Capital One 2006 Annual Report Download - page 126

Download and view the complete annual report

Please find page 126 of the 2006 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

108

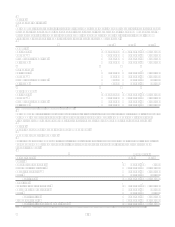

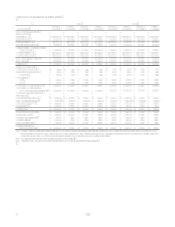

The Company has entered into forward exchange contracts to reduce the Companys sensitivity to foreign currency exchange

rate changes on its foreign currency denominated loans. The forward rate agreements allow the Company to lock-in

functional currency equivalent cash flows associated with the foreign currency denominated loans.

During the year ended December 31, 2006, the Company recognized no losses related to the ineffective portions of its cash

flow hedging instruments. During the year ended December 31, 2005, the Company recognized $3.1 million of losses,

recorded in other non-interest income, related to the ineffective portions of its cash flow hedging instruments. The Company

recognized no net gains or losses during the years ended December 31, 2006 and December 31, 2005 for cash flow hedges

that have been discontinued because the forecasted transaction was no longer probable of occurring.

At December 31, 2006, the Company expects to reclassify $0.9 million of net losses, after tax, on derivative instruments from

cumulative other comprehensive income to earnings during the next 12 months as terminated swaps are amortized and as

interest payments and receipts on derivative instruments occur.

Hedge of Net Investment in Foreign Operations

The Company uses forward exchange contracts to protect the value of its investment in its foreign subsidiaries. Realized and

unrealized foreign currency gains and losses from these hedges are not included in the income statement, but are shown in the

translation adjustments in other comprehensive income. The purpose of these hedges is to protect against adverse movements

in exchange rates.

For the years ended December 31, 2006 and 2005, net gains of $1.5 million and $0.3 million respectively, related to these

derivatives were included in the cumulative translation adjustment.

Non-Trading Derivatives

The Company uses interest rate swaps to manage interest rate sensitivity related to loan securitizations. The Company enters

into interest rate swaps with its securitization trust and essentially offsets the derivative with separate interest rate swaps with

third parties.

The Company uses interest rate swaps in conjunction with its auto securitizations. These swaps have zero balance notional

amounts unless the paydown of auto securitizations differs from its scheduled amortization.

The Company enters into customer-oriented derivative financial instruments, including interest rate swaps, options, caps,

floors, and foreign exchange contracts. These customer-oriented positions are matched with offsetting positions to minimize

risk to the Company.

These derivatives do not qualify as hedges and are recorded on the balance sheet at fair value with changes in value included

in current earnings. During the years ended December 31, 2006 and 2005, the Company had net gains of $36.8 million and

$6.6 million, respectively, which are recorded in non-interest income.

In April 2006, the Company entered into derivative instruments to mitigate certain exposures it faced as a result of the

expected acquisition of North Fork. The position was designed to protect the Companys tangible capital ratios from falling

below a desired level in the event that subsequent increases in interest rates had reduced the mark-to-market value of North

Forks balance sheet prior to closing. The Companys maximum negative exposure was no more than approximately $50

million. The derivative instruments were not treated as designated hedges and were marked to market through the income

statement until expiration. During their existence, $30.2 million was recognized as a reduction to mortgage banking

operations income as a mark to market adjustment. The derivative instruments expired out of the money and unexercised on

October 2, 2006 with a $19.9 million reduction to mortgage banking operations income.

Mortgage Banking Derivatives

The Company, as part of its mortgage banking operations, enters into commitments to originate or purchase loans whereby

the interest rate of the loan is determined prior to funding (interest rate lock commitment). Interest rate lock commitments

on mortgage loans that the Company intends to sell in the secondary market are considered freestanding derivatives. These

derivatives are carried at fair value with changes in fair value reported as a component of gain on sale of loans. In accordance

with Staff Accounting Bulletin No, 105, Application of Accounting Principles to Loan Commitments, interest rate lock

commitments are initially valued at zero. Changes in fair value subsequent to inception are determined based on current

secondary market prices for underlying loans with similar coupons, maturity and credit quality, subject to the anticipated

probability that the loans will fund within the terms of the commitment. The initial value inherent in the loan commitments at

origination is recognized through gain on sale of loans when the underlying loan is sold. Both the interest rate lock