Wells Fargo 2007 Annual Report Download - page 109

Download and view the complete annual report

Please find page 109 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

106

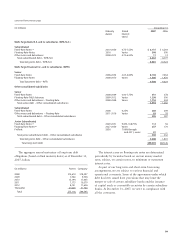

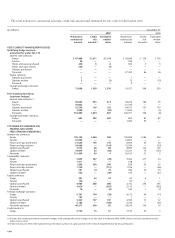

The fair value of commercial and commercial real estate

loans is calculated by discounting contractual cash flows using

discount rates that reflect our current pricing for loans with

similar characteristics and remaining maturity.

For real estate 1-4 family first and junior lien mortgages,

fair value is calculated by discounting contractual cash flows,

adjusted for prepayment and credit loss estimates, using dis-

count rates based on current industry pricing (where readily

available) or our own estimate of an appropriate risk-adjusted

discount rate for loans of similar size, type, remaining maturity

and repricing characteristics.

For credit card loans, the portfolio’s yield is equal to our

current pricing and, therefore, the fair value is equal to book

value adjusted for estimates of credit losses inherent in the

portfolio at the balance sheet date.

For all other consumer loans, the fair value is generally

calculated by discounting the contractual cash flows, adjusted

for prepayment and credit loss estimates, based on the current

rates we offer for loans with similar characteristics.

Loan commitments, standby letters of credit and commer-

cial and similar letters of credit not included in the following

table had contractual values of $241.9 billion, $12.5 billion

and $955 million, respectively, at December 31, 2007, and

$216.5 billion, $12.0 billion and $801 million, respectively,

at December 31, 2006. These instruments generate ongoing

fees at our current pricing levels, which are recognized over

the term of the commitment period. Of the commitments at

December 31, 2007, 40% mature within one year. Deferred

fees on commitments and standby letters of credit totaled

$33 million and $39 million at December 31, 2007 and

2006, respectively. The fair value of these instruments is

estimated based upon fees charged for similar agreements.

The carrying value of the deferred fees is a reasonable

estimate of the fair value of the commitments.

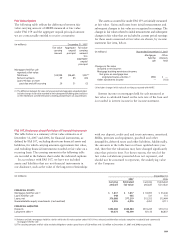

DERIVATIVES Quoted market prices are available and used

for our exchange-traded derivatives, such as certain interest

rate futures and option contracts, which we classify as

Level 1. However, substantially all of our derivatives are

traded in over-the-counter markets where quoted market

prices are not readily available. For those derivatives, we

measure fair value using internally developed models that

use primarily market observable inputs, such as yield curves

and option volatilities, and, accordingly, classify as Level 2.

Examples of Level 2 derivatives are basic interest rate swaps

and forward contracts. Any remaining derivative fair value

measurements using significant assumptions that are

unobservable we classify as Level 3. Level 3 derivatives

include interest rate lock commitments written for our

residential mortgage loans that we intend to sell.

MORTGAGE SERVICING RIGHTS AND CERTAIN OTHER INTERESTS HELD

IN SECURITIZATIONS Mortgage servicing rights (MSRs) and

certain other interests held in securitizations (e.g., interest-only

strips) do not trade in an active market with readily observable

prices. Accordingly, we determine the fair value of MSRs

SECURITIES AVAILABLE FOR SALE Securities available for sale

are recorded at fair value on a recurring basis. Fair value

measurement is based upon quoted prices, if available. If

quoted prices are not available, fair values are measured

using independent pricing models or other model-based

valuation techniques such as the present value of future cash

flows, adjusted for the security’s credit rating, prepayment

assumptions and other factors such as credit loss assumptions.

Level 1 securities include those traded on an active exchange,

such as the New York Stock Exchange, as well as U.S.

Treasury, other U.S. government and agency mortgage-

backed securities that are traded by dealers or brokers in

active over-the-counter markets. Level 2 securities include

private collateralized mortgage obligations, municipal bonds

and corporate debt securities. Securities classified as Level 3

are primarily private placement asset-backed securities where

we underwrite the underlying collateral (auto lease receivables)

and residual certificated interests in our residential mortgage

loan securitizations.

MORTGAGES HELD FOR SALE (MHFS) Under FAS 159, we elected

to carry our new prime residential MHFS portfolio at fair

value. The remaining MHFS are carried at the lower of cost

or market value. Fair value is based on independent quoted

market prices, where available, or the prices for other

mortgage whole loans with similar characteristics. As

necessary, these prices are adjusted for typical securitization

activities, including servicing value, portfolio composition,

market conditions and liquidity. Nearly all of our MHFS

are classified as Level 2. For a minor portion where

market pricing data is not available, we use a discounted

cash flow model to estimate fair value and, accordingly,

classify as Level 3.

LOANS HELD FOR SALE Loans held for sale are carried at the

lower of cost or market value. The fair value of loans held

for sale is based on what secondary markets are currently

offering for portfolios with similar characteristics. As such,

we classify loans subjected to nonrecurring fair value

adjustments as Level 2.

LOANS For the carrying value of loans, see Note 1 – Loans.

We do not record loans at fair value on a recurring basis.

As such, valuation techniques discussed herein for loans are

primarily for estimating fair value for FAS 107 disclosure

purposes. However, from time to time, we record nonrecurring

fair value adjustments to loans to reflect (1) partial write-

downs that are based on the observable market price or

current appraised value of the collateral, or (2) the full

charge-off of the loan carrying value.

The fair value estimates for FAS 107 purposes differentiates

loans based on their financial characteristics, such as product

classification, loan category, pricing features and remaining

maturity. Prepayment and credit loss estimates are evaluated

by product and loan rate.