Volvo 2006 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2006 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

IFRS 2 Share-based Payments

Volvo has decided that the “new share-based incentive program”

adopted at the 2004 Annual General Meeting is covered by IFRS 2

Share-based payments. The impact, however, was limited. The IFRS

2 distinguishes between “cash-settled” and “equity-settled” compo-

nents of share-based payments, in Volvo cases, shares. The Volvo

program include both a cash-settled and an equity-settled part. The

equity-settled part was earlier accounted for at fair value and pro-

vided for as an accrued expense over the vesting period with a “true

up” each reporting date. According to IFRS 2 the fair value is deter-

mined at the grant-date, recognized as an expense during the vest-

ing period and credited to equity. Additional social costs are

reported as a liability and is revalued at each balance sheet day in

accordance with URA 46.

IFRS 5 Non-Current Asset Held for Sale

and Discontinued Operations

IFRS 5 is applied prospectively from January 1, 2005, according to

IFRS 1. Volvo had not identifi ed any non-current assets that could be

classifi ed held for sales and which would have had material impact

on the balance sheet as of December 31, 2004, and no effect has

been identifi ed in the 2004 income statement. Discontinued oper-

ations pertain to signifi cant operations, such as operating segments,

comprising one or more cash-generating units. The rules for discon-

tinued operations have not been applicable for Volvo during 2004

and 2005.

Other transition rules according to IFRS 1

and IFRS standards

In applying IFRS, Volvo had the possibility to chose to measure prop-

erty, plant and equipment at fair value. Volvo has chosen not to use

this possibility but continue the present valuation of property, plant

and equipment at historical cost less accumulated depreciation. The

same treatment is also used for investment properties. IFRS 1 pro-

vides an option how to treat the effects of Changes in Foreign

Exchange Rates, according to IAS 21. A fi r st time adopter of IFRS

could set the cumulative translation difference to zero for foreign

operations. Volvo has chosen this possibility and set the translation

difference to zero at January 1, 2004. Assumptions made under pre-

vious GAAP shall not be changed under the transition to IFRS

unless there is objective evidence that those were in error. Volvo has

made no changes in assumptions in the preparation of comparative

information prepared in accordance with IFRS. According to SIC 12,

Special Purpose Entities should be consolidated as from January 1,

2004. Volvo has not identifi ed any such Special Purpose Entities.

Defi nition of cash and cash equivalents in

presentation of cash-fl ow statements

Under Swedish GAAP, all investments in marketable debt securities

have been included in the defi nition of cash and cash equivalents for

the purpose of the cash-fl ow statement. In accordance with Volvo’s

fi n a ncial risk policy, all such securities should fulfi ll requirements

regarding low risk and high liquidity. Under IFRS, investments in mar-

ketable securities are excluded from the defi nition of cash and cash

equivalents for the purpose of the cash-fl ow statement if these

instruments have maturity dates beyond three months from the date

of investment. In the 2004 closing no marketable securities were

defi ned as cash equivalents according to IFRS. Classifi cation of cash

and cash equivalents in the cash-fl ow statement does not affect

Volvo’s net fi n ancial position.

In the transition to IFRS the following reclassifi cation is done in

the cash fl ow statement. Customer fi nance receivables, net, are

reported within Cash fl ow from operating activities, instead of as

previously being reported as Cash fl o w from investing activities.

Cash fl o w related to customer fi n ancing operations arises mainly

within Financial Services (VFS). Changes in customer fi nan cing are

currently reported in Volvo’s cash-fl ow statement with VFS consoli-

dated in accordance with the equity method as changes in working

capital, since Volvo’s operations excluding VFS do not have any sig-

nifi cant customer fi nancing operations. Changes in customer fi nanc-

ing operations are reported on a separate line in Volvo’s cash-fl ow

statement including VFS. Volvo’s reported Operating Cash-fl ow is

not affected by the reclassifi cation.

Classifi cation of leasing contracts in segment reporting

of Financial Services

In accordance with IFRS, operating lease contracts with end-cus-

tomers are in segment reporting for Financial Services reported as

fi n a ncial leasing contracts if the residual value in these contracts is

guaranteed to Financial Services by another Volvo business area. In

the Volvo Group’s consolidated balance sheet, these leasing agree-

ments are still reported as assets under operating lease. In compari-

son with the 2004 closing approximately SEK 12 billion is reclassi-

fi e d to fi nancial leases from operating leases in the Financial

Services segment reporting.

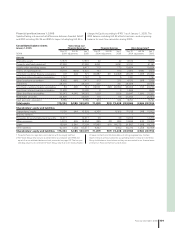

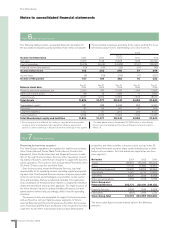

Cash-fl ow statement According to previous presentation Presentation according to IFRS

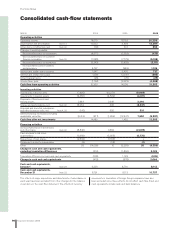

SEK billion 2004 2005 2004 2005

Operating activities

Operating income 14.7 18.2 14.7 18.2

Depreciation and amortization 10.0 9.9 10.0 9.9

Other non-cash items (0.1) 0.4 (0.1) 0.4

Change in working capital (1.4) (4.7) (1.4) (4.7)

Customer Finance receivables, net (7.4) (7.8)

Financial items and income taxes (0.5) (2.0) (0.5) (2.0)

Cash fl ow from operating activities 22.7 21.8 15.3 14.0

Investing activities

Investments in fi xed assets (7.4) (10.3) (7.4) (10.3)

Investment in leasing vehicles (4.4) (4.5) (4.4) (4.5)

Disposal of fi xed assets and leasing vehicles 2.4 2.6 2.4 2.6

Customer Finance receivables, net (7.4) (7.8)

Operating cash fl ow 5.9 1.8 5.9 1.8

Financial information 2006 99