Wells Fargo 2007 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

46

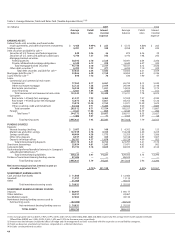

Table 4: Analysis of Changes in Net Interest Income

(in millions) Year ended December 31,

2007 over 2006 2006 over 2005

Volume Rate Total Volume Rate Total

Increase (decrease) in interest income:

Federal funds sold, securities purchased under resale

agreements and other short-term investments $ (52) $ 10 $ (42) $ 2 $ 99 $ 101

Trading assets (30) (27) (57) (17) 72 55

Debt securities available for sale:

Securities of U.S. Treasury and federal agencies (2) (1) (3) (5) 6 1

Securities of U.S. states and political subdivisions 117 (20) 97 (13) (8) (21)

Mortgage-backed securities:

Federal agencies 102 20 122 1,040 4 1,044

Private collateralized mortgage obligations (5) (26) (31) 93 54 147

Other debt securities 83038 173 — 173

Mortgages held for sale (634) 38 (596) 230 303 533

Loans held for sale 21 2 23 (146) 47 (99)

Loans:

Commercial and commercial real estate:

Commercial 1,001 26 1,027 529 860 1,389

Other real estate mortgage 248 18 266 16 296 312

Real estate construction 167 (21) 146 278 157 435

Lease financing 28 7 35 12 (10) 2

Consumer:

Real estate 1-4 family first mortgage 292 (11) 281 (1,441) 607 (834)

Real estate 1-4 family junior lien mortgage 634 91 725 620 827 1,447

Credit card 448 37 485 247 108 355

Other revolving credit and installment 339 57 396 730 365 1,095

Foreign 116 (47) 69 205 (55) 150

Other 2 1 3 (10) 10 —

Total increase in interest income 2,800 184 2,984 2,543 3,742 6,285

Increase (decrease) in interest expense:

Deposits:

Interest-bearing checking 23 14 37 12 60 72

Market rate and other savings 345 535 880 75 1,276 1,351

Savings certificates 343 164 507 337 273 610

Other time deposits (1,134) (38) (1,172) 167 530 697

Deposits in foreign offices 732 (6) 726 376 220 596

Short-term borrowings 211 42 253 (88) 336 248

Long-term debt 465 235 700 186 1,072 1,258

Total increase in interest expense 985 946 1,931 1,065 3,767 4,832

Increase (decrease) in net interest income

on a taxable-equivalent basis $ 1,815 $(762) $ 1,053 $ 1,478 $ (25) $1,453

Table 4 allocates the changes in net interest income on

a taxable-equivalent basis to changes in either average

balances or average rates for both interest-earning assets

and interest-bearing liabilities. Because of the numerous

simultaneous volume and rate changes during any period,

it is not possible to precisely allocate such changes between

volume and rate. For this table, changes that are not solely

due to either volume or rate are allocated to these categories

in proportion to the percentage changes in average volume

and average rate.

Noninterest Income

We earn trust, investment and IRA fees from managing and

administering assets, including mutual funds, corporate trust,

personal trust, employee benefit trust and agency assets. At

December 31, 2007, these assets totaled $1.12 trillion, up 14%

from $983 billion at December 31, 2006. Trust, investment

and IRA fees are primarily based on a tiered scale relative to

the market value of the assets under management or admin-

istration. The 13% increase in these fees in 2007 from 2006

was due to continued strong asset growth across all the trust

and investment management businesses.

We also receive commissions and other fees for providing

services to full-service and discount brokerage customers.

At December 31, 2007 and 2006, brokerage assets totaled

$131 billion and $115 billion, respectively. Generally, these

fees include transactional commissions, which are based

on the number of transactions executed at the customer’s

direction, or asset-based fees, which are based on the market

value of the customer’s assets. A significant portion of the

20% increase in these fees in 2007 from a year ago was due

to higher securities issuance and investment banking activity.

Card fees increased 22% to $2,136 million in 2007 from

$1,747 million in 2006, primarily due to an increase in the

percentage of our customer base using a Wells Fargo credit

card and to higher credit and debit card transaction volume.

Purchase volume on these cards increased 19% from a year

ago and average card balances were up 28%.