Capital One 2006 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2006 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

40

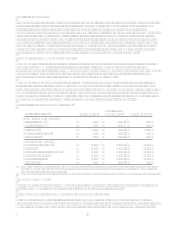

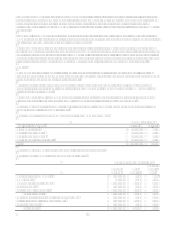

Net Charge-Offs

Net charge-offs include the principal amount of losses (excluding accrued and unpaid finance charges and fees and fraud

losses) less current period principal recoveries. The Company charges off credit card loans at 180 days past the due date and

generally charges off other consumer loans at 120 days past the due date or upon repossession of collateral. Non-

collateralized consumer bankruptcies are typically charged-off within 2-7 days upon notification and in any event within 30

days. Commercial loans are charged-off when the amounts are deemed uncollectible. Costs to recover previously charged-off

accounts are recorded as collection expenses in other non-interest expense.

The reported and managed net charge-off rates decreased 134 and 141 basis points, respectively, with net charge-off dollars

decreasing 1% on a reported and managed basis, for the year ended December 31, 2006 compared to the prior year. The

decrease in net charge-off rates is due to historically low levels of bankruptcies following the change in bankruptcy

legislation in the fourth quarter of 2005 and an increase in the concentration of higher credit quality loans in the reported loan

portfolio driven by recent acquisitions.

The reported and managed net charge-off rates decreased 23 and 16 basis points, respectively, while net charge-off dollars

increased 12% and 11% on a reported and managed basis, respectively, for the year ended December 31, 2005 compared to

the prior year. The decrease in net charge-off rates principally relates to the Companys continued asset diversification within

and beyond U.S. consumer credit cards. The increase in the net charge-off dollars was driven by growth in the reported and

managed loan portfolios combined with the incremental increase of bankruptcy charge-offs resulting from the enactment of

the new bankruptcy legislation. Reported and managed bankruptcy charge-offs increased $146.8 million and $394.8 million,

respectively, for the year ended December 31, 2005 when compared to the prior year.

For additional information, see section XII, Tabular Summary, Table F (Net Charge-offs).

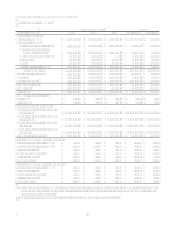

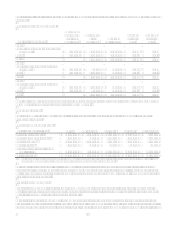

Nonperforming Assets

The Company assumed nonperforming assets in connection with the acquisitions of Hibernia and North Fork.

Nonperforming loans consist of nonaccrual loans (loans on which interest income is not currently recognized) and

restructured loans (loans with below-market interest rates or other concessions due to the deteriorated financial condition of

the borrower). Commercial, small business and some auto loans are placed in nonaccrual status at 90 days past due or sooner

if, in managements opinion, there is doubt concerning the ability to fully collect both principal and interest.

For additional information, see section XII, Tabular Summary, Table G (Nonperforming Assets).

Allowance for loan and lease losses

The allowance for loan and lease losses is maintained at the amount estimated to be sufficient to absorb probable principal

losses, net of principal recoveries (including recovery of collateral), inherent in the existing reported loan portfolios. The

provision for loan losses is the periodic cost of maintaining an adequate allowance. The amount of allowance necessary is

based on distinct allowance methodologies depending on the type of loans which include specifically identified criticized

loans, migration analysis, forward loss curves and historical loss trends. In evaluating the sufficiency of the allowance for

loan and lease losses, management takes into consideration the following factors: recent trends in delinquencies and charge-

offs including bankrupt, deceased and recovered amounts; forecasting uncertainties and size of credit risks; the degree of risk

inherent in the composition of the loan portfolio; economic conditions; legal and regulatory guidance; credit evaluations and

underwriting policies; seasonality; and the value of collateral supporting the loans. To the extent credit experience is not

indicative of future performance or other assumptions used by management do not prevail, loss experience could differ

significantly, resulting in either higher or lower future provision for loan and lease losses, as applicable. The evaluation

process for determining the adequacy of the allowance for loan losses and the periodic provisioning for estimated losses is

undertaken on a quarterly basis, but may increase in frequency should conditions arise that would require the Companys

prompt attention. Conditions giving rise to such action are business combinations or other acquisitions or dispositions of

large quantities of loans, dispositions of non-performing and marginally performing loans by bulk sale or any development

which may indicate an adverse trend.

The allowance for loan losses increased $390.0 million from December 31, 2005 driven primarily by the acquisition of North

Fork which added $222.2 million of allowance for loan losses at December 31, 2006. The remaining increase was the result

of 8% growth in the reported loan portfolio, exclusive of the North Fork loans portfolio.

During 2006, the Company determined that $25.7 million of allowance for loan losses previously established by Hibernia to

cover expected losses in the portion of the loan portfolio impacted by the 2005 hurricanes was no longer needed. This

determination was driven by improvements in credit performance of the impacted portfolios since the time those reserves