rating agency

standards for comparably structured transactions. In addition,

PNC would be required to fund $658 million of the liquidity

facilities if the underlying assets are in default. Market Street

creditors have no direct recourse to PNC.

PNC provides program-level credit enhancement to cover net

losses in the amount of 10% of commitments, excluding

explicitly rated AAA/Aaa facilities. PNC provides 100% of

the enhancement in the form of a cash collateral account

funded by a loan facility. This facility expires in June 2015. At

December 31, 2010, $601 million was outstanding on this

facility. This amount was eliminated in PNC’s Consolidated

Balance Sheet as of December 31, 2010 due to the

consolidation of Market Street. We are not required to nor

have we provided additional financial support to the SPE.

C

REDIT

C

ARD

S

ECURITIZATION

T

RUST

We are the sponsor of several credit card securitizations

facilitated through a trust. This bankruptcy-remote SPE or

VIE was established to purchase credit card receivables from

the sponsor and to issue and sell asset-backed securities

created by it to independent third-parties. The SPE was

financed primarily through the sale of these asset-backed

securities. These transactions were originally structured as a

form of liquidity and to afford favorable capital treatment. At

December 31, 2010, Series 2006-1, 2007-1, and 2008-3 issued

115