Wells Fargo 2007 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

52

In addition, in securities available for sale, we held

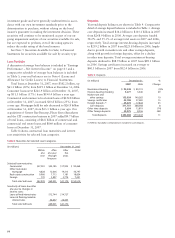

approximately $1,735 million in tax-exempt bonds at

December 31, 2007, in the form of CDOs, consolidated

in our balance sheet with related liabilities, based on the

Company’s participation in certain municipal tender option

bond programs. The fair value includes a $69 million net

unrealized loss due to changes in interest rates which is

expected to be recovered over time. Approximately 98%

of the bonds are rated investment grade while 2% are not

rated. Under the municipal tender option bond programs

in which we participate, we place long-term tax-exempt

municipal bonds in a trust sponsored by a third party which

serves as the collateral for short-term tender option bonds

issued by the trust to investors. These tender option bonds

can be “put” or tendered by the investor to the trust at par

at predetermined times (generally weekly or monthly). We

are required to consolidate the trusts in accordance with

FIN 46R. We earn a spread between the long-term rate on

the municipal bonds and the short-term rate on the corre-

sponding tender option bonds.

For more information on securitizations, including sales

proceeds and cash flows from securitizations, see Note 8

(Securitizations and Variable Interest Entities) to Financial

Statements.

Our money market mutual funds are allowed to hold

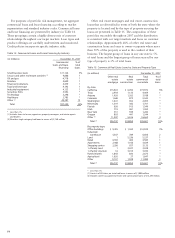

investments in SIVs in accordance with approved investment

parameters for the respective funds and, therefore, may have

indirect exposure to CDOs. At December 31, 2007, our

money market mutual funds held $106 billion of assets

under management including investments in eight SIVs not

sponsored by the Company aggregating $1.6 billion, or

1.5% of the funds’ assets. Based on the maturity and pay-

down of these investments, by February 1, 2008, the funds

held three SIVs aggregating $1.0 billion. At February 1,

2008, the remaining assets held by the money market funds

were either U.S. government, high-grade municipal, or high-

grade corporate securities. At such time, to maintain an

investment rating of AAA for certain funds, we elected to

enter into a capital support agreement for up to $130 million

related to one SIV held by our AAA-rated non-government

money market mutual funds. We are generally not responsible

for investment losses incurred by our funds, and we do not

have a contractual or implicit obligation to indemnify such

losses or provide additional support to the funds. Based on

our estimate of the guarantee obligation at the time we entered

into the agreement, we recorded a liability of $39 million in

2008. While we elected to enter into the capital support

agreement for the AAA-rated funds, we are not obligated

and may elect not to provide additional support to these

funds or other funds in the future.

Wells Fargo Home Mortgage (Home Mortgage), in the

ordinary course of business, originates a portion of its mort-

gage loans through unconsolidated joint ventures in which

we own an interest of 50% or less. Loans made by these

joint ventures are funded by Wells Fargo Bank, N.A. through

an established line of credit and are subject to specified

underwriting criteria. At December 31, 2007, the total assets

of these mortgage origination joint ventures were approxi-

mately $55 million. We provide liquidity to these joint ven-

tures in the form of outstanding lines of credit and, at

December 31, 2007, these liquidity commitments totaled

$238 million.

We also hold interests in other unconsolidated joint

ventures formed with unrelated third parties to provide

efficiencies from economies of scale. A third party manages

our real estate lending services joint ventures and provides

customers title, escrow, appraisal and other real estate related

services. Our merchant services joint venture includes credit

card processing and related activities. At December 31, 2007,

total assets of our real estate lending and merchant services

joint ventures were approximately $775 million.

In connection with certain brokerage, asset management,

insurance agency and other acquisitions we have made, the

terms of the acquisition agreements provide for deferred

payments or additional consideration, based on certain

performance targets. At December 31, 2007, the amount

of additional consideration we expected to pay was not

significant to our financial statements.

As a financial services provider, we routinely commit to

extend credit, including loan commitments, standby letters of

credit and financial guarantees. A significant portion of com-

mitments to extend credit may expire without being drawn

upon. These commitments are subject to the same credit

policies and approval process used for our loans. For more

information, see Note 6 (Loans and Allowance for Credit

Losses) and Note 15 (Guarantees and Legal Actions) to

Financial Statements.

In our venture capital and capital markets businesses, we

commit to fund equity investments directly to investment

funds and to specific private companies. The timing of future

cash requirements to fund these commitments generally

depends on the related investment cycle, the period over

which privately-held companies are funded by investors and

ultimately sold or taken public. This cycle can vary based on

market conditions and the industry in which the companies

operate. We expect that many of these investments will become

public, or otherwise become liquid, before the balance of

unfunded equity commitments is used. At December 31, 2007,

these commitments were approximately $895 million. Our

other investment commitments, principally related to affordable

housing, civic and other community development initiatives,

were approximately $685 million at December 31, 2007.

In the ordinary course of business, we enter into

indemnification agreements, including underwriting agree-

ments relating to our securities, securities lending, acquisi-

tion agreements, and various other business transactions

or arrangements. For more information, see Note 15

(Guarantees and Legal Actions) to Financial Statements.