SunTrust 2003 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2003 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

84 SunTrust Banks, Inc. Annual Report 2003

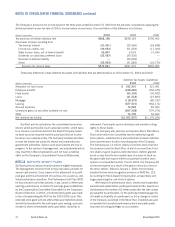

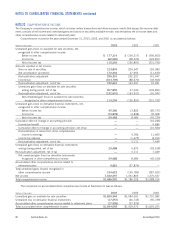

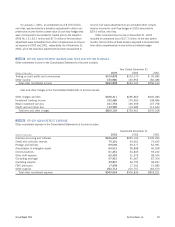

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS continued

As of December 31, 2003 and December 31, 2002, the

maximum potential amount of the Company’s obligation was

$9.7 billion and $9.2 billion, respectively, for financial and per-

formance standby letters of credit. The Company has recorded

$93.8 million in other liabilities for unearned fees related to

these letters of credit as of December 31, 2003. The Company’s

outstanding letters of credit generally have a term of less than

one year. If a letter of credit is drawn upon, the Company may

seek recourse through the customer’s underlying line of credit. If

the customer’s line of credit is also in default, the Company may

take possession of the collateral securing the line of credit.

CONTINGENT CONSIDERATION

The Company has contingent payment obligations related to

certain business combination transactions. Payments are calcu-

lated using certain post-acquisition performance criteria. At

December 31, 2003, the maximum potential liability associated

with these arrangements was approximately $33.4 million.

OTHER

In the normal course of business, the Company enters into

indemnification agreements and provides standard representa-

tions and warranties in connection with numerous transactions.

These transactions include those arising from underwriting

agreements, merger and acquisition agreements, loan sales, and

various other business transactions or arrangements. The extent

of the Company’s obligations under these indemnification agree-

ments depends upon the occurrence of future events; therefore,

the Company’s potential future liability under these arrange-

ments is not determinable.

Third party investors hold Series B Preferred Stock in STB

Real Estate Holdings (Atlanta), Inc. (STBREH), a subsidiary of

SunTrust. The contract between STBREH and the third party

investors contains an automatic exchange clause which, under

certain circumstances, requires the Series B preferred shares to

be automatically exchanged for guaranteed preferred beneficial

interest in debentures of the Company. The guaranteed preferred

beneficial interest in debentures is guaranteed to have a liquida-

tion value equal to the sum of the issue price, $350 million, and

an approximate yield of 8.5% per annum subject to reduction for

any cash or property dividends paid to date. As of December 31,

2003 and December 31, 2002, $412.5 and $377.5 million is

accrued in other liabilities for the principal and interest, respec-

tively. This exchange agreement remains in effect as long as any

shares of Series B Preferred Stock are owned by the third party

investors, not to exceed 30 years.

SunTrust Securities, Inc. (STS) and SunTrust Capital Markets,

Inc. (STCM), broker-dealer affiliates of SunTrust, use a common

third party clearing broker to clear and execute their customers’

securities transactions and to hold customer accounts. Under their

respective agreements, STS and STCM agree to indemnify the

clearing broker for losses that result from a customer’s failure to

fulfill its contractual obligations. As the clearing broker’s rights to

charge STS and STCM have no maximum amount, the Company

believes that the maximum potential obligation cannot be esti-

mated. However, to mitigate exposure, the affiliate may seek

recourse from the customer through cash or securities held in the

defaulting customer’s account. For the years ended December 31,

2003 and 2002, STS and STCM experienced minimal net losses

as a result of the indemnity. The clearing agreements expire in

2004 for STS and 2005 for STCM.

SunTrust Bank has guarantees associated with credit default

swaps, an agreement in which the buyer of protection pays a pre-

mium to the seller of the credit default swap for protection against

an event of default. Events constituting default under such agree-

ments that would result in the Company making a guaranteed

payment to a counterparty may include (i) default of the referenced

asset; (ii) bankruptcy of the customer; or (iii) restructuring or reor-

ganization by the customer. The notional amount outstanding at

December 31, 2003 and December 31, 2002 is $195.0 million

and $175.0 million, respectively. As of December 31, 2003, the

notional amounts expire as follows: $45.0 million in 2004,

$15.0 million in 2005, $0.0 in 2006, $20.0 million in 2007,

$90.0 million in 2008, and $25.0 million in 2009. In the event

of default under the contract, the Company would make a cash

payment to the holder of credit protection and would take delivery

of the referenced asset from which the Company may recover a

portion of the credit loss.

NOTE 19

CONCENTRATIONS OF CREDIT RISK

Credit risk represents the maximum accounting loss that would be

recognized at the reporting date if borrowers failed to perform as

contracted and any collateral or security proved to be of no value.

Concentrations of credit risk (whether on- or off-balance sheet)

arising from financial instruments can exist in relation to individual

borrowers or groups of borrowers, certain types of collateral, certain

types of industries or certain regions of the country. Credit risk asso-

ciated with these concentrations could arise when a significant

amount of loans, related by similar characteristics, are simultane-

ously impacted by changes in economic or other conditions that

cause their probability of repayment to be adversely affected. The

Company does not have a significant concentration to any individ-

ual client except for the U.S. government and its agencies. The

major concentrations of credit risk for the Company arise by collat-

eral type in relation to loans and credit commitments. The only

significant concentration in loans by collateral type that exists is in

loans secured by residential real estate. At December 31, 2003,

the Company had $24.2 billion in residential real estate loans,

representing 29.9% of total loans, and an additional $7.8 billion

in commitments to extend credit on such loans. A geographic

concentration arises because the Company operates primarily in

the Southeastern and Mid-Atlantic regions of the United States.

SunTrust engages in limited international banking activities.

The Company’s total cross-border outstandings were $513.6 mil-

lion as of December 31, 2003.