PNC Bank 2010 Annual Report Download - page 132

Download and view the complete annual report

Please find page 132 of the 2010 PNC Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

|

|

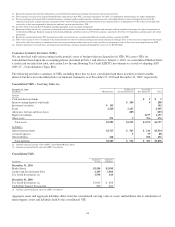

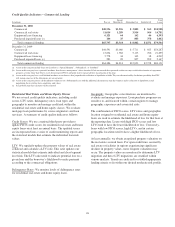

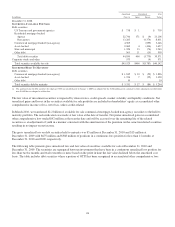

Credit Quality Indicators – Commercial Lending

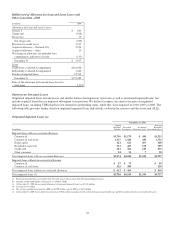

In millions Pass (a)

Special

Mention (b) Substandard (c) Doubtful (d)

Total

Loans

December 31, 2010

Commercial $48,556 $1,926 $ 3,883 $ 563 $54,928

Commercial real estate 11,014 1,289 3,914 564 16,781

Equipment lease financing 6,121 64 162 46 6,393

Purchased impaired loans (e) 106 35 883 378 1,402

Total commercial lending $65,797 $3,314 $ 8,842 $1,551 $79,504

December 31, 2009

Commercial $44,591 $3,060 $ 5,711 $ 925 $54,287

Commercial real estate 13,834 1,782 5,113 766 21,495

Equipment lease financing 5,778 44 342 38 6,202

Purchased impaired loans (e) 283 28 857 999 2,167

Total commercial lending $64,486 $4,914 $12,023 $2,728 $84,151

(a) Assets in this category include loans not classified as “Special Mention”, “Substandard”, or “Doubtful.”

(b) Assets in this category have a potential weakness that deserves management’s close attention. If left uncorrected these potential weaknesses may result in deterioration of repayment

prospects at some future date. These assets do not expose PNC to sufficient risk to warrant adverse classification at this time.

(c) Assets in this category have a well-defined weakness or weaknesses that jeopardize the collection or liquidation of debt. They are characterized by the distinct possibility that PNC

will sustain some loss if the deficiencies are not corrected.

(d) Assets in this category possess all the inherent weaknesses of a Substandard asset with the additional characteristics that the weakness makes collection or liquidation in full

improbable due to existing facts, conditions, and values.

(e) It is probable that these amounts will be collected.

Residential Real Estate and Home Equity Classes

We use several credit quality indicators, including credit

scores, LTV ratios, delinquency rates, loan types and

geography to monitor and manage credit risk within the

residential real estate and home equity classes. We evaluate

mortgage loan performance by source originators and loan

servicers. A summary of credit quality indicators follows:

Credit Scores: We use a national third-party provider to

update FICO credit scores for residential real estate and home

equity loans on at least an annual basis. The updated scores

are incorporated into a series of credit monitoring reports and

the statistical models that estimate the individual loan risk

values.

LTV: We regularly update the property values of real estate

collateral and calculate a LTV ratio. This ratio updates our

statistical models that estimate individual and class/segment

level risk. The LTV ratio tends to indicate potential loss on a

given loan and the borrower’s likelihood to make payment

according to the contractual obligations.

Delinquency Rates: We monitor levels of delinquency rates

for residential real estate and home equity loans.

Geography: Geographic concentrations are monitored to

evaluate and manage exposures. Loan purchase programs are

sensitive to, and focused within, certain regions to manage

geographic exposures and associated risks.

The combination of FICO scores, LTV ratios and geographic

location assigned to residential real estate and home equity

loans are used to estimate the likelihood of loss for that loan at

the reporting date. Loans with high FICO scores and low

LTVs tend to have the lower likelihood of loss. Conversely,

loans with low FICO scores, high LTVs, and in certain

geographic locations tend to have a higher likelihood of loss.

At least annually, we obtain an updated property valuation on

the real estate secured loans. For open credit lines secured by

real estate or facilities in regions experiencing significant

declines in property values, more frequent valuations may

occur. The property values are monitored to determine LTV

migration and those LTV migrations are stratified within

various markets. Trends are analyzed to establish appropriate

lending criteria to fit within our desired moderate risk profile.

124