Wells Fargo 2007 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

101

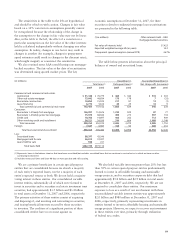

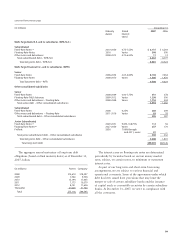

Our approach to managing interest rate risk includes the

use of derivatives. This helps minimize significant, unplanned

fluctuations in earnings, fair values of assets and liabilities,

and cash flows caused by interest rate volatility. This

approach involves modifying the repricing characteristics of

certain assets and liabilities so that changes in interest rates

do not have a significant adverse effect on the net interest

margin and cash flows. As a result of interest rate fluctuations,

hedged assets and liabilities will gain or lose market value.

In a fair value hedging strategy, the effect of this unrealized

gain or loss will generally be offset by the gain or loss on the

derivatives linked to the hedged assets and liabilities. In a

cash flow hedging strategy, we manage the variability of cash

payments due to interest rate fluctuations by the effective use

of derivatives linked to hedged assets and liabilities.

We use derivatives as part of our interest rate risk

management, including interest rate swaps, caps and floors,

futures and forward contracts, and options. We also offer

various derivatives, including interest rate, commodity, equity,

credit and foreign exchange contracts, to our customers but

usually offset our exposure from such contracts by purchasing

other financial contracts. The customer accommodations and

any offsetting financial contracts are treated as free-standing

derivatives. Free-standing derivatives also include derivatives

we enter into for risk management that do not otherwise

qualify for hedge accounting, including economic hedge

derivatives. To a lesser extent, we take positions based on

market expectations or to benefit from price differentials

between financial instruments and markets. Additionally,

free-standing derivatives include embedded derivatives

that are required to be separately accounted for from their

host contracts.

By using derivatives, we are exposed to credit risk if

counterparties to financial instruments do not perform as

expected. If a counterparty fails to perform, our credit risk

is equal to the fair value gain in a derivative contract. We

minimize credit risk through credit approvals, limits and

monitoring procedures. Credit risk related to derivatives is

considered and, if material, provided for separately. As we

generally enter into transactions only with counterparties

that carry high quality credit ratings, losses from counterparty

nonperformance on derivatives have not been significant.

Further, we obtain collateral, where appropriate, to reduce

risk. To the extent the master netting arrangements and

other criteria meet the requirements of FASB Interpretation

No. 39, Offsetting of Amounts Related to Certain Contracts,

as amended by FASB Interpretation No. 41, Offsetting

of Amounts Related to Certain Repurchase and Reverse

Repurchase Agreements, amounts are shown net in the

balance sheet.

Our derivative activities are monitored by Corporate

ALCO. Our Treasury function, which includes asset/liability

management, is responsible for various hedging strategies

developed through analysis of data from financial models

and other internal and industry sources. We incorporate the

resulting hedging strategies into our overall interest rate risk

management and trading strategies.

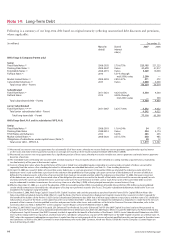

Fair Value Hedges

Prior to January 1, 2006, we used derivatives as fair value

hedges to manage the risk of changes in the fair value of

residential MSRs and other interests held. These derivatives

included interest rate swaps, swaptions, Eurodollar and

Treasury futures and options, and forward contracts.

Derivative gains or losses caused by market conditions

(volatility) and the spread between spot and forward rates

priced into the derivative contracts (the passage of time)

were excluded from the evaluation of hedge effectiveness,

but were reflected in earnings. Upon adoption of FAS 156,

derivatives used to hedge our residential MSRs are no longer

accounted for as fair value hedges under FAS 133, but as

economic hedges. Net derivative gains and losses related to

our residential mortgage servicing activities are included in

“Servicing income, net” in Note 9.

We use interest rate swaps to convert certain of our fixed-

rate long-term debt and certificates of deposit to floating

rates to hedge our exposure to interest rate risk. We also

enter into cross-currency swaps and cross-currency interest

rate swaps to hedge our exposure to foreign currency risk

and interest rate risk associated with the issuance of non-

U.S. dollar denominated long-term debt. Prior to January 1,

2007, the ineffective portion of these fair value hedges was

recorded as part of interest expense in the income statement.

Subsequent to January 1, 2007, the ineffective portion of

Note 16: Derivatives

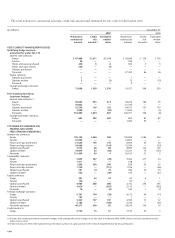

predecessors (collectively Visa) and certain other member

banks of the Visa USA network, (2) litigation, and (3) an

escrow account that will be established by Visa Inc. at the

time of its IPO. The escrow account will be funded from IPO

proceeds and will be used to make payments related to Visa

litigation. We recorded litigation liabilities associated with

indemnification obligations related to agreements entered

into during second quarter 2006 and third quarter 2007.

Based on our proportionate membership share of Visa USA,

we recorded a litigation liability and corresponding expense

of $95 million for 2006 and $203 million for 2007. The

effect to the second quarter 2006 was estimated based

upon our share of an actual settlement reached in November

2007. Management does not believe that the fair value of

this obligation if determined in second quarter 2006 would

have been materially different given information available

at that time. Management has concluded, and the Audit

and Examination Committee of our Board of Directors

has concurred, that these amounts are immaterial to the

periods affected.