SunTrust 2003 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2003 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

80 SunTrust Banks, Inc. Annual Report 2003

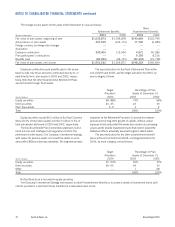

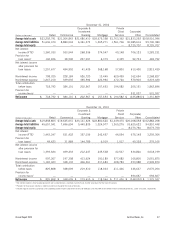

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS continued

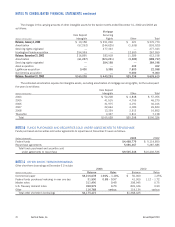

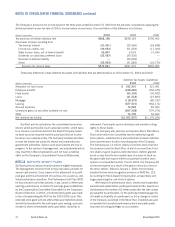

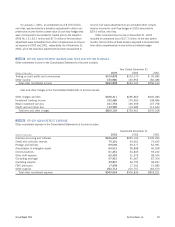

NET PERIODIC BENEFIT COST

Components of net periodic benefit cost (income) were as follows:

Supplemental Other

Retirement Benefits Retirement Benefits Postretirement Benefits

(Dollars in thousands) 2003 2002 2001 2003 2002 2001 2003 2002 2001

Service cost $43,071 $42,530 $ 39,506 $1,520 $823 $ 773 $2,515 $4,146 $ 3,905

Interest cost 74,574 69,067 62,976 4,991 4,995 4,678 10,823 11,052 11,643

Expected return on

plan assets (111,656) (112,670) (103,451) ———(8,489) (8,218) (9,124)

Amortization of prior

service cost (443) (443) (1,422) 1,941 2,201 2,446 ———

Recognized net

actuarial loss 57,307 16,657 — 4,358 3,180 2,581 6,840 3,372 2,443

Amortization of initial

transition obligation ——(510) 44 44 275 2,322 3,809 3,809

Net periodic benefit

cost (income) $62,853 $15,141 $ (2,901) $12,854 $11,243 $10,753 $14,011 $14,161 $12,676

Weighted-average

assumptions used to

determine net cost

Discount rate 6.75% 7.25% 7.50% 6.75% 7.25% 7.50% 6.75% 7.25% 7.50%

Expected return on

plan assets 8.75 9.50 9.50 ———6.25 7.00 7.00

Rate of compensation

increase 3.50 4.00 4.00 3.50 4.00 4.00 ———

Based on the investment policy of the plans, as well as the

plan’s asset allocation and future return expectation, an 8.75%

rate of return was used to calculate the periodic benefit cost for

2003. During 2003, a detailed asset study was performed

which included a statistical forecast of the plan’s expected rate

of return for the approximate duration of SunTrust’s benefit obli-

gations using capital markets data and historical analysis. Based

on this study, SunTrust anticipates lowering the return on asset

assumption to 8.50% for 2004.

In addition, SunTrust sets pension asset values equal to

their market value, in contrast to the use of a smoothed asset

value that incorporates gains and losses over a period of years.

The poor economic environment over the three years prior to

2003 may have led to inflated asset values in cases where a

smoothed asset value is used. Assumed discount rates and

expected returns on plan assets impact the net periodic benefit

cost. A 25 basis point adverse change to the discount rate or

other expected long-term return on plan assets would increase

the net periodic benefit cost approximately $9.0 million and

$3.8 million, respectively.

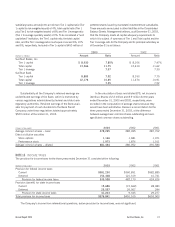

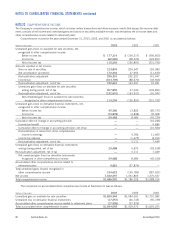

NOTE 17

DERIVATIVES AND OFF-BALANCE SHEET

ARRANGEMENTS

In the normal course of business, the Company utilizes various

financial instruments to meet the needs of customers and to man-

age the Company’s exposure to interest rate and other market

risks. These financial instruments, which consist of derivatives

contracts and credit-related arrangements, involve, to varying

degrees, elements of credit and market risk in excess of the

amount recorded on the balance sheet in accordance with gener-

ally accepted accounting principles.

Credit risk represents the potential loss that may occur

because a party to a transaction fails to perform according to the

terms of the contract. Market risk is the possibility that a change

in market prices may cause the value of a financial instrument to

decrease or become more costly to settle. The contract/notional

amounts of financial instruments, which are not included in the

Consolidated Balance Sheets, do not necessarily represent credit

or market risk. However, they can be used to measure the extent

of involvement in various types of financial instruments.

The Company manages the credit risk of its derivatives and

unfunded commitments by limiting the total amount of arrange-

ments outstanding by individual counterparty; by monitoring the

size and maturity structure of the portfolio; by obtaining collateral

based on management’s credit assessment of the counterparty;

and by applying uniform credit standards maintained for all

activities with credit risk. Collateral held varies but may include

marketable securities, accounts receivable, inventory, property,

plant and equipment, and income-producing commercial prop-

erties. Collateral may cover the entire expected exposure for

transactions or may be called for when credit exposure exceeds

defined thresholds or credit risk. In addition, the Company enters

into master netting agreements which incorporate the right of set-

off to provide for the net settlement of covered contracts with the

same counterparty in the event of default or other termination of

the agreement.