Wells Fargo 2007 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

83

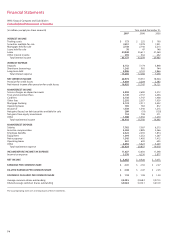

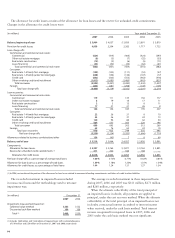

(in millions, except per Year ended December 31, 2005

share amounts)

Net income, as reported $7,671

Add: Stock-based employee compensation

expense included in reported net

income, net of tax 1

Less: Total stock-based employee

compensation expense under the

fair value method for all awards,

net of tax (188)

Net income, pro forma $7,484

Earnings per common share

As reported $ 2.27

Pro forma 2.22

Diluted earnings per common share

As reported $ 2.25

Pro forma 2.19

date of grant. Effective January 1, 2006, we adopted FAS

123(R), Share-Based Payment, using the “modified prospec-

tive” transition method. Accordingly, compensation cost

recognized in 2006 and 2007 includes (1) compensation cost

for share-based payments granted prior to, but not yet vested

as of the adoption date of January 1, 2006, based on the

grant date fair value estimated in accordance with FAS 123,

and (2) compensation cost for all share-based awards granted

on or after January 1, 2006. Results for prior periods have

not been restated. In calculating the common stock equiva-

lents for purposes of diluted earnings per share, we selected

the transition method provided by FASB Staff Position FAS

123(R)-3, Transition Election Related to Accounting for the

Tax Effects of Share-Based Payment Awards.

As a result of adopting FAS 123(R) on January 1, 2006,

income before income taxes of $11.6 billion and net income

of $8.1 billion for 2007 was $129 million and $80 million

lower, respectively, than if we had continued to account for

share-based compensation under APB 25, and, for 2006,

income before income taxes of $12.7 billion and net income

of $8.4 billion was $134 million and $84 million lower,

respectively. Basic and diluted earnings per share for 2007 of

$2.41 and $2.38, respectively, were both $0.025 per share

lower than if we had not adopted FAS 123(R), and, for

2006, basic and diluted earnings per share of $2.50 and

$2.47, respectively, were also both $0.025 per share lower.

Pro forma net income and earnings per common share

information are provided in the following table as if we

accounted for employee stock option plans under the fair

value method of FAS 123 in 2005.

Earnings Per Common Share

We present earnings per common share and diluted earnings

per common share. We compute earnings per common share

by dividing net income (after deducting dividends on preferred

stock) by the average number of common shares outstanding

during the year. We compute diluted earnings per common

share by dividing net income (after deducting dividends on

preferred stock) by the average number of common shares

outstanding during the year, plus the effect of common stock

equivalents (for example, stock options, restricted share

rights and convertible debentures) that are dilutive.

Derivatives and Hedging Activities

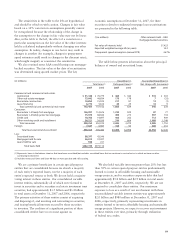

We recognize all derivatives in the balance sheet at fair value.

On the date we enter into a derivative contract, we designate

the derivative as (1) a hedge of the fair value of a recognized

asset or liability, including hedges of foreign currency exposure

(“fair value” hedge), (2) a hedge of a forecasted transaction

or of the variability of cash flows to be received or paid

related to a recognized asset or liability (“cash flow” hedge),

or (3) held for trading, customer accommodation or asset/

liability risk management purposes, including economic hedges

not qualifying under FAS 133, Accounting for Derivative

Instruments and Hedging Activities (“free-standing derivative”).

For a fair value hedge, we record changes in the fair value of

the derivative and, to the extent that it is effective, changes in

the fair value of the hedged asset or liability attributable to the

hedged risk, in current period earnings in the same financial

statement category as the hedged item. For a cash flow hedge,

we record changes in the fair value of the derivative to the

extent that it is effective in other comprehensive income, with

any ineffectiveness recorded in current period earnings. We

subsequently reclassify these changes in fair value to net income

in the same period(s) that the hedged transaction affects net

income in the same financial statement category as the hedged

item. For free-standing derivatives, we report changes in the

fair values in current period noninterest income.

For fair value and cash flow hedges qualifying under FAS

133, we formally document at inception the relationship

between hedging instruments and hedged items, our risk

management objective, strategy and our evaluation of effec-

tiveness for our hedge transactions. This includes linking all

derivatives designated as fair value or cash flow hedges to

specific assets and liabilities in the balance sheet or to specific

forecasted transactions. Periodically, as required, we also

formally assess whether the derivative we designated in each

hedging relationship is expected to be and has been highly

effective in offsetting changes in fair values or cash flows of

the hedged item using the regression analysis method or, in

limited cases, the dollar offset method.

We discontinue hedge accounting prospectively when

(1) a derivative is no longer highly effective in offsetting

changes in the fair value or cash flows of a hedged item,

(2) a derivative expires or is sold, terminated, or exercised,

(3) a derivative is de-designated as a hedge, because it is

unlikely that a forecasted transaction will occur, or (4) we

determine that designation of a derivative as a hedge is no

longer appropriate.

Stock options granted in each of our February 2005

and February 2004 annual grants, under our Long-Term

Incentive Compensation Plan (the Plan), fully vested upon

grant, resulting in full recognition of stock-based compensa-

tion expense for both grants in the year of the grant under

the fair value method in the table above. Stock options

granted in our 2003 annual grant under the Plan vest over a

three-year period, and expense reflected in the table for this

grant is recognized over the vesting period.