Vodafone 2013 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2013 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

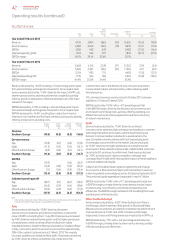

EBITDA grew by 10.3%*, with a 1.6* percentage point increase in EBITDA

margin, primarily driven by revenue growth in Vodacom’s mobile

operations outside South Africa and savings in network costs in South

Africa following investment in single RAN and transmission equipment.

Other AMAP

Organic service revenue decreased by -2.1%* with growth in Egypt,

Ghana and Qatar more than offset by revenue declines in Australia

and New Zealand. Australia continued to experience steep revenue

declines on the back of ongoing service perception issues and

a declining customer base. There has been a strong focus on network

improvement and arresting the weakness in brand perception. In Egypt

the launch of value management initiatives, take-up of data services

and the increase in international incoming call volumes and rates drove

service revenue growth of 3.7%*, despite competitive pressures and

the uncertain political environment. Data revenue continued to show

strong growth of 29.6%* and xed line revenue grew by 29.0%*. In Qatar

service revenue grew by 29.8%*, driven by the growth in the customer

base, which is now over one million, supported by successful new

propositions. In Ghana, continued strong growth in the customer base

and the success of integrated tariffs led to service revenue growth

of 24.2%*.

EBITDA declined by -2.6%*, with EBITDA margin remaining stable, with

the impact of service revenue declines in Australia and New Zealand

offsetting growth in Egypt, Qatar and Ghana.

References to “Q2” are to the quarter ended 30 September 2012, references to the “Q3” or “previous quarter”

are to the quarter ended 31 December 2013, and references to “Q4” and “fourth quarter” are to the quarter

ended 31 March 2013 unless otherwise stated. References to the “rst half of the year” are to the six months

ended 30 September 2012 and references to “H2” or the “second half of the year” are to the six months ended

31 March 2013 unless otherwise stated. References to the “year” or “nancial year” are to the nancial year

ended 31 March 2013, references to the “prior nancial year” are to the nancial year ended 31 March 2012,

and references to the “new nancial year” and “coming year” are to the nancial year ended 31 March 2014

unless otherwise stated. References to the”2012 nancial year”, “2013 nancial year”, the “2014 nancial year”,

the “2015 nancial year”, and the “2016 nancial year” are to the nancial years ended/ending 31 March 2012,

2013, 2014, 2015 and 2016, respectively.

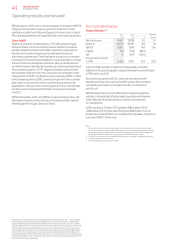

Non-Controlled Interests

Verizon Wireless1 2 3

2013

£m

2012

£m

% change

£Organic

Service revenue 19,697 18,039 9.2 8.1

Revenue 21,972 20,187 8.8 7.8

EBITDA 8,831 7,689 14.9 13.6

Interest (25) (212) (88.2)

Tax213 (287) (104.5)

Group’s share of result

in VZW 6,422 4,867 31.9 30.5

In the US VZW reported 5.9 million net mobile retail connection

additions in the year, bringing its closing mobile retail connection base

to 98.9 million, up 6.4%.

Service revenue growth of 8.1%* continued to be driven by the

expanding number of accounts and ARPA4 growth from increased

smartphone penetration and a higher number of connections

per account.

EBITDA margin improved, with efciencies in operating expenses

and direct costs partially offset by higher acquisition and retention

costs reecting the increased new connections and demand

for smartphones.

VZW’s net debt at 31 March 2013 totalled US$6.2 billion5 (2012:

US$6.4 billion5). During the year VZW paid a US$8.5 billion income

dividend to its shareholders and completed the acquisition of spectrum

licences for US$3.7 billion (net).

Notes:

1 All amounts represent the Group’s share based on its 45% equity interest, unless otherwise stated.

2 The Group’s share of the tax attributable to VZW relates only to the corporate entities held by the VZW

partnership and certain US state taxes which are levied on the partnership. The tax attributable to the

Group’s share of the partnership’s pre-tax prot is included within the Group tax charge.

3 The denition of “connections” reported by VZW is the same as “customers” as reported by Vodafone.

4 Average monthly revenue per account.

5 Net debt excludes pending credit card receipts.

Operating results (continued)

44 Vodafone Group Plc

Annual Report 2013