Vodafone 2013 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2013 Vodafone annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

|

|

Chief Executive’s review (continued)

Verizon Wireless

VZW continued to trade very well, launching

successful new price plans and making further

market share gains. Organic service revenue

was up 8.1%* and EBITDA was up 13.6%*.

Free cash ow amounted to US$13.2 billion

(£8.4 billion), and net debt at 31 March 2013

was US$6.2 billion (£4.1 billion). Our share

of VZW’s prots for the year amounted

to £6.4 billion, up 30.5%* year-on-year.

Vodafone 2015

While the macroeconomic and regulatory

environment in Europe presents signicant

short-term challenges, we see a number

of positive developments. We expect

smartphone adoption to continue to grow

in all markets over the next three years, with

mobile applications and low cost smartphone

availability increasing in mature and emerging

markets alike.

With the broad deployment of high speed data

networks, both mobile and xed, we expect

customers’ appetite for data to increase

signicantly. At the same time, the evolution

of network and IT platforms should enable

lower cost and more standardised approaches

as we further integrate commercial and

technology planning.

As a result, we believe that the long-term

prospects for the mobile market are

highly attractive for those that make scale,

standardisation and the customer data

experience fundamental to how they operate.

Vodafone 2015 is our strategy to maximise

this opportunity.

Consumer 2015

We are adopting a new strategic approach

to consumer pricing and bundling in Europe,

in order to offer customers greater freedom

of usage and, at the same time, stabilise

ARPU. We have launched new plans across

much of our footprint, branded Vodafone Red

in most markets, which incorporate unlimited

voice and SMS, and generous data allowances.

As a result, we have radically simplied pricing,

giving clear visibility of the cost of ownership

and, enabling simplication of IT and billing.

We are progressively enhancing the value

proposition through the introduction

of a number of additional features, including

improved access to technical support,

attractive roaming packages, shared data

plans, early handset upgrades, storage and

back-up in the cloud, and device security,

to increase the breadth of service and support

ARPU over time.

Already, we have 4.1 million customers

on Vodafone Red plans3 across 14 markets.

The customer response has been very positive,

with strong net promoter scores. Data usage

on Vodafone Red plans is much higher,

as is the average return on our commercial

investment. As expected, we have seen

some ARPU dilution, but at a lower level than

planned. We aim to have ten million customers

on Vodafone Red plans by March 2014.

We also see an increasing move towards

residential unied communications services

in some of our European markets. We expect

this trend to grow, with cable operators

offering MVNO services, and incumbent

xed line providers combining their domestic

broadband services with mobile and TV plans.

Our goal is to offer unied communications

services in our major European markets,

accessing next generation xed line

infrastructure through a combination of

negotiated wholesale terms, deployment

ofour own bre and, potentially, acquisitions.

A clear regulatory framework with regard

toaccessing incumbent bre infrastructure

will be key.

In emerging markets, we aim to build on our

success to date to become a clear leader,

increasing the value of these markets to the

Group through market growth, improving

margins, share gains and stronger cash

generation. These markets offer very attractive

long-term opportunities from sustained GDP

growth, the scope for widespread mobile

data adoption and the fullment of unmet

needs such as basic nancial services. We aim

to maximise these opportunities through

superior marketing and distribution, smart

data pricing, the development of low-cost

smartphones and selective innovation in areas

in which we can truly differentiate.

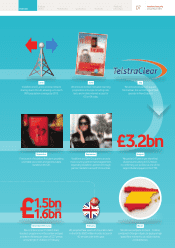

Enterprise 2015

We are strengthening our leading position

in enterprise, enhancing our product offering

to large and medium-sized businesses and

creating a dedicated enterprise operational

structure, following the market success

of Vodafone Global Enterprise (‘VGE’) and the

CWW and TelstraClear acquisitions. Enterprise

now represents 27.3% of Group service

revenue and we have over 32 million mobile

enterprise customers accounting for around

8% of our total customer base.

VGE, serving our biggest multi-national

accounts, will continue to expand its

remit, driven by an increasing appetite

among customers to consolidate telecoms

procurement cross-border and bring

mobility into the heart of their business

strategies. In unied communications,

we continue to develop Vodafone One Net

for small- and medium-sized companies,

and increasingly provide total communications

services to our larger customers through

the purchase of CWW. This acquisition will

also allow us to develop our product offering

in high growth segments, such as cloud

and hosting.

In machine-to-machine (‘M2M’), we intend

to leverage our new business unit organisation,

global technical platform and vertical sector

competences to exploit the current wave

of adoption of M2M solutions across many

industry and service sectors.

Network 2015

Our network strategy continues to focus

on supporting higher speed data in both

mature and emerging markets, and delivering

a consistently excellent data experience

to our customers through the widespread

deployment of HSPA+, LTE and high

capacity backhaul. We expect to continue

our consistent level of investment so that

Vodafone customers can be assured of

a video-standard data service across our

footprint in Europe and we can successfully

manage the high growth in data volumes

anticipated. We aim to extend our 3G footprint

at 43.2 Mbps and LTE coverage across our

ve major European markets to 80% and 40%

respectively by March 2015.

To complement our physical infrastructure

investment, we are committed to securing

the best portfolio of low frequency spectrum

to maintain and improve our strong market

positions through the improved customer

experience this will offer. During the year,

we acquired spectrum in the important

800 MHz band in the UK, the Netherlands,

Ireland, Romania and in the 1800 MHz band

in India, taking our total spectrum investment

to £7.9 billion in the last four years.

4.1m

of our customers are on our new strategic

Vodafone Red plans3, which we rst

launched in the UK in September 2012.

£6.4bn

our share of VZW prots for the year,

which represented 30.5%* year-on-year

growth.

16 Vodafone Group Plc

Annual Report 2013