Virgin Media 2013 Annual Report Download - page 122

Download and view the complete annual report

Please find page 122 of the 2013 Virgin Media annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

-

134

-

135

-

136

-

137

-

138

-

139

|

|

III - 12

______________

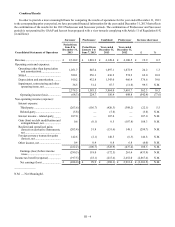

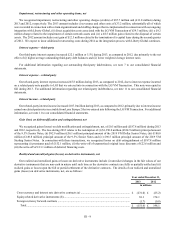

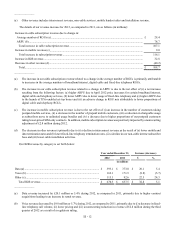

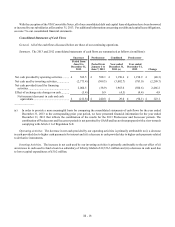

(a) Other revenue includes interconnect revenue, non-cable services, mobile handset sales and installation revenue.

The details of our revenue increase for 2012, as compared to 2011, are as follows (in millions):

Increase in cable subscription revenue due to change in:

Average number of RGUs (a)................................................................................................................................. £ 28.4

ARPU (b)................................................................................................................................................................ 78.7

Total increase in cable subscription revenue....................................................................................................... 107.1

Increase in mobile revenue (c).................................................................................................................................. 9.0

Total increase in subscription revenue................................................................................................................ 116.1

Increase in B2B revenue........................................................................................................................................... 32.8

Decrease in other revenue (d)................................................................................................................................... (40.2)

Total..................................................................................................................................................................... £ 108.7

______________

(a) The increase in our cable subscription revenue related to a change in the average number of RGUs is primarily attributable

to increases in the average numbers of broadband internet, digital cable and fixed-line telephony RGUs.

(b) The increase in our cable subscription revenue related to a change in ARPU is due to the net effect of (i) a net increase

resulting from the following factors: (a) higher ARPU due to April 2012 price increases for certain broadband internet,

digital cable and telephony services, (b) lower ARPU due to lower usage of fixed-line telephony and (c) higher ARPU due

to the launch of TiVo-enabled set-top boxes and (ii) an adverse change in RGU mix attributable to lower proportions of

digital cable and telephony RGUs.

(c) The increase in mobile subscription revenue is due to the net effect of (i) an increase in the number of customers taking

postpaid mobile services, (ii) a decrease in the number of prepaid mobile customers, (iii) a reduction in chargeable usage

as subscribers move to unlimited usage bundles and (iv) a decrease due to higher proportions of our postpaid customers

taking lower-priced SIM-only contracts. In addition, mobile subscription revenue was positively impacted by a nonrecurring

adjustment of £2.8 million during 2012.

(d) The decrease in other revenue is primarily due to (i) a decline in interconnect revenue as the result of (a) lower mobile and

data termination rates and (b) lower fixed-line telephony termination rates, (ii) a decline in our non-cable internet subscriber

base and (iii) lower cable installation activities.

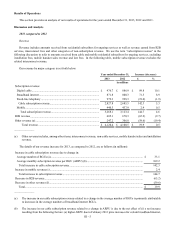

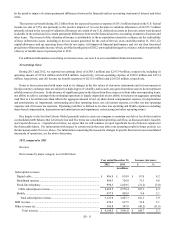

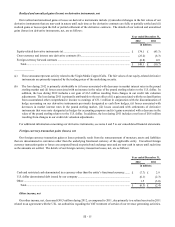

Our B2B revenue by category is set forth below:

Year ended December 31, Increase (decrease)

2012 2011 £%

in millions

Data (a)........................................................................................................ £ 393.1 £ 373.0 £ 20.1 5.4

Voice (b)...................................................................................................... 162.1 171.9 (9.8)(5.7)

Other (c)....................................................................................................... 115.1 92.6 22.5 24.3

Total B2B revenue.................................................................................. £ 670.3 £ 637.5 £ 32.8 5.1

______________

(a) Data revenue increased by £20.1 million or 5.4% during 2012, as compared to 2011, primarily due to higher contract

acquisitions leading to an increase in rental revenue.

(b) Voice revenue decreased by £9.8 million or 5.7% during 2012, as compared to 2011, primarily due to (i) a decrease in fixed-

line telephony call volume, (ii) lower pricing and (iii) a nonrecurring reduction in revenue of £2.8 million during the third

quarter of 2012 as a result of a regulatory ruling.