Wells Fargo 2007 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

60

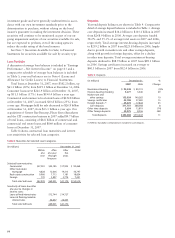

We consider the allowance for credit losses of $5.52 billion

adequate to cover credit losses inherent in the loan portfolio,

including unfunded credit commitments, at December 31, 2007.

Given that the majority of our loan portfolio is consumer

loans, for which losses tend to emerge within a relatively

short, predictable timeframe, and that a significant portion

of the allowance for credit losses is related to estimated

credit losses associated with consumer loans, management

believes that the provision for credit losses for consumer

loans, absent any significant credit event, severe decrease in

collateral values, significant acceleration of losses or signifi-

cant change in payment behavior, will closely track the level

of related net charge-offs. In 2007, due to further deteriora-

tion in the outlook for the housing market, we recorded a

credit reserve build, primarily for higher loss content that

we estimated in the Home Equity portfolio. The process for

determining the adequacy of the allowance for credit losses

is critical to our financial results. It requires difficult, subjec-

tive and complex judgments, as a result of the need to make

estimates about the effect of matters that are uncertain. (See

“Financial Review – Critical Accounting Policies – Allowance

for Credit Losses.”) Therefore, we cannot provide assurance

that, in any particular period, we will not have sizeable credit

losses in relation to the amount reserved. We may need to

significantly adjust the allowance for credit losses, considering

current factors at the time, including economic or market

conditions and ongoing internal and external examination

processes. Our process for determining the adequacy of the

allowance for credit losses is discussed in “Financial Review

– Critical Accounting Policies – Allowance for Credit Losses”

and Note 6 (Loans and Allowance for Credit Losses) to

Financial Statements.

Asset/Liability and Market Risk Management

Asset/liability management involves the evaluation, monitoring

and management of interest rate risk, market risk, liquidity

and funding. The Corporate Asset/Liability Management

Committee (Corporate ALCO)—which oversees these risks

and reports periodically to the Finance Committee of the

Board of Directors—consists of senior financial and business

executives. Each of our principal business groups has indi-

vidual asset/liability management committees and processes

linked to the Corporate ALCO process.

INTEREST RATE RISK

Interest rate risk, which potentially can have a significant

earnings impact, is an integral part of being a financial

intermediary. We are subject to interest rate risk because:

• assets and liabilities may mature or reprice at different

times (for example, if assets reprice faster than liabilities

and interest rates are generally falling, earnings will

initially decline);

• assets and liabilities may reprice at the same time but by

different amounts (for example, when the general level

of interest rates is falling, we may reduce rates paid on

checking and savings deposit accounts by an amount that

is less than the general decline in market interest rates);

• short-term and long-term market interest rates may

change by different amounts (for example, the shape of

the yield curve may affect new loan yields and funding

costs differently); or

• the remaining maturity of various assets or liabilities may

shorten or lengthen as interest rates change (for example,

if long-term mortgage interest rates decline sharply,

mortgage-backed securities held in the securities available-

for-sale portfolio may prepay significantly earlier than

anticipated—which could reduce portfolio income).

Interest rates may also have a direct or indirect effect on

loan demand, credit losses, mortgage origination volume, the

fair value of MSRs and other financial instruments, the value

of the pension liability and other items affecting earnings.

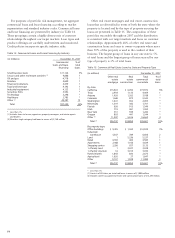

Table 18: Allocation of the Allowance for Credit Losses

(in millions) December 31,

2007 2006 2005 2004 2003

Loans Loans Loans Loans Loans

as % as % as % as % as %

of total of total of total of total of total

loans loans loans loans loans

Commercial and commercial real estate:

Commercial $1,137 24% $1,051 22% $ 926 20% $ 940 19% $ 917 19%

Other real estate mortgage 288 9 225 9 253 9 298 11 444 11

Real estate construction 156 5 109 5 115 4 46 3 63 3

Lease financing 51 2 40 2 51 2 30 2 40 2

Total commercial and commercial real estate 1,632 40 1,425 38 1,345 35 1,314 35 1,464 35

Consumer:

Real estate 1-4 family first mortgage 415 19 186 17 229 25 150 31 176 33

Real estate 1-4 family junior lien mortgage 1,329 20 168 21 118 19 104 18 92 15

Credit card 834 5 606 5 508 4 466 4 443 3

Other revolving credit and installment 1,164 14 1,434 17 1,060 15 889 11 802 13

Total consumer 3,742 58 2,394 60 1,915 63 1,609 64 1,513 64

Foreign 144 2 145 2 149 2 139 1 95 1

Total allocated 5,518 100% 3,964 100% 3,409 100% 3,062 100% 3,072 100%

Unallocated component of allowance — — 648 888 819

Total $5,518 $3,964 $4,057 $3,950 $3,891