SunTrust 2003 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2003 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

Annual Report 2003 SunTrust Banks, Inc. 81

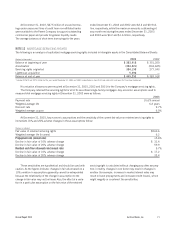

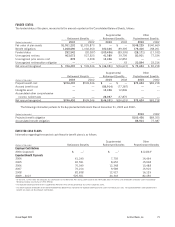

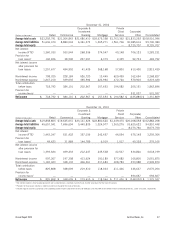

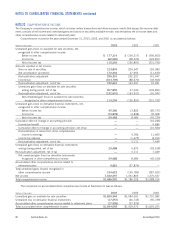

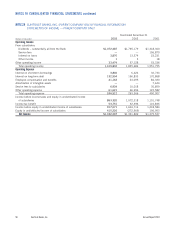

DERIVATIVES

The Company enters into various derivative contracts both in a

dealer capacity, to facilitate customer transactions, and also as a

risk management tool. Where contracts have been created for

customers, the Company enters into transactions with dealers to

offset its risk exposure. Derivatives are also used as a risk man-

agement tool to hedge the Company’s exposure to changes in

interest rates or other defined market risks.

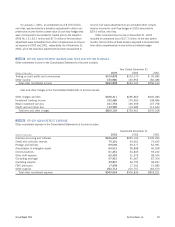

Interest rate swaps are contracts in which a series of inter-

est rate cash flows, based on a specific notional amount and a

fixed and floating interest rate, are exchanged over a prescribed

period. Caps and floors are contracts that transfer, modify or

reduce interest rate risk in exchange for the payment of a pre-

mium when the contract is issued. The true measure of credit

exposure is the replacement cost of contracts that have become

favorable to the Company.

Futures and forwards are contracts for the delayed delivery

of securities or money market instruments in which the seller

agrees to deliver on a specified future date, a specified instru-

ment, at a specified price or yield. The credit risk inherent in

futures is the risk that the exchange party may default. Futures

contracts settle in cash daily; therefore, there is minimal credit

risk to the Company. The credit risk inherent in forwards arises

from the potential inability of counterparties to meet the terms of

their contracts. Both futures and forwards are also subject to the

risk of movements in interest rates or the value of the underlying

securities or instruments.

Derivative instruments expose the Company to credit and

market risk. If the counterparty fails to perform, the credit risk is

equal to the fair value gain of the derivative. When the fair value

of a derivative contract is positive, this indicates the counterparty

owes the Company, and therefore, creates a repayment risk for the

Company. When the fair value of a derivative contract is negative,

the Company owes the counterparty and has no repayment risk.

The Company minimizes the credit or repayment risk in derivative

instruments by entering into transactions with high quality coun-

terparties that are reviewed periodically by the Company’s credit

committee. The Company also maintains a policy of requiring that

all derivative contracts be governed by an International Swaps and

Derivatives Associations Master Agreement; depending on the

nature of the derivative transactions, bilateral collateral agree-

ments may be required as well. When the Company has more

than one outstanding derivative transaction with a single counter-

party, and there exists a legally enforceable master netting

agreement with the counterparty, the mark to market exposure is

the net of the positive and negative exposures with the same coun-

terparty. When there is a net negative exposure, the Company

considers its exposure to the counterparty to be zero. The net mark

to market position with a particular counterparty represents a rea-

sonable measure of credit risk when there is a legally enforceable

master netting agreement, including a legal right of setoff of receiv-

able and payable derivative contracts between the Company and

a counterparty.

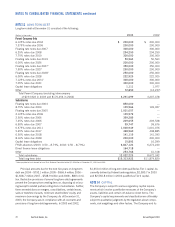

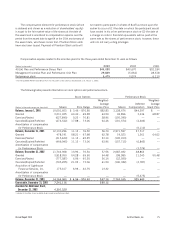

At December 31, 2003 At December 31, 2002

Contract or Contract or

Notional Amount Notional Amount

For Credit Risk For Credit Risk

(Dollars in millions) End User Customers1Amount End User Customers1Amount

Derivatives Contracts

Interest rate contracts

Swaps $9,524 $39,468 $ 395 $4,919 $32,344 $ 266

Futures and forwards 4,836 3,861 — 8,746 6,708 —

Caps/Floors 30 8,176 — —6,254 —

Total interest rate contracts 14,390 51,505 395 13,665 45,306 266

Foreign exchange rate contracts —6,129 82 —3,803 50

Interest rate lock commitments 2,795 — — 5,489 — —

Commodity and other contracts 440 29 68 236 2 59

Total derivatives contracts $17,625 $57,663 $ 545 $19,390 $49,111 $ 375

Credit-related Arrangements

Commitments to extend credit $56,584 $56,584 $49,557 $49,557

Standby letters of credit and

similar arrangements 9,843 9,843 9,362 9,362

Total credit-related arrangements $66,427 $66,427 $58,919 $58,919

Total Credit Risk Amount $66,972 $59,294

1Includes both long and short derivative contracts.