Experian 2014 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2014 Experian annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

|

|

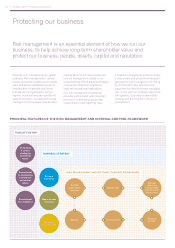

22 Strategic report • Protecting our business

Long-term performance risks

Throughout the year, we have critically reviewed and evaluated the risks Experian faces. This section outlines our assessment of

the most significant risks and uncertainties that could affect our long-term performance. These risks are not set out in any order or

priority. The list is not exhaustive and it is likely to change during the course of the year, as some risks assume greater importance

and others become less significant.

PRINCIPAL RISKS

REGULATORY COMPLIANCE

We must comply with international, federal, regional, provincial, state and other jurisdictional regulations and best practice, including but

not limited to privacy, consumer data protection, health and safety, tax, labour, environmental, anti-corruption and information security laws.

Performance indicator

EBIT and general

litigation trends

Strategic alignment

• Product innovation

• Geographic expansion

Description of risk

• We might fail to comply with international, federal,

regional, provincial, state or other jurisdictional

regulations, due to their complexity, frequent changes

or inconsistent application and interpretation.

Potential impact

• We may face increased costs to comply with

these regulations.

• If we fail to comply, we may have to pay fines or

face restrictions on our ability to carry on or expand

our operations.

How we manage this risk

• Our Global Compliance team has region-specific

regulatory expertise and works with our businesses

to identify and adopt compliance strategies.

Change from 2013

Increasing risk

2014 update

To the best of our knowledge, we comply

with data protection requirements in every

jurisdiction we operate in.

The UK Financial Conduct Authority

(‘FCA’) has been formed with rule-making,

investigative and enforcement powers

over some activities of our Credit Services

businesses. Both the US Consumer

Financial Protection Bureau and FCA

have similar objectives, tied to protecting

consumers’ interests. It remains uncertain

how these bodies may affect our Credit and

Consumer Services business processes

and business models in the future.

DATA OWNERSHIP AND ACCESS

Our products and services rely extensively upon data collected from public and private sources. The act of collecting and analysing large

quantities of this data generates more data, which augments our products and services.

Performance indicator

EBIT

Strategic alignment

• Product innovation

Description of risk

• Consumer privacy concerns could lead to changes

or restrictions in how consumer information is

collected, aggregated, analysed and used for

marketing, risk management and fraud detection.

• Our data providers could withdraw or be unable

to provide their data to us.

Potential impact

• Our ability to provide products and services to our clients

could be affected, leading to a materially adverse effect

on our business, reputation and operating results.

How we manage this risk

• We monitor legislative bills and educate lawmakers,

regulators, consumer and privacy advocates, industry

trade groups and other stakeholders in the public

policy debate.

• We use standardised selection, negotiation and

contracting of provider agreements, to address

delivery assurance, reliability and protections relating

to critical service provider relationships.

• Our legal contracts define the type and use of data

and services.

• We analyse data to make sure we receive data of

the best value and highest quality.

Change from 2013

Stable

2014 update

Momentum towards positive data, which

provides visibility into on-time payment

history, continues in some countries,

although the benefits of positive data laws

sometimes take longer to come into effect.

For example, Brazilian banks are being

cautious about how credit bureaux acquire

data-sharing permissions from consumers,

resulting in a protracted timeline for

adopting positive data. Separately,

we continue to enter into long-term

contracts with data providers, as well

as securing access to data sources

through acquisitions.

Protecting our business continued