Chrysler 2003 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2003 Chrysler annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

|

|

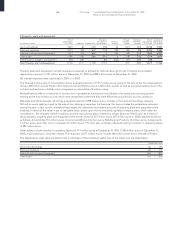

76 Fiat Group Consolidated Financial Statements at December 31, 2003

Notes to the Consolidated Financial Statements

currency are translated at the exchange rate in effect at year

end. Resulting exchange gains and losses are included in the

statement of operations.

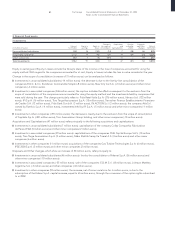

Taxes payable includes the tax charge for the current year

recorded in the statement of operations.

Accruals and deferrals

Accruals and deferrals are determined using the accrual method

based on the income and expense to which they relate.

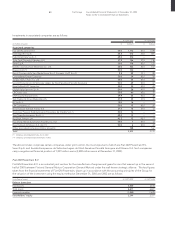

Securitization of financial receivables

The Fiat Group has programs for discounting financial

receivables originated by the financial services companies

using securitization transactions. This discounting of financial

receivables calls for the sale without recourse of a portfolio

of financial receivables to a non-Group securitization vehicle.

This company finances the purchase of the portfolio by issuing

securities which it backs (Asset Backed Securities). The securities

issued are divided into two types having different characteristics:

the first is placed on the market, occasionally subdivided by

various classes of ratings, and subscribed to by investors; the

second, the reimbursement of which is subordinated to the first,

is subscribed to by the seller. The risk for the seller is limited

to the portion of the securities which it has subscribed. At the

end of each accounting period, therefore, such securities are

evaluated in relation to the performance of the receivables

sold and may be written down on the basis of this evaluation.

These securities are recorded in Financial receivables.

Lastly, these sales without recourse require the immediate

recognition of the present value of the future margin implicit

in the receivables sold, net of discounting costs. This net value

is included in the Value of production since it relates to revenues

arising out of the normal operations of the financial services

companies (to this end, the financial income of such companies

is included in revenues from sales and services, as described

in the relevant note).

Memorandum accounts

Derivative financial instruments

Financial instruments used to hedge exchange and interest rate

fluctuations and, in general, changes in the assets and liabilities,

are presented in Note 14. Derivative financial instruments are

recorded at inception in the memorandum accounts at their

notional contract amount.

Beginning in 2001 the Fiat Group adopted – to the extent that

it is consistent and not in contrast with general principles set

forth in the Italian law governing financial statements – the

international accounting standard IAS 39 “Financial Instruments:

Recognition and Measurement”, applicable beginning January

1, 2001. Such principle covers the accounting treatment of all

financial assets and liabilities in and off-balance sheet and, in

particular, states that derivative financial instruments should be

valued at fair value. Taking into account the restrictions under

Italian law and the evolution of the law now underway, the

Group maintains, consistently with Consob rulings, that IAS

39 is immediately applicable only in part and only in reference

to the designation of derivative financial instruments as

“hedging” or “non-hedging instruments” and with respect

to the symmetrical accounting of the result of the valuation of

the derivative hedging instrument and the result attributable

to the hedged item (“hedge accounting”). The transactions

which, according to the Group’s policy for risk management, are

able to meet the conditions stated by the accounting principle

for hedge accounting treatment are designated as hedging

transactions; the others although set up for the purpose of

managing risk (inasmuch as the Group’s policy does not permit

speculative transactions), have been designated as “trading”.

Details of the accounting treatment adopted are as follows.

For foreign exchange instruments designated as hedges,

the premium (or discount, representing the difference between

the spot exchange rate at the inception of the contract and

the forward exchange rate) is recorded in the statement of

operations, in Financial income and expenses, in accordance

with the accrual method. Differences between the value of such

instruments using the exchange rates at inception and those

at year end are also included in the statement of operations

to offset the exchange effects of the items being hedged. In

particular, for contracts put into place to hedge the exchange

risk of future transactions that are considered highly probable,

the effects of the alignment with the year-end exchange rate

are deferred until the year in which the underlying transactions

are recorded.

For interest rate instruments designated as hedges, the interest

rate differential is included in the statement of operations, in

Financial income and expenses, in accordance with the accrual

method, offsetting the effects of the hedged transaction.

Derivative financial instruments hedging interest rate

fluctuations that are designated as trading instruments are

valued at market value and the differential, if negative

compared to the contractual value, is recorded in the statement

of operations as Financial income and expenses, in accordance

with the concept of prudence.

The same prudent principle is followed in recording derivative

financial instruments to manage trading risks (for example

equity swaps) that do not meet the conditions for hedge

accounting treatment.

Statement of Operations

Revenue recognition

Revenues from sales and services are recognized on the accrual

basis net of returns, discounts, allowances and rebates.