Virgin Media 2013 Annual Report Download - page 51

Download and view the complete annual report

Please find page 51 of the 2013 Virgin Media annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

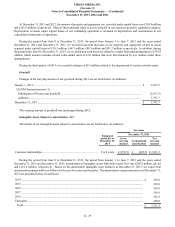

VIRGIN MEDIA INC.

(See note 1)

Notes to Consolidated Financial Statements — (Continued)

December 31, 2013, 2012 and 2011

II - 26

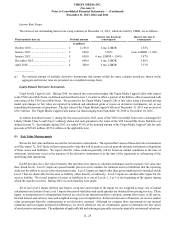

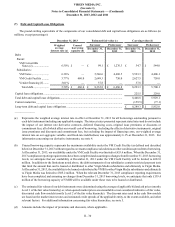

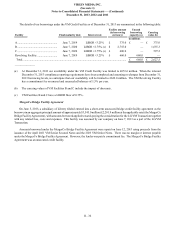

The recurring fair value measurement of our equity-related derivatives are based on binomial option pricing models, which

require the input of observable and unobservable variables such as exchange traded equity prices, risk-free interest rates, dividend

yields and forecasted volatilities of the underlying equity securities. The valuations of our equity-related derivatives are based on

a combination of Level 1 inputs (exchange traded equity prices), Level 2 inputs (interest rate futures and swap rates) and Level 3

inputs (forecasted volatilities). As changes in volatilities could have a significant impact on the overall valuations, we have

determined that these valuations fall under Level 3 of the fair value hierarchy. For the December 31, 2013 valuations of our equity-

related derivatives, we used estimated volatilities ranging from 25% to 27%. Based on the December 31, 2013 market price for

Liberty Global ordinary shares, changes in forecasted volatilities currently would not have a significant impact on the valuation

of the Virgin Media Capped Calls or the derivative embedded in the VM Convertible Notes, as defined and described in note 7.

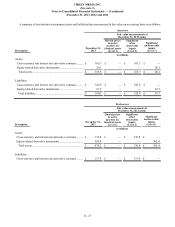

As further described in note 4, we have entered into various derivative instruments to manage our interest rate and foreign

currency exchange risk. The recurring fair value measurements of these derivative instruments are determined using discounted

cash flow models. Most of the inputs to these discounted cash flow models consist of, or are derived from, observable Level 2

data for substantially the full term of these derivative instruments. This observable data includes applicable interest rate futures

and swap rates, which are retrieved or derived from available market data. Although we may extrapolate or interpolate this data,

we do not otherwise alter this data in performing our valuations. We incorporate a credit risk valuation adjustment in our fair value

measurements to estimate the impact of both our own nonperformance risk and the nonperformance risk of our counterparties.

Our and our counterparties’ credit spreads are Level 3 inputs that are used to derive the credit risk valuation adjustments with

respect to our various interest rate and foreign currency derivative valuations. As we would not expect changes in our or our

counterparties’ credit spreads to have a significant impact on the valuations of these derivative instruments, we have determined

that these valuations fall under Level 2 of the fair value hierarchy. Our credit risk valuation adjustments with respect to our cross-

currency and interest rate swaps are quantified and further explained in note 4.

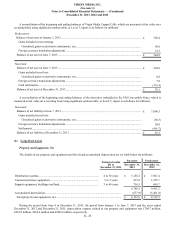

Fair value measurements are also used in connection with nonrecurring valuations performed in connection with impairment

assessments and acquisition accounting. These nonrecurring valuations include the valuation of customer relationship intangible

assets, property and equipment and the implied value of goodwill. The valuation of customer relationships is primarily based on

an excess earnings methodology, which is a form of a discounted cash flow analysis. The excess earnings methodology requires

us to estimate the specific cash flows expected from the customer relationship, considering such factors as estimated customer

life, the revenue expected to be generated over the life of the customer, contributory asset charges, and other factors. Tangible

assets are typically valued using a replacement or reproduction cost approach, considering factors such as current prices of the

same or similar equipment, the age of the equipment and economic obsolescence. The implied value of goodwill is determined

by allocating the fair value of a reporting unit to all of the assets and liabilities of that unit as if the reporting unit had been acquired

in a business combination, with the residual amount allocated to goodwill. All of our nonrecurring valuations use significant

unobservable inputs and therefore fall under Level 3 of the fair value hierarchy. During 2013, we performed nonrecurring valuations

for the LG/VM Transaction. We used a discount rate of 9.0% for our valuation of the customer relationships acquired as a result

of this acquisition. For additional information, see note 3.