Wells Fargo 2007 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2007 Wells Fargo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

|

|

105

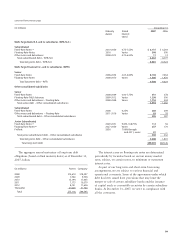

Note 17: Fair Values of Assets and Liabilities

We use fair value measurements to record fair value

adjustments to certain assets and liabilities and to determine

fair value disclosures. Trading assets, securities available for

sale, derivatives, prime residential mortgages held for sale

(MHFS) and residential MSRs are recorded at fair value on

a recurring basis. Additionally, from time to time, we may

be required to record at fair value other assets on a nonre-

curring basis, such as nonprime residential and commercial

MHFS, loans held for sale, loans held for investment and

certain other assets. These nonrecurring fair value adjustments

typically involve application of lower-of-cost-or-market

accounting or write-downs of individual assets.

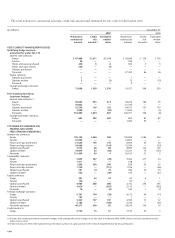

Effective January 1, 2007, upon adoption of FAS 159,

The Fair Value Option for Financial Assets and Financial

Liabilities, including an amendment of FASB Statement No.

115 (FAS 159), we elected to measure MHFS at fair value

prospectively for new prime residential MHFS originations

for which an active secondary market and readily available

market prices currently exist to reliably support fair value

pricing models used for these loans. We also elected to

remeasure at fair value certain of our other interests held

related to residential loan sales and securitizations. We

believe the election for MHFS and other interests held

(which are now hedged with free-standing derivatives

(economic hedges) along with our MSRs) will reduce certain

timing differences and better match changes in the value of

these assets with changes in the value of derivatives used as

economic hedges for these assets. There was no transition

adjustment required upon adoption of FAS 159 for MHFS

because we continued to account for MHFS originated prior

to 2007 at the lower of cost or market value. At December 31,

2006, the book value of other interests held was equal to

fair value and, therefore, a transition adjustment was

not required.

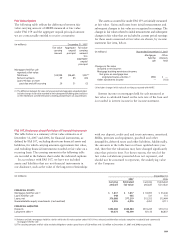

Upon adoption of FAS 159, we were also required to

adopt FAS 157, Fair Value Measurements (FAS 157). FAS

157 defines fair value, establishes a consistent framework for

measuring fair value and expands disclosure requirements

for fair value measurements. Additionally, FAS 157 amended

FAS 107, Disclosure about Fair Value of Financial

Instruments (FAS 107), and, as such, we follow FAS 157

in determination of FAS 107 fair value disclosure amounts.

The disclosures required under FAS 159, FAS 157 and

FAS 107 have been included in this Note.

Fair Value Hierarchy

Under FAS 157, we group our assets and liabilities at fair

value in three levels, based on the markets in which the

assets and liabilities are traded and the reliability of the

assumptions used to determine fair value. These levels are:

• Level 1 – Valuation is based upon quoted prices for

identical instruments traded in active markets.

• Level 2 – Valuation is based upon quoted prices for

similar instruments in active markets, quoted prices for

identical or similar instruments in markets that are not

active, and model-based valuation techniques for which

all significant assumptions are observable in the market.

• Level 3 – Valuation is generated from model-based

techniques that use significant assumptions not observable

in the market. These unobservable assumptions reflect our

own estimates of assumptions that market participants

would use in pricing the asset or liability. Valuation

techniques include use of option pricing models, discounted

cash flow models and similar techniques.

Determination of Fair Value

Under FAS 157, we base our fair values on the price that

would be received to sell an asset or paid to transfer a

liability in an orderly transaction between market participants

at the measurement date. It is our policy to maximize the use

of observable inputs and minimize the use of unobservable

inputs when developing fair value measurements, in accordance

with the fair value hierarchy in FAS 157.

Fair value measurements for assets and liabilities where

there exists limited or no observable market data and,

therefore, are based primarily upon our own estimates,

are often calculated based on current pricing policy, the

economic and competitive environment, the characteristics

of the asset or liability and other such factors. Therefore,

the results cannot be determined with precision and may

not be realized in an actual sale or immediate settlement

of the asset or liability. Additionally, there may be inherent

weaknesses in any calculation technique, and changes in the

underlying assumptions used, including discount rates and

estimates of future cash flows, that could significantly affect

the results of current or future values.

Following is a description of valuation methodologies

used for assets and liabilities recorded at fair value and for

estimating fair value for financial instruments not recorded

at fair value (FAS 107 disclosures).

Assets

SHORT-TERM FINANCIAL ASSETS Short-term financial assets

include cash and due from banks, federal funds sold and

securities purchased under resale agreements and due from

customers on acceptances. These assets are carried at

historical cost. The carrying amount is a reasonable estimate

of fair value because of the relatively short time between the

origination of the instrument and its expected realization.

TRADING ASSETS Trading assets are recorded at fair value and

consist primarily of securities and derivatives held for trading

purposes. The valuation method for trading securities is the same

as the methodology used for securities classified as available for

sale (see the following page). The valuation methodology for

derivatives is described in the following Derivatives section.