Nokia 2006 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2006 Nokia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

|

|

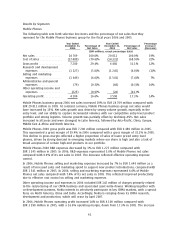

Accounting developments

The International Accounting Standards Board, or IASB, has and will continue to critically examine

current International Financial Reporting Standards, or IFRS, with a view toward increasing

international harmonization of accounting rules. This process of amendment and convergence of

worldwide accounting rules continued in 2006 resulting in amendments to the existing rules

effective from January 1, 2007 and additional amendments effective the following year. These are

discussed in more detail under ‘‘New IFRS standards and revised IAS standards’’ in Note 1 to our

consolidated financial statements included in Item 18 of this annual report on Form 20F. There were

no material IFRS accounting developments adopted in 2006.

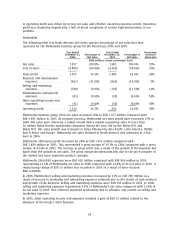

Critical Accounting Policies

Our accounting policies affecting our financial condition and results of operations are more fully

described in Note 1 to our consolidated financial statements included in Item 18 of this annual

report on Form 20F. Certain of Nokia’s accounting policies require the application of judgment by

management in selecting appropriate assumptions for calculating financial estimates, which

inherently contain some degree of uncertainty. Management bases its estimates on historical

experience and various other assumptions that are believed to be reasonable under the

circumstances, the results of which form the basis for making judgments about the reported carrying

values of assets and liabilities and the reported amounts of revenues and expenses that may not be

readily apparent from other sources. Actual results may differ from these estimates under different

assumptions or conditions.

Nokia believes the following are the critical accounting policies and related judgments and estimates

used in the preparation of its consolidated financial statements. We have discussed the application

of these critical accounting estimates with our Board of Directors and Audit Committee.

Revenue recognition

Revenue from the majority of the Group is recognized when persuasive evidence of an arrangement

exists, delivery has occurred, the fee is fixed or determinable, collectibility is probable and the

significant risks and rewards of ownership have transferred to the buyer. The remainder of revenue

is recorded under the percentage of completion method.

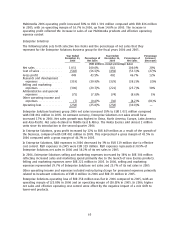

Mobile Phones, Multimedia and certain Enterprise Solutions and Networks revenue is generally

recognized when persuasive evidence of an arrangement exists, delivery has occurred, the fee is

fixed or determinable, collectibility is probable and significant risks and rewards of ownership have

transferred to the buyer. This requires us to assess at the point of delivery whether these criteria

have been met. When management determines that such criteria have been met, revenue is

recognized. Nokia records estimated reductions to revenue for special pricing agreements, price

protection and other volume based discounts at the time of sale, mainly in the mobile device

business. Sales adjustments for volume based discount programs are estimated based largely on

historical activity under similar programs. Price protection adjustments are based on estimates of

future price reductions and certain agreed customer inventories at the date of the price adjustment.

An immaterial part of the revenue from products sold through distribution channels is recognized

when the reseller or distributor sells the product to the enduser. Service revenue is generally

recognized on a straight line basis over the specified period unless there is evidence that some other

method better represents the stage of completion. Except for separately licensed software solutions

and certain Networks’ equipment, the company generally considers the software content of its

products or services to be incidental to the products or services as a whole.

Networks revenue and cost of sales from contracts involving solutions achieved through modification

of complex telecommunications equipment is recognized on the percentage of completion basis

when the outcome of the contract can be estimated reliably. This occurs when total contract revenue

and the cost to complete the contract can be estimated reliably, it is probable that economic

54