Virgin Media 2013 Annual Report Download - page 134

Download and view the complete annual report

Please find page 134 of the 2013 Virgin Media annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139

|

|

III - 24

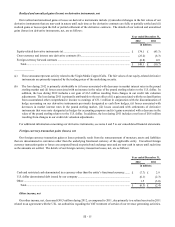

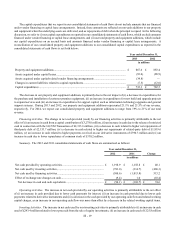

Nonrecurring Valuations. Our nonrecurring valuations are primarily associated with (i) the application of acquisition

accounting and (ii) impairment assessments, both of which require that we make fair value determinations as of the applicable

valuation date. In making these determinations, we are required to make estimates and assumptions that affect the recorded

amounts, including, but not limited to, expected future cash flows, market comparables and discount rates, remaining useful lives

of long-lived assets, replacement or reproduction costs of property and equipment and the amounts to be recovered in future periods

from acquired net operating losses and other deferred tax assets. To assist us in making these fair value determinations, we may

engage third-party valuation specialists. Our estimates in this area impact, among other items, the amount of depreciation and

amortization, impairment charges and income tax expense or benefit that we report. Our estimates of fair value are based upon

assumptions believed to be reasonable, but which are inherently uncertain. All of our long-lived assets were measured at fair value

on June 7, 2013 due to the application of acquisition accounting from the LG/VM Transaction and all of our long-lived assets are

subject to impairment assessments. For additional information, see notes 3, 5 and 6 to our consolidated financial statements.

Income Tax Accounting

We are required to estimate the amount of tax payable or refundable for the current year and the deferred tax assets and

liabilities for the future tax consequences attributable to differences between the financial statement carrying amounts and income

tax basis of assets and liabilities and the expected benefits of utilizing net operating loss and tax credit carryforwards, using enacted

tax rates in effect for each taxing jurisdiction in which we operate for the year in which those temporary differences are expected

to be recovered or settled. This process requires our management to make assessments regarding the timing and probability of

the ultimate tax impact of such items.

Net deferred tax assets are reduced by a valuation allowance if we believe it more-likely-than-not such net deferred tax assets

will not be realized. Establishing or reducing a tax valuation allowance requires us to make assessments about the timing of future

events, including the probability of expected future taxable income and available tax planning strategies. At December 31, 2013,

the aggregate valuation allowance provided against deferred tax assets was £2,866.6 million. The actual amount of deferred income

tax benefits realized in future periods will likely differ from the net deferred tax assets reflected in our December 31, 2013 balance

sheet due to, among other factors, possible future changes in income tax law or interpretations thereof in the jurisdictions in which

we operate and differences between estimated and actual future taxable income. Any of such factors could have a material effect

on our current and deferred tax positions as reported in our consolidated financial statements. A high degree of judgment is required

to assess the impact of possible future outcomes on our current and deferred tax positions.

Tax laws in jurisdictions in which we operate are subject to varied interpretation, and many tax positions we take are subject

to significant uncertainty regarding whether the position will be ultimately sustained after review by the relevant tax authority.

We recognize the financial statement effects of a tax position when it is more-likely-than-not, based on technical merits, that the

position will be sustained upon examination. The determination of whether the tax position meets the more-likely-than-not threshold

requires a facts-based judgment using all information available. In certain cases, we have concluded that the more-likely-than-

not threshold is not met, and accordingly, the amount of tax benefit recognized in our consolidated financial statements is different

than the amount taken or expected to be taken in our tax returns. As of December 31, 2013, the amount of unrecognized tax

benefits for financial reporting purposes, but taken or expected to be taken on tax returns, was £7.7 million of which nil would

have a favorable impact on our effective income tax rate if ultimately recognized, after considering amounts that we would expect

to be offset by valuation allowances.

We are required to continually assess our tax positions, and the results of tax examinations or changes in judgment can result

in substantial changes to our unrecognized tax benefits.

We have taxable outside basis differences on certain investments in non-U.S. subsidiaries. We do not recognize the deferred

tax liabilities associated with these outside basis differences when the difference is considered essentially permanent in duration.

In order to be considered essentially permanent in duration, sufficient evidence must indicate that the foreign subsidiary has invested

or will invest its undistributed earnings indefinitely, or that earnings will be remitted in a tax-free liquidation. If circumstances

change and it becomes apparent that some or all of the undistributed earnings will be remitted on a taxable basis in the foreseeable

future, a net deferred tax liability must be recorded for some or all of the outside basis difference. The assessment of whether

these outside basis differences are considered permanent in nature requires significant judgment and is based on management

intentions to reinvest the earnings of a foreign subsidiary indefinitely in light of anticipated liquidity requirements and other relevant

factors. At December 31, 2013, income and withholding taxes for which a net deferred tax liability might otherwise be required

have not been provided on an estimated £4.3 billion of cumulative temporary differences on non-U.S. entities. If our plans or