Neiman Marcus 2014 Annual Report Download - page 79

Download and view the complete annual report

Please find page 79 of the 2014 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

|

|

Table of Contents

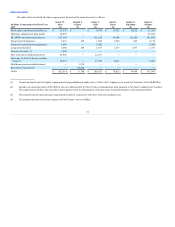

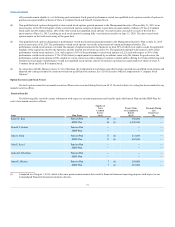

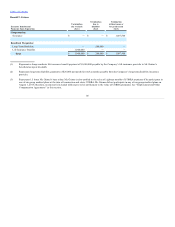

(2) For purposes of calculating the amounts in this column, retirement age was assumed to be the normal retirement age of the later of age 65 or the fifth

anniversary of the individual’s "date of hire," as defined in the Pension Plan. A description of the valuation method and all material assumptions

applied in quantifying the present value of accumulated benefit is set forth in Note 11 of the Notes to Consolidated Financial Statements.

(3) Ms. Katz’s service credit exceeds the 25-year maximum set forth in the SERP Plan. Pursuant to an agreement with us, Ms. Katz was entitled to an

additional year of credit for each full year of service after she reached the 25-year maximum until December 31, 2010, with all service frozen as of

such date. In addition, if her employment is terminated by us for any reason other than death, “disability,” “cause” or for non-renewal of her

employment term, or if she terminates her employment with us for “good reason” or “retirement” and she has not yet reached 65, her SERP Plan

benefit will not be reduced solely by reason of her failure to reach 65 as of the termination date. Ms. Katz’s employment agreement also provides

that the amount credited to her under the DC SERP shall not be less than the present value of the additional benefits she would have accrued under

the SERP Plan after December 31, 2010 had the SERP Plan remained in effect through the end of her employment term. The value of Ms. Katz’s

benefit with all service is $4,549,000. The value with 25 years of service under the SERP Plan is $4,353,000; therefore, the value of the additional

years of service in excess of her actual service is $196,000.

(4) Effective December 31, 2007, benefit accruals for Messrs. Gold and Skinner under the Pension Plan and the SERP Plan were frozen, as further

described below.

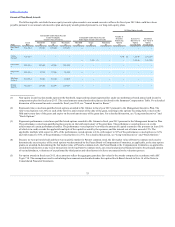

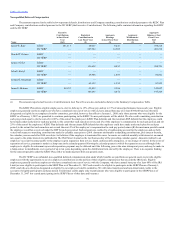

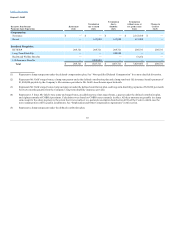

The Pension Plan is a funded, tax-qualified pension plan. Prior to 2008, most non-union employees over age 21 who had completed one year of

service with 1,000 or more hours were eligible to participate in the Pension Plan, which paid benefits upon retirement or termination of employment.

Effective as of December 31, 2007, eligibility and benefit accruals under the Pension Plan were frozen for all participants except for those “Rule of 65”

employees who elected to continue participating in the Pension Plan. The Pension Plan is a “career-accumulation” plan, under which a participant earns each

year a retirement annuity equal to one percent of his or her compensation for the year up to the Social Security wage base and 1.5 percent of his or her

compensation for the year in excess of such wage base. “Compensation” for this purpose generally includes salary, bonuses, commissions and overtime but

not in excess of the limits imposed upon annual compensation under Section 401(a)(17) of the Internal Revenue Code of 1986, as amended (the Code) (the

IRS Limit). The IRS Limit for calendar year 2015 is $265,000, increased from $260,000 for calendar year 2014, and is adjusted annually for cost-of-living

increases. Benefits under the Pension Plan become fully vested after five years of service with us. Effective August 1, 2010, benefit accruals were frozen for

the remaining “Rule of 65” employees and such participants were given the opportunity to participate in the RSP.

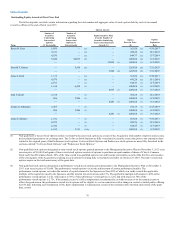

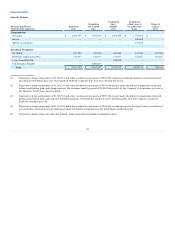

The SERP Plan is an unfunded, non-qualified plan under which benefits are paid from our general assets to supplement Pension Plan benefits and

Social Security. Prior to 2008, executive, administrative and professional employees (other than those employed as salespersons) with an annual base salary

at least equal to a minimum established by the Company were eligible to participate. Similar to the Pension Plan, effective December 31, 2007, eligibility

and benefit accruals under the SERP Plan were frozen for all participants except for those “Rule of 65” employees who elected to continue participating in

the Pension Plan. At normal retirement age (the later of age 65 and the fifth anniversary of the participant’s date of hire), an eligible participant with 25 or

more years of service is entitled to full benefits in the form of monthly payments under the SERP Plan computed as a straight life annuity, equal to 50 percent

of the participant’s average monthly compensation for the highest consecutive 60 months preceding retirement less 60 percent of his or her estimated annual

primary Social Security benefit, offset by the benefit accrued by the participant under the Pension Plan. The amount is then adjusted actuarially to determine

the actual monthly payments based on the time and form of payment. For this purpose, “compensation” includes salary but does not include bonuses. If the

participant has fewer than 25 years of service, the combined benefit is proportionately reduced. Benefits under the SERP Plan become fully vested after five

years of service. The SERP Plan is designed to comply with the requirements of Section 409A of the Code. Along with the Pension Plan and the ESP, benefit

accruals under the SERP Plan were frozen for the remaining “Rule of 65” employees effective August 1, 2010 and those remaining participants were given

the opportunity to participate in the DC SERP.

78