Volvo 2006 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2006 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

An industry in flux

The transport industry is moving through a process of change in which

increasingly stringent environmental standards are a major driving force.

Substantial investments are required for R&D programs involving new tech-

nologies to reduce emissions from vehicles and for the development of

alternative fuels and drivelines. To meet these challenges, consolidation is

in progress among manufacturers through mergers and acquisitions.

In mature markets in the US and Europe, consolidation in the truck indus-

try has been in progress over a number of decades and has made substan-

tial progress. In other regions or sectors – such as Asia or the construction

industry – the pressure to consolidate is expected to increase.

Meanwhile, new competitors have emerged as major regional players in

growth markets with the aim of becoming global players. Restructuring

creates the potential for the Volvo Group to further strengthen its positions

in each business area by means of acquisitions.

Growth markets

The Volvo Group’s goal is to be the world’s leading supplier of commercial

transport solutions. Volvo currently has well-established positions in the

European and North American markets. However, the most rapid growth is

occurring in regions in which the Group had very limited operations ten or 15

years ago. The Volvo Group plans to expand in these markets – in Asia, for

example.

China and India are examples of markets that are already considerably

large and will prove even more important for the Volvo Group’s future growth.

In addition, Eastern European markets are showing steep growth and the

Group is well positioned to capitalize on expansion in these markets.

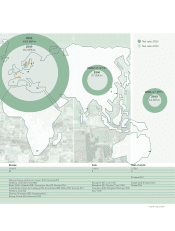

Heavy truck registrations, > 16 tons Three strong markets, heavy trucks

05 06030204

Europe

North America

295277255229229

349308249178180

Vehicles, thousands

Consolidation – European truck manufactures

Mercedes

Volvo

Gräf u .Stift

Lancia

Scania

Ford

BMC

Henschel

Willeme

Seddon

Guy

Steyr

Commer

Atkinson

Dennis

Unic

Saurer

Fiat

Leyland

Krupp

ÖAF

Berliet

Bussing

DAF

Magirus

Berna

OM

ERF

Astra

Hotchkiss

Barreiros

Bernard

Bedford

Saviem

Pegaso

FTF

Dodge

MAN

Foden

Volvo Group

DaimlerChrysler

Paccar

MAN

Scania

Iveco

1966 2006

A global group 2006 9