Volvo 2011 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2011 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

|

|

Consolidated financial statements

Principles for consolidation

The consolidated financial statements have been prepared in accordance

with the principles set forth in IAS 27, Consolidated and Separate Financial

Statements. Accordingly, intra-Group transactions and gains on transac-

tions with associated companies are eliminated. The consolidated finan-

cial statements comprise the Parent Company, subsidiaries, joint ventures

and associated companies.

– Subsidiaries are defined as companies in which Volvo holds more than

50% of the voting rights or in which Volvo otherwise has a controlling

interest.

– Joint ventures are companies over which Volvo has joint control together

with one or more external parties. Joint ventures are recognized using

the proportionate method of consolidation.

– Associated companies are companies in which Volvo has a significant

influence, which is normally when Volvo’s holdings correspond to at

least 20% but less than 50% of the voting rights. Holdings in associated

companies are recognized in accordance with the equity method.

Translation to Swedish kronor when consolidating companies using

foreign currencies

AB Volvo’s functional currency is the Swedish krona (SEK). The functional

currency of each Volvo Group company is determined based on the pri-

mary economic environment in which it operates. The primary economic

environment is normally the one in which the company primarily generates

and expends cash. In most cases, the functional currency is the currency

of the country where the company is located. AB Volvo’s and the Volvo

Group’s presentation currency is SEK. In preparing the consolidated

financial statements, all items in the income statements of foreign sub-

sidiaries and joint ventures (except for subsidiaries in hyperinflationary

economies) are translated to SEK at monthly exchange rates. All balance-

sheet items are translated at exchange rates at the respective year-ends

(closing rate). The differences in consolidated shareholders’ equity, arising

from variations between closing rates for the current and preceding year

are charged or credited directly to other comprehensive income as a separate

component.

The accumulated translation difference related to a certain subsidiary,

joint venture or associated company is reversed to profit or loss as a part

of the gain/loss arising from the divestment or liquidation of such a company.

IAS 29, Financial Reporting in Hyperinflationary Economies, is applied

to financial statements of subsidiaries operating in hyperinflationary

economies. Volvo’s method of recognition is based on cost. Translation

differences due to inflation are charged against earnings for the year. Cur-

rently, Volvo has no subsidiaries with a functional currency that could be

considered a hyperinflationary currency.

Receivables and liabilities in foreign currency

Receivables and liabilities in foreign currency are measured at closing

rates. Translation differences on operating assets and liabilities are rec-

ognized in operating income, while translation differences arising in finan-

cial assets and liabilities are charged to other financial income and

expenses. Financial assets and liabilities are defined as items included in

the net financial position of the Volvo Group (see Definitions at the end of

this report). Derivative financial instruments used for hedging of exchange

and interest risks are recognized at fair value. Gains on exchange rates

are recognized as receivables and losses on exchange rates are recog-

nized as liabilities. Depending on the lifetime of the financial instrument,

the item is recognized as current or non-current in the balance sheet.

Exchange rate differences on loans and other financial instruments in

foreign currency, which are used to hedge net assets in foreign subsidiaries

and associated companies, are offset against translation differences in

the shareholders’ equity of the respective companies. Exchange-rate

gains and losses on assets and liabilities in foreign currencies, both on

payments during the year and on measurements at year-end, impact profit

or loss in the year in which they are incurred. The more important exchange

rates applied are shown in the table.

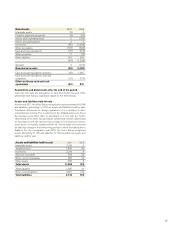

Exchange rates Average rate Closingrate

Country Currency 2011 2010 2011 2010

Brazil BRL 3.8850 4.0925 3.7109 4.0560

Canada CAD 6.5694 6.9973 6.7808 6.8085

China CNY 1.0057 1.0643 1.0998 1.0300

Denmark DKK 1.2137 1.2823 1.2044 1.2086

Euro zone EUR 9.0430 9.5502 8.9540 9.0113

Great Britain GBP 10.4179 11.1319 10.6831 10.5538

Japan JPY 0.0817 0.0823 0.0892 0.0835

Norway NOK 1.1596 1.1926 1.1515 1.1530

South Korea KRW 0.0059 0.0062 0.0060 0.0060

United States USD 6.4982 7.2060 6.9247 6.8038

New accounting principles for 2011

None of the new accounting principles or interpretations that came into

effect as of January 1, 2011 has had any significant impact on the Volvo

Group’s financial statements.

New accounting principles for 2012 and later

When preparing the consolidated financial statements as of December

31, 2011, a number of standards and interpretations has been published,

but has not yet become effective. The following is a preliminary assessment

of the effect that the implementation of these standards and statements

could have on the Volvo Group’s financial statements.

Amendment to IAS 19 Employee benefits*

As from January 1, 2013 the amendment to IAS 19, Employee benefits

will become effective. The revised standard is applied retrospectively, and

hence the closing balance for 2011 will be adjusted in accordance with

revised IAS 19 and the reported numbers for 2012 will be restated

accordingly for comparison reason.

The amended standard removes the option to use the corridor method

currently used by the Volvo Group. Discount rate will be used when calcu-

lating the net interest income or expense on the net defined benefit liabil-

ity (asset), hence the expected return will no longer be used. All changes

in the net defined benefit liability or asset will be recognized when they

occur. Service cost and net interest will be recognized in profit and loss

while remeasurements such as actuarial gains and losses will be recognized

in other comprehensive income.

In accordance with IAS 19 revised, the recognized pension liability will

increase by approximately SEK 12 billion as the unrecognized part of the

pension liability no longer can be reported off balance. Shareholders’

equity will decrease by approximately SEK 8 billion net of deferred taxes

in the opening balance for 2012 in accordance with IAS 19 revised. Net

financial position including post-employment benefits would increase by

SEK 12 billion while the equity ratio would decrease. Further changes in

the net defined benefit liability will be the modified net interest calculation

and the removal of the amortisation of actuarial gains and losses.

NOTES TO FINANCIAL STATEMENTS

FINANCIAL INFORMATION 2011

82