Capital One 2006 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2006 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

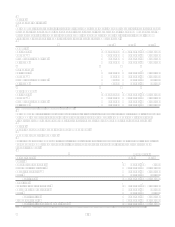

104

payments to plaintiffs and for changes in policies and interchange rates for debit cards. Certain merchant plaintiffs have opted

out of the settlements and have commenced separate lawsuits. Additionally, consumer class action lawsuits with claims

mirroring the merchants allegations have been filed in several courts. Finally, MasterCard and Visa, as well as certain

member banks, continue to face additional lawsuits regarding policies, practices, products and fees.

With the exception of the Interchange lawsuits and the Amex lawsuit, the Corporation and its subsidiaries are not parties to

the lawsuits against MasterCard and Visa described above and therefore will not be directly liable for any amount related to

any possible or known settlements of such lawsuits. However, the Corporations subsidiary banks are member banks of

MasterCard and Visa and thus may be affected by settlements or lawsuits relating to these issues, including changes in

interchange payments. In addition, it is possible that the scope of these lawsuits may expand and that other member banks,

including the Corporations subsidiary banks, may be brought into the lawsuits or future lawsuits. In part as a result of such

litigation, MasterCard and Visa are expected to continue to evolve as corporate entities, including by changing their

governance structures as previously announced. During the second quarter of 2006, MasterCard successfully completed its

initial public offering and Visa revised its governance structure. Both entities now rely upon independent directors for certain

decisions, including the setting of interchange rates.

Given the complexity of the issues raised by these lawsuits and the uncertainty regarding: (i) the outcome of these suits,

(ii) the likelihood and amount of any possible judgments, (iii) the likelihood, amount and validity of any claim against the

member banks, including the Corporation and its subsidiary banks, (iv) changes in industry structure that may result from the

suits and (v) the effects of these suits, in turn, on competition in the industry, member banks, and interchange fees, the

Company cannot determine at this time the long-term effects of these suits.

Other Pending and Threatened Litigation

In January 2007, individual plaintiffs purporting to represent a class of cardholders filed an antitrust lawsuit (the Piñon

matter) against several issuing banks, including the Corporation, alleging among other things that the defendants conspired

to fix the level of late fees and over-limit fees charged to cardholders, and that these fees are excessive. The complaint

requests civil monetary damages, which could be trebled.

We believe that we have meritorious defenses with respect to this case and intend to defend this case vigorously. At the

present time, management is not in a position to determine whether the resolution of this case will have a material adverse

effect on either the consolidated financial position of the Corporation or the Corporations results of operations in any future

reporting period.

In addition, the Company also commonly is subject to various pending and threatened legal actions relating to the conduct of

its normal business activities. In the opinion of management, the ultimate aggregate liability, if any, arising out of any such

pending or threatened legal actions will not be material to the consolidated financial position or results of operations of the

Company.

Tax issues for years 1995-1999 are pending in the U.S. Tax Court. The ultimate resolution of these issues is not expected to

have a material effect upon the Corporations operations or financial condition.

Note 21

Related Party Transactions

In the ordinary course of business, executive officers and directors of the Company may have consumer loans issued by the

Company. Pursuant to the Companys policy, such loans are issued on the same terms as those prevailing at the time for

comparable loans to unrelated persons and do not involve more than the normal risk of collectibility.

Note 22

Off-Balance Sheet Securitizations

Off-balance sheet securitizations involve the transfer of pools of consumer loan receivables by the Company to one or more

third-party trusts or qualified special purpose entities in transactions that are accounted for as sales in accordance with SFAS

140. Certain undivided interests in the pool of consumer loan receivables are sold to investors as asset-backed securities in

public underwritten offerings or private placement transactions. The proceeds from off-balance sheet securitizations are

distributed by the trusts to the Company as consideration for the consumer loan receivables transferred. Each new off-balance

sheet securitization results in the removal of consumer loan principal receivables equal to the sold undivided interests in the

pool from the Companys consolidated balance sheet (off-balance sheet loans), the recognition of certain retained residual

interests and a gain on the sale. The remaining undivided interests in principal receivables of the pool, as well as the unpaid

billed finance charge and fee receivables related to the Companys undivided interest in the principal receivables are retained

by the Company and recorded as consumer loans on the Consolidated Balance Sheet. The amounts of the remaining