Vodafone 2013 Annual Report Download - page 16

Download and view the complete annual report

Please find page 16 of the 2013 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

Chief Executive’s review

Summary of where we are now.

a Further good progress on data: organic revenue

growth 13.8%*, European smartphone penetration

36% , up 9 percentage points year-on-year.

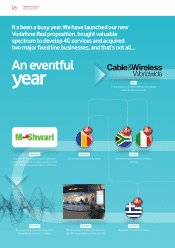

a Vodafone Red now in 14 markets; 4.1 million

customers as at 12 May 2013; 67% of consumer

contract revenue in our European markets

from integrated plans.

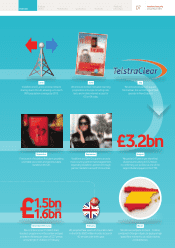

a Unied communications strategy accelerated:

acquisitions of CWW and TelstraClear;

bre deployment planned in Spain and Portugal.

a £2.4 billion dividend received from VZW

of which £1.5 billion is committed

to share buybacks.

Ready to seize

futuregrowth

opportunities

Even in the context of tough economic and regulatory

conditions, I remain very excited about the longer term

prospects for the industry, as customer appetite for

high speed data grows rapidly, and companies look to

embed mobility into their corporate strategies.

Financial review of the year

Performance was strong in our emerging

markets operations, with continued good

growth in revenue and improving margins.

However, the macroeconomic environment

in Southern Europe has been very challenging,

and European regulation continues to depress

returns in the industry, rather than incentivise

investment. VZW, our 45% owned associate

in the US, continued to achieve strong

growth in revenue, EBITDA, cash ow and

market share.

Overall, I am satised with the progress

we have made with our strategic priorities:

a We have launched Vodafone Red, our new

strategic approach to pricing and our

customer proposition, in 14 markets, with

very positive initial results;

a We remain competitive in all markets,

gaining or at least holding market share

in most of our operations;

a We have bought new low frequency

spectrum in a number of markets, and have

laid the technology platform for the rapid

deployment of HSPA+ and 4G/LTE services;

a We have accelerated the integration

of CWW and TelstraClear, two xed line

businesses acquired during the year,

advancing our enterprise and unied

communications strategies; and

a We have increased the ordinary dividend

per share by 7% for the third year in a row,

as well as buying back £1.6 billion of shares1.

Group revenue for the year was down -1.4%*

to £44.4 billion, with Group organic service

revenue down -1.9%*. Data revenue (+13.8%*)

and major emerging markets (India +10.7%*,

Vodacom +3.0%*, Turkey +17.3%*) continued

to perform strongly. Group EBITDA margin fell

-0.5* percentage points, or -0.1* percentage

points excluding restructuring costs, as the

impact of steep revenue declines in Southern

Europe offset improving margins in India

and Vodacom. Group EBITDA fell -3.1%*

to £13.3 billion, after restructuring costs

of £310 million.

Consumer 2015

Enterprise 2015

Network 2015

Operations 2015

14 Vodafone Group Plc

Annual Report 2013