Neiman Marcus 2014 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2014 Neiman Marcus annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

|

|

Table of Contents

• higher delivery and processing net costs of approximately 0.4% of revenues due to the free shipping/free returns policy mentioned above; and

• higher buying and occupancy costs of approximately 0.2% of revenues as a result of (1) non-cash purchase accounting adjustments to increase

our lease rentals to estimated market rates at the Acquisition date and (2) higher rental rates incurred in connection with the expansion of our

small format stores.

COGS were 64.9% of revenues in fiscal year 2015 compared to 69.1% of revenues for the thirty-nine weeks ended August 2, 2014 (Successor) and

60.7% of revenues for the thirteen weeks ended November 2, 2013 (Predecessor). The difference in COGS for fiscal year 2015 compared to the foregoing

Predecessor and Successor periods is due primarily to the factors described above as well as seasonal considerations. Our first and third fiscal quarters are

generally characterized by a higher level of full-price sales and margins. For additional information on how seasonality affects our COGS, see "—

Seasonality."

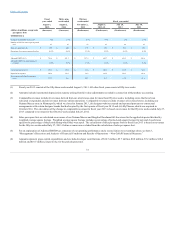

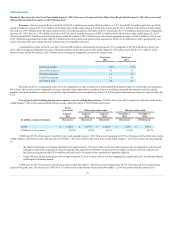

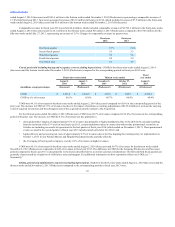

Selling, general and administrative expenses (excluding depreciation). SG&A in fiscal year 2015 compared to the thirty-nine weeks ended August

2, 2014 (Successor) and the thirteen weeks ended November 2, 2013 (Predecessor) were:

SG&A

$ 1,162.1

$ 875.8

$ 835.0

$ 286.3

$ 266.4

SG&A as a % of revenues

22.8%

22.4%

22.5%

24.1%

23.6%

SG&A expenses as a percentage of revenues decreased 0.1% of revenues to 22.4% in the thirty-nine weeks ended August 1, 2015 (Successor)

compared to 22.5% of revenues in the corresponding period of the prior year due primarily to:

• lower current and long-term incentive compensation costs of approximately 0.5% of revenues; partially offset by

• higher expenses of approximately 0.4% of revenues driven by the recent expansion of our small format stores, the remodels of our full-line

stores and the acquisition of MyTheresa.

SG&A expenses as a percentage of revenues increased 0.5% of revenues to 24.1% in the thirteen weeks ended November 1, 2014 (Successor)

compared to 23.6% of revenues in the prior year fiscal period due primarily to:

• higher planned investments and initiative costs of approximately 0.2% of revenues associated with our ongoing investments in corporate

initiatives and pre-opening costs incurred in connection with the opening of three small format stores in the thirteen weeks ended November 1,

2014 (Successor);

• higher selling costs of approximately 0.2% of revenues driven in part by the expansion of our small format stores; and

• higher current incentive compensation costs of approximately 0.1% of revenues.

SG&A was 22.8% of revenues in fiscal year 2015 compared to 22.5% of revenues for the thirty-nine weeks ended August 2, 2014 (Successor) and

23.6% of revenues for the thirteen weeks ended November 2, 2013 (Predecessor). The difference in SG&A for fiscal year 2015 compared to the foregoing

Predecessor and Successor periods is due primarily to the factors described above as well as seasonal considerations. Our first and third fiscal quarters are

generally characterized by a higher level of full-price sales and margins. For additional information on seasonality, see "—Seasonality."

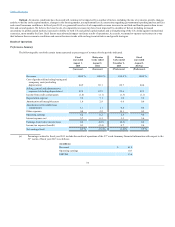

Income from credit card program. Income from our credit card program was $52.8 million, or 1.0% of revenues, in fiscal year 2015 compared to

$40.7 million, or 1.1% of revenues, in the thirty-nine weeks ended August 2, 2014 (Successor) and $14.7 million, or 1.3% of revenues, in the thirteen weeks

ended November 2, 2013 (Predecessor).

Depreciation and amortization expenses. Depreciation expense was $185.6 million, or 3.6% of revenues, in fiscal year 2015 compared to $113.3

million, or 3.1% of revenues, in the thirty-nine weeks ended August 2, 2014 (Successor) and $34.2 million, or 3.0% of revenues, in the thirteen weeks ended

November 2, 2013 (Predecessor). The increase in depreciation

40