Capital One 2006 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2006 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

46

For the year, average branch-based deposits increased approximately $1.3 billion. Deposit growth was the result of an

increase in deposits in the hurricane impacted areas during the first few months of the year. This growth was the continuation

of a surge in deposits experienced in the fourth quarter of 2005 after the hurricanes. Deposit growth in the second half of the

year primarily came from Texas, where the Company continued to open new branches. Deposits decreased in the fourth

quarter as new growth in Texas was offset by attrition in the hurricane impacted areas.

During 2006, the Company determined that $25.7 million of allowance for loan losses previously established to cover

expected losses in the portion of the loan portfolio impacted by the hurricanes was no longer needed. This determination was

driven by improvements in credit performance of the impacted portfolios since the time those reserves were established. As a

result, results for the Banking segment include the reversal of this allowance.

During 2006, the Company opened 33 new branches in Texas, with 14 opened in the fourth quarter. An additional 6 branches

opened during the first two weeks of January 2007. These new branches contributed to the deposit growth mentioned above.

The costs of operating these branches, including lease costs, depreciation and personnel, is included in non-interest expense.

Also included in non-interest expense are costs associated with the integration of Hibernia into the Company. Substantially

all integration activities related to Hibernia have been or will be completed by the end of the first quarter of 2007.

VIII. Funding

Funding Availability

The Company has established access to a variety of funding sources. Table 6 illustrates the Companys unsecured funding

sources and its two auto securitization warehouses.

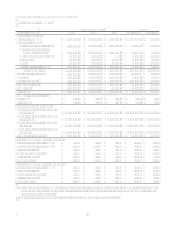

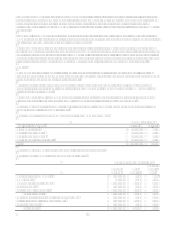

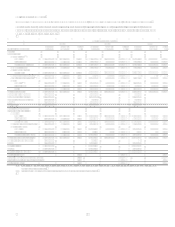

Table 6: Funding Availability

(Dollars or dollar equivalents in millions) Effective/

Issue Date Availability (1)(5) Outstanding

Final

Maturity(4)

Senior and Subordinated Global Bank Note Program(2) 1/03 $ 1,800 $ 3,183

Senior Domestic Bank Note Program(3) 4/97 $ 166

Credit Facility 6/04 $ 750 6/07

Capital One Auto Loan Facility I $ 2,839 $ 461

Capital One Auto Loan Facility II 3/05 $ 592 $ 1,158

Corporation Shelf Registration 10/05 $ 2,500 N/A

(1) All funding sources are non-revolving except for the Credit Facility and the Capital One Auto Loan Facilities. Funding availability under the credit facilities is

subject to compliance with certain representations, warranties and covenants. Funding availability under all other sources is subject to market conditions.

(2) The notes issued under the Senior and Subordinated Global Bank Note Program may have original terms of thirty days to thirty years from their date of issuance.

This program was updated in June 2005.

(3) The notes issued under the Senior Domestic Bank Note Program have original terms of one to ten years. The Senior Domestic Bank Note Program is no longer

available for issuances.

(4) Maturity date refers to the date the facility terminates, where applicable.

(5) Availability does not include unused conduit capacity related to securitization structures of $7.9 billion at December 31, 2006.

The Senior and Subordinated Global Bank Note Program gives the Bank the ability to issue securities to both U.S. and non-

U.S. lenders and to raise funds in U.S. and foreign currencies, subject to conditions customary in transactions of this nature.

Prior to the establishment of the Senior and Subordinated Global Bank Note Program, the Bank issued senior unsecured debt

through an $8.0 billion Senior Domestic Bank Note Program. The Bank did not renew the Senior Domestic Bank Note

Program for future issuances following the establishment of the Senior and Subordinated Global Bank Note Program.

In June 2004, the Company terminated its Domestic Revolving and Multicurrency Credit Facilities and replaced them with a

new revolving credit facility (Credit Facility) providing for an aggregate of $750.0 million in unsecured borrowings from

various lending institutions to be used for general corporate purposes. The Credit Facility is available to the Corporation, the

Bank, the Savings Bank, and Capital One Bank (Europe), plc, subject to covenants and conditions customary in transactions

of this type. The Corporations availability has been increased to $500.0 million under the Credit Facility. All borrowings

under the Credit Facility are based upon varying terms of London Interbank Offering Rate (LIBOR).

In April 2002, COAF entered into a revolving warehouse credit facility collateralized by a security interest in certain auto

loan assets (the Capital One Auto Loan Facility I). As of December 31, 2006, the Capital One Auto Loan Facility I had the

capacity to issue up to $3.3 billion in secured notes. The Capital One Auto Loan Facility I has multiple participants each with

separate renewal dates. The facility does not have a final maturity date. Instead, each participant may elect to renew the

commitment for another set period of time. Interest on the facility is based on commercial paper rates.