Experian 2014 Annual Report Download - page 33

Download and view the complete annual report

Please find page 33 of the 2014 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

29

Strategic report • Chief Executive’s statement

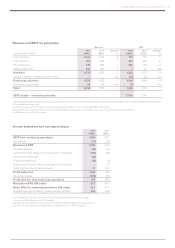

Total revenue growth from continuing

activities was 7% at constant currency

and organic revenue growth was

5% (H1 6%, H2 5%). We saw further

progress in EBIT margins, which rose

by 30 basis points to 27.4%, with EBIT

rising 8% at constant currencies.

Actual revenue and EBIT growth were

4% and 5% respectively, including the

contribution from recent acquisitions,

offset by negative currency translation

effects. Benchmark EPS increased to

91.7 US cents per share, up 8% at actual

exchange rates.

Notable highlights include:

• We grew across all four regions, with

organic revenue growth of 7% in Latin

America, 7% in the UK and Ireland,

4% in North America and 2% in

EMEA/Asia Pacific.

• We also grew across all four

global business lines, with organic

revenue growth of 10% in Decision

Analytics, 5% in Credit Services, 5%

in Consumer Services and 1% in

Marketing Services.

• Cash generation was a particular

highlight, as we converted 101% of

EBIT into operating cash, resulting

in a net debt to EBITDA ratio of 2.27

times, from a peak of over 2.5 times

in November 2013.

• We made significant strategic

progress, as we concentrate our

efforts across key growth initiatives.

We are placing significant emphasis

on fraud and identity management,

we are becoming increasingly

focused on a select number of

industry verticals and we are

sharpening our operations in our

most exciting geographies.

• We also raised our full year dividend

by 8% to 37.50 US cents per share.

Strategic and operational review

Let me focus on specific highlights for the

year and comment on our future direction:

Credit Services

We delivered good revenue growth in

Credit Services, up 5% organically.

With confidence gradually returning to

the retail lending sector, the core bureau

in North America performed well. While

declines in the US mortgage market

held back growth somewhat, lenders

are generally prospecting more for new

credit customers. We are also benefiting

as we steadily reduce our dependency on

financial services and raise our exposure

to faster-growing market segments.

We took a significant step in this

regard with the acquisition of Passport

Health Communications (‘Passport’)

which, combined with our existing

operations, makes us the leader in US

healthcare revenue cycle management,

a highly attractive market. Passport has

performed well since acquisition, as

described in more detail below.

Macro-economically, it was a challenging

year in Latin America, particularly in

Brazil. That said, it is gratifying to note

that our bureaux in the region were

collectively the fastest growing in the

Experian portfolio. During the year we

strengthened our operations in Brazil,

stepping up our ability to grow through

new products, new clients, new verticals

and by deploying services which straddle

our whole business. And while the World

Cup poses specific challenges in H1, we

are well placed to continue to expand

in Brazil and across the region over the

medium term.

We have seen improving momentum in

the UK, where we have placed significant

emphasis on increasing the data depth

of the bureau. This helps to open up new

market opportunities, enables greater

levels of innovation and ultimately creates

ever greater competitive distinction for

Experian. Overall, we feel well placed

as confidence and investment return to

the UK economy. Meanwhile, in EMEA/

Asia Pacific, we have acted to strengthen

our operations in parts of Continental

Europe, with good results, and we are

fully engaged in building positive data

in Australia, following the enactment of

regulations in March.

Decision Analytics

I am delighted with progress in Decision

Analytics, which returned to strong

revenue growth, up 10% organically.

For some time now, we have been

investing in our products and flexing our

infrastructure with the aim of creating a

more sustainable, high-growth Decision

Analytics business. We have made

considerable advances, positioning us

well for the future. PowerCurve, our new

flagship credit risk management software,

has met with worldwide success, and we

will continue the roll-out over the coming

year. Fraud and identity management

increasingly represents a new dimension

to our business, and has been pivotal in

opening up a new set of opportunities

in new client segments such as the US

public sector. We are investing further in

analytics, meeting demand from clients

for sophisticated tools to help them deal

with their big data challenges. Finally, I

should note the particular success we

have met with in EMEA/Asia Pacific

which, in response to previous actions,

recovered during the year.

P34

P38

P40

P34

P40

P36