Wells Fargo 2007 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

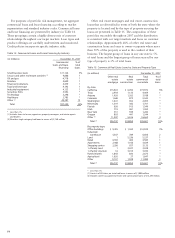

61

We assess interest rate risk by comparing our most likely

earnings plan with various earnings simulations using many

interest rate scenarios that differ in the direction of interest

rate changes, the degree of change over time, the speed of

change and the projected shape of the yield curve. For example,

as of December 31, 2007, our most recent simulation indicated

estimated earnings at risk of approximately 4% of our most

likely earnings plan over the next 12 months using a scenario

in which the federal funds rate rises 175 basis points to 6%

and the 10-year Constant Maturity Treasury bond yield rises

300 basis points to 7%. Simulation estimates depend on, and

will change with, the size and mix of our actual and projected

balance sheet at the time of each simulation. Due to timing

differences between the quarterly valuation of MSRs and the

eventual impact of interest rates on mortgage banking volumes,

earnings at risk in any particular quarter could be higher than

the average earnings at risk over the 12-month simulation

period, depending on the path of interest rates and on our

hedging strategies for MSRs. See “Mortgage Banking

Interest Rate and Market Risk” below.

We use exchange-traded and over-the-counter interest rate

derivatives to hedge our interest rate exposures. The notional

or contractual amount, credit risk amount and estimated net

fair value of these derivatives as of December 31, 2007 and

2006, are presented in Note 16 (Derivatives) to Financial

Statements. We use derivatives for asset/liability management

in three main ways:

• to convert a major portion of our long-term fixed-rate

debt, which we issue to finance the Company, from

fixed-rate payments to floating-rate payments by

entering into receive-fixed swaps;

• to convert the cash flows from selected asset and/or

liability instruments/portfolios from fixed-rate payments

to floating-rate payments or vice versa; and

• to hedge our mortgage origination pipeline, funded

mortgage loans and MSRs using interest rate swaps,

swaptions, futures, forwards and options.

MORTGAGE BANKING INTEREST RATE AND MARKET RISK

We originate, fund and service mortgage loans, which subjects

us to various risks, including credit, liquidity and interest rate

risks. We reduce unwanted credit and liquidity risks by selling

or securitizing predominantly all of the long-term fixed-rate

mortgage loans we originate and most of the ARMs we orig-

inate. From time to time, we hold originated ARMs in our

loan portfolio as an investment for our growing base of core

deposits. We determine whether the loans will be held for

investment or held for sale at the time of commitment. We

may subsequently change our intent to hold loans for invest-

ment and sell some or all of our ARMs as part of our corpo-

rate asset/liability management. We may also acquire and

add to our securities available for sale a portion of the secu-

rities issued at the time we securitize mortgages held for sale.

2007 was a challenging year for the financial services

industry with the downturn in the national housing market,

deterioration in the capital markets, widening credit spreads

and increases in market volatility, in addition to changes in

interest rates discussed in the following sections. Notwithstanding

the sharp downturn in the housing sector, the widening of

nonconforming credit spreads and the lack of liquidity in the

nonconforming secondary markets, our mortgage banking

revenue grew, reflecting the complementary origination and

servicing strengths of the business. The secondary market for

agency-conforming mortgages functioned well for most of

the year. However, secondary market spreads widened during

the second half of 2007. The mortgage warehouse and

pipeline, which predominantly consists of prime mortgage

loans, was written down by $479 million in 2007 to reflect

the unusual widening in nonconforming and conforming

agency market spreads. In addition to the write-down associ-

ated with the mortgage warehouse and pipeline, we further

reduced mortgage origination gains by $324 million primarily

to reflect a write-down of mortgage loans repurchased during

the year, as well as an increase to the repurchase reserve for

projected early payment defaults.

Interest rate and market risk can be substantial in the

mortgage business. Changes in interest rates may potentially

impact total origination and servicing fees, the value of our

residential MSRs measured at fair value, the value of MHFS

and the associated income and loss reflected in mortgage

banking noninterest income, the income and expense associ-

ated with instruments (economic hedges) used to hedge

changes in the fair value of MSRs and MHFS, and the value

of derivative loan commitments (interest rate “locks”)

extended to mortgage applicants.

Interest rates impact the amount and timing of origination

and servicing fees because consumer demand for new mort-

gages and the level of refinancing activity are sensitive to

changes in mortgage interest rates. Typically, a decline in

mortgage interest rates will lead to an increase in mortgage

originations and fees and may also lead to an increase in ser-

vicing fee income, depending on the level of new loans added

to the servicing portfolio and prepayments. Given the time it

takes for consumer behavior to fully react to interest rate

changes, as well as the time required for processing a new

application, providing the commitment, and securitizing and

selling the loan, interest rate changes will impact origination

and servicing fees with a lag. The amount and timing of the

impact on origination and servicing fees will depend on the

magnitude, speed and duration of the change in interest rates.

Under FAS 159, which we adopted January 1, 2007, we

elected to measure MHFS at fair value prospectively for new

prime MHFS originations for which an active secondary mar-

ket and readily available market prices currently exist to reli-

ably support fair value pricing models used for these loans.

We also elected to measure at fair value certain of our other

interests held related to residential loan sales and securitiza-

tions. We believe that the election for new prime MHFS and

other interests held (which are now hedged with free-standing

derivatives (economic hedges) along with our MSRs) will

reduce certain timing differences and better match changes in

the value of these assets with changes in the value of deriva-

tives used as economic hedges for these assets. Loan origina-

tion fees are recorded when earned, and related direct loan

origination costs and fees are recognized when incurred.