Volvo 2011 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2011 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

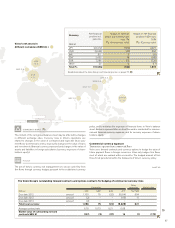

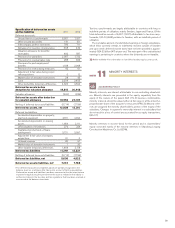

CREDIT RISKS

Credit risks are defined as the risk that Volvo does not receive payment for

recognized accounts receivable and customer-financing receivables

(commercial credit risk), that Volvo’s investments are unable to be realized

(financial credit risk) and that potential profit is not realized due to the

counterparty not fulfilling its part of the contract when using derivative

instruments (financial counterparty risk).

POLICY

The objective of the Volvo Group Credit Policy is to define and measure

the credit exposure and control the risk of losses deriving from credits to

customers, credits to suppliers, counter party risks and Customer Dealer

Financing activities.

Commercial credit risk

Volvo’s credit granting is steered by Group-wide policies and customer-

classification rules. The credit portfolio should contain a sound distribu-

tion among different customer categories and industries. The credit risks

are managed through active credit monitoring, follow-up routines and,

where applicable, product repossession. Moreover, regular monitoring

ensures that the necessary allowances are made for incurred losses on

doubtful receivables. In Notes 15 and 16, ageing analyses are presented

of customer finance receivables overdue and accounts receivables over-

due in relation to the reserves made.

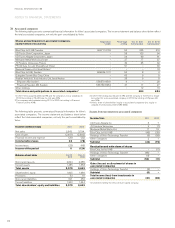

The credit portfolio of Volvo’s customer-financing operations amounted

at December 31, 2011, to approximately net SEK 79 billion (73). The credit

risk of this portfolio is distributed over a large number of retail customers

and dealers. Collaterals are provided in the form of the financed products.

In the credit granting Volvo strives for a balance between risk exposure

and expected return.

Read more about Volvo’s credit risk in the customer-financing operation in

Note 15.

Financial credit risk

The Volvo Group’s financial assets are largely managed by Volvo Treasury

and invested in the money and capital markets. All investments must meet

the requirements of low credit risk and high liquidity. According to Volvo’s

credit policy, counterparties for investments and derivative transactions

should have a rating of A or better from one of the well-established credit

rating institutions.

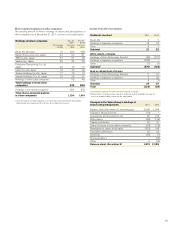

Financial counterparty risk

The use of derivatives involves a counterparty risk, in that a potential gain

will not be realized if the counterparty fails to fulfill its part of the contract.

To reduce the exposure, master netting agreements are signed, wherever

possible, with the counterparty in question. Counterparty risk exposure for

futures contracts is limited through daily or monthly cash transfers cor-

responding to the value change of open contracts. The estimated gross

exposure to counterparty risk relating to futures, interest-rate swaps and

interest-rate forward contracts, options and commodities contracts

amounted at December 31, 2011, to 281 (331), 4,024 (3,539 ), 284 (190)

and 68 (168).

CREDIT RISKS

89