ICICI Bank 2012 Annual Report Download - page 177

Download and view the complete annual report

Please find page 177 of the 2012 ICICI Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

172 -

173

173 -

174

174 -

175

175 -

176

176 -

177

177 -

178

178 -

179

179 -

180

180 -

181

181 -

182

182 -

183

183 -

184

184 -

185

185 -

186

186 -

187

187 -

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

F99

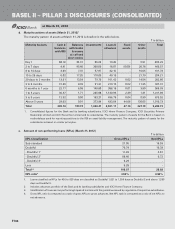

The capital ratios of the Bank and its banking subsidiaries at March 31, 2012 are as follows:

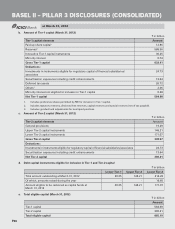

Capital ratios ICICI Bank Ltd

(consolidated)1

ICICI Bank Ltd

(standalone)1

ICICI Bank UK

PLC1

ICICI Bank

Canada1

ICICI Bank

Eurasia LLC1,2

Tier-1 capital ratio 12.80% 12.68% 21.18% 29.85% n.a.

Total capital ratio 19.60% 18.52% 32.42% 31.69% 27.71%

1. Computed as per capital adequacy guidelines issued by regulators of respective jurisdictions.

2. Tier-1 capital ratio is not required to be reported in line with regulatory norms stipulated by the Central Bank of Russia.

4. RISK MANAGEMENT FRAMEWORK

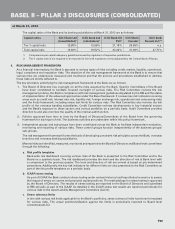

As a financial intermediary, the Bank is exposed to various types of risks including credit, market, liquidity, operational,

legal, compliance and reputation risks. The objective of the risk management framework at the Bank is to ensure that

various risks are understood, measured and monitored and that the policies and procedures established to address

these risks are strictly adhered to.

The key principles underlying the risk management framework at the Bank are as follows:

1. The Board of Directors has oversight on all the risks assumed by the Bank. Specific Committees of the Board

have been constituted to facilitate focused oversight of various risks. The Risk Committee reviews the risk

management policies, the Bank’s compliance with risk management guidelines stipulated by the RBI and the status

of implementation of the advanced approaches under the Basel framework. It reviews key risk indicators covering

areas such as credit risk, interest rate risk, liquidity risk, foreign exchange risk, operational and outsourcing risks

and the limits framework, including stress test limits for various risks. The Risk Committee also reviews the risk

profile of the overseas banking subsidiaries. Credit Committee reviews developments in key industrial sectors

and the Bank’s exposure to these sectors and various portfolios on a periodic basis. Audit Committee provides

direction to and also monitors the quality of the internal audit function.

2. Policies approved from time to time by the Board of Directors/Committees of the Board form the governing

framework for each type of risk. The business activities are undertaken within this policy framework.

3. Independent groups and sub-groups have been constituted across the Bank to facilitate independent evaluation,

monitoring and reporting of various risks. These control groups function independently of the business groups/

sub-groups.

The risk management framework forms the basis of developing consistent risk principles across the Bank, overseas

branches and overseas banking subsidiaries.

Material risks are identified, measured, monitored and reported to the Board of Directors and Board level committees

through the following:

a. Risk profile templates

Bank-wide risk dashboard covering various risks of the Bank is presented to the Risk Committee and to the

Board on a quarterly basis. The risk dashboard provides the level and the direction of risk at Bank level with

a comparison to the previous quarter. The level and direction of risk are arrived at based on pre-determined

parameters. Additionally, the key risk indicators for different risks are also presented to the Risk Committee as

part of the risk profile templates on a periodic basis.

b. ICAAP/stress testing

As part of ICAAP, the Bank conducts stress testing under various historical and hypothetical scenarios to assess

the impact of stress on current and projected capital positions. The methodology for stress testing is approved

by the Board of Directors. The results of stress testing are reported to the Board of Directors and submitted

to RBI annually as part of the ICAAP. As detailed in the ICAAP, stress test results are reported periodically for

various risks to the Asset Liability Management Committee (ALCO).

c. Stress tolerance limits

In line with various risk limits applicable for the Bank’s portfolios, stress tolerance limits have been formulated

for various risks. The actual position/utilisation against the limits is periodically reported to Board level

committees/ALCO.

BASEL II – PILLAR 3 DISCLOSURES (CONSOLIDATED)

at March 31, 2012