Nokia 2014 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2014 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

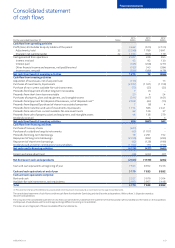

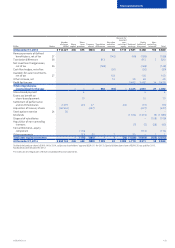

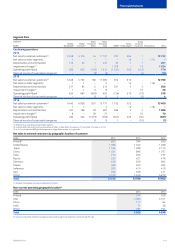

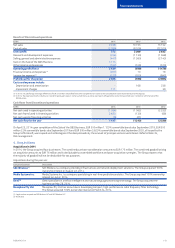

135

Financial statements

NOKIA IN 2014

Loans receivable

Loans receivable include loans to customers and suppliers and are

measured initially at fair value and subsequently at amortized cost

less impairment using the eective interest method. Loans are subject

to regular review as to their collectability and available collateral.

An allowance is made if a loan is deemed not to be fully recoverable.

The related cost is recognized in other expenses or nancial expenses,

depending on the nature of the receivable to reect the shortfall

between the carrying amount and the present value of the expected

future cash ows. Interest income on loans receivable is recognized

in other income or nancial income by applying the eective

interest rate.

Bank and cash

Cash consists of cash at bank and in hand.

Accounts receivable

Accounts receivable include both amounts invoiced to customers and

amounts where the Group’s revenue recognition criteria have been

fullled but the customers have not yet been invoiced. Accounts

receivable are carried at the original amount invoiced to customers

less allowances for doubtful accounts. Allowances for doubtful

accounts are based on a periodic review of all outstanding amounts,

including an analysis of historical bad debt, customer concentrations,

customer creditworthiness, past due amounts, current economic

trends and changes in customer payment terms. Impairment charges

on receivables identied as uncollectible are included in other

operating expenses. The Group derecognizes an accounts receivable

balance only when the contractual rights to the cash ows from the

asset expire or it transfers the nancial asset and substantially all the

risks and rewards of the asset to another entity.

Financial liabilities

The Group has classied its nancial liabilities into the following

categories: derivative and other current nancial liabilities, compound

nancial instruments, loans payable, and accounts payable. Derivatives

are described in the section on derivative nancial instruments.

Compound nancial instruments

Compound nancial instruments have both a nancial liability and an

equity component from the issuers’ perspective. The components are

dened based on the terms of the nancial instrument and presented

and measured separately according to their substance. The nancial

liability component is initially recognized at fair value, the residual

being allocated to the equity component. The allocation remains the

same for the life of the compound nancial instrument. The Group

has issued convertible bonds for which the nancial liability

component is accounted for as a loan payable.

Loans payable

Loans payable are recognized initially at fair value net of transaction

costs. In subsequent periods, loans payable are presented at

amortized cost using the eective interest method. Transaction costs

and loan interest are recognized in the consolidated income statement

as nancial expenses over the life of the instrument.

Accounts payable

Accounts payable are carried at invoiced amount which is considered

to be the fair value due to the short-term nature of the Group’s

accounts payable.

Derivative nancial instruments

All derivatives are recognized initially at fair value on the date a

derivative contract is entered into and subsequently remeasured at

fair value. The method of recognizing the resulting gain or loss varies

according to whether the derivatives are designated and qualify under

hedge accounting. Generally, the cash ows of a hedge are classied

as cash ows from operating activities in the consolidated statement

of cash ows as the underlying hedged items relate to the Group’s

operating activities. When a derivative contract is accounted for as

a hedge of an identiable position relating to nancing or investing

activities, the cash ows of the contract are classied in the same

way as the cash ows of the position being hedged.

Derivatives not designated in hedge accounting relationships

carried at fair value through prot and loss

Forward foreign exchange contracts are valued at market forward

exchange rates. Changes in fair value are measured by comparing

these rates with the original contract forward rate. Currency options

are valued at each statement of nancial position date by using the

Garman & Kohlhagen option valuation model. Changes in fair value

are recognized in the consolidated income statement.

Fair values of forward rate agreements, interest rate options, futures

contracts and exchange traded options are calculated based on

quoted market rates at each statement of nancial position date.

Discounted cash ow analyses are used to value interest rate and

cross-currency interest rate swaps. Changes in fair value are

recognized in the consolidated income statement.

For derivatives not designated under hedge accounting but

hedging identiable exposures such as anticipated foreign currency

denominated sales and purchases, the gains and losses are recognized

in other income or expenses. The gains and losses on all other

derivatives not designated under hedge accounting are recognized

in nancial income and expenses.

Embedded derivatives, if any, are identied and monitored by the

Group and measured at fair value at each consolidated statement

of nancial position date with changes in fair value recognized in the

consolidated income statement.

Hedge accounting

The Group applies hedge accounting on certain forward foreign

exchange contracts, certain options or option strategies, and certain

interest rate derivatives. Qualifying options and option strategies have

zero net premium or a net premium paid. For option structures, the

critical terms of the bought and sold options are the same and the

nominal amount of the sold option component is no greater than

that of the bought option.

Cash ow hedges: hedging of forecast foreign currency

denominated sales and purchases

The Group applies hedge accounting for ‘qualifying hedges’. Qualifying

hedges are those properly documented cash ow hedges of foreign

exchange rate risk of future forecast foreign currency denominated

sales and purchases that meet the requirements set out in IAS 39,

Financial Instruments: Recognition and Measurement. The hedged

item must be ‘highly probable’ and present an exposure to variations

in cash ows that could ultimately aect prot or loss. The hedge must

be highly eective, both prospectively and retrospectively.