Capital One 2006 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2006 Capital One annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

|

|

106

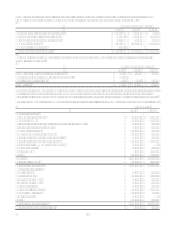

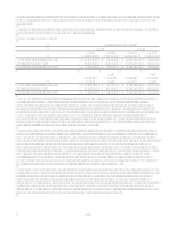

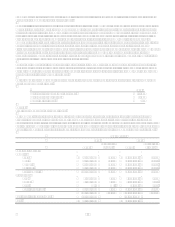

Securitization Key Assumptions

Year Ended December 31 2006 2005

Weighted average life for receivables (months) 8 to 9 9 to 10

Principal repayment rate (weighted average rate) 14% to 16% 13% to 14%

Charge-off rate (weighted average rate) 3% to 4% 4% to 5%

Discount rate (weighted average rate) 10% to 13% 9% to 13%

If these assumptions are not met, or if they change, the interest-only strip and related servicing and securitizations income

would be affected. The following adverse changes to the key assumptions and estimates, presented in accordance with SFAS

140, are hypothetical and should be used with caution. As the figures indicate, any change in fair value based on a 10% or

20% variation in assumptions cannot be extrapolated because the relationship of a change in assumption to the change in fair

value may not be linear. Also, the effect of a variation in a particular assumption on the fair value of the interest-only strip is

calculated independently from any change in another assumption. However, changes in one factor may result in changes in

other factors, which might magnify or counteract the sensitivities.

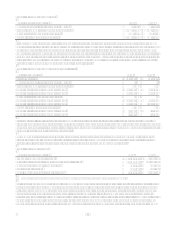

Securitization Key Assumptions and Sensitivities

As of December 31 2006 2005

Interest-only strip $ 448,684 $ 419,196

Weighted average life for receivables (months) 8 9

Principal repayment rate (weighted average rate) 16% 14%

Impact on fair value of 10% adverse change $ (26,505) $ (13,802)

Impact on fair value of 20% adverse change (49,799) (25,203)

Charge-off rate (weighted average rate) 4% 4%

Impact on fair value of 10% adverse change $ (45,334) $ (62,326)

Impact on fair value of 20% adverse change (90,476) (124,536)

Discount rate (weighted average rate) 10% 13%

Impact on fair value of 10% adverse change $ (2,042) $ (2,202)

Impact on fair value of 20% adverse change (4,109) (4,378)

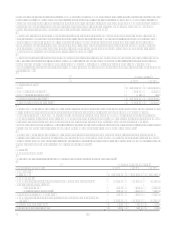

Static pool credit losses are calculated by summing the actual and projected future credit losses and dividing them by the

original balance of each pool of assets. Due to the short-term revolving nature of the consumer loan receivables, the weighted

average percentage of static pool credit losses is not considered materially different from the assumed charge-off rates used to

determine the fair value of the retained interests.

The Company acts as a servicing agent and receives contractual servicing fees of between 0.50% and 6% of the investor

principal outstanding, based upon the type of assets serviced. The Company generally does not record material servicing

assets or liabilities for these rights since the contractual servicing fee approximates market rates.

Securitization Cash Flows

Year Ended December 31 2006 2005

Proceeds from new securitizations $ 12,343,771 $ 9,482,333

Collections reinvested in revolving-period securitizations 85,525,697 76,224,390

Repurchases of accounts from the trust 236,964 391,118

Servicing fees received 893,046 846,535

Cash flows received on retained interests(1) 4,465,769 4,076,128

(1) Includes all cash receipts of excess spread and other payments (excluding servicing fees) from the Trust to the Company.

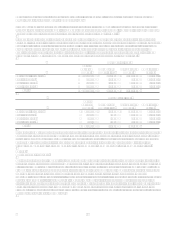

For the year ended December 31, 2006, the Company recognized gross gains of $50.4 million on the sale of $12.3 billion of

loan principal receivables compared to gross gains of $58.2 million on the sale of $9.5 billion of loan principal receivables

for the year ended December 31, 2005 and gross gains of $55.8 million on the sale of $10.9 billion of loans in 2004 These

gross gains are included in servicing and securitizations income. In addition, the Company recognized, as a reduction to

servicing and securitizations income, upfront securitization transaction costs and recurring credit facility commitment fees of

$66.1 million, $48.6 million and $69.0 million for the years ended December 31, 2006, 2005 and 2004, respectively. The

remainder of servicing and securitizations income represents servicing income and excess interest and non-interest income