SunTrust 2003 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2003 SunTrust annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

|

|

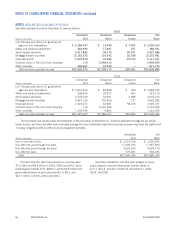

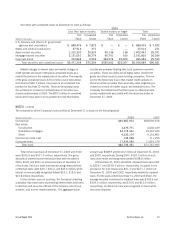

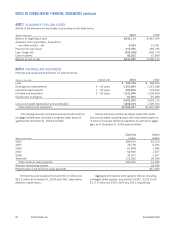

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

60 SunTrust Banks, Inc. Annual Report 2003

NOTE 1

ACCOUNTING POLICIES

GENERAL

The consolidated financial statements include the accounts of

the Company and its subsidiaries. All significant intercompany

accounts and transactions have been eliminated. Results of

operations of companies purchased are included from the dates

of acquisition. Assets and liabilities of purchased companies are

stated at estimated fair values at the date of acquisition.

The preparation of financial statements in conformity with

accounting principles generally accepted in the United States

requires management to make estimates and assumptions that

affect the reported amounts of assets and liabilities, the disclo-

sure of contingent assets and liabilities at the date of the financial

statements and the reported amounts of revenues and expenses

during the reporting period. Actual results could vary from these

estimates; however, in the opinion of management, such vari-

ances would not be material. Certain reclassifications have been

made to prior year amounts to conform to the 2003 presentation.

SECURITIES

Securities in the investment portfolio are classified as securities

available for sale and are carried at market value with unrealized

gains and losses, net of any tax effect, included in accumulated

other comprehensive income as a component of shareholders’

equity. Realized gains and losses on the securities portfolio are

determined using the specific identification method and recog-

nized currently in the Consolidated Statements of Income.

Trading account securities are carried at market value with

the gains and losses, determined using the specific identification

method and recognized currently in the Consolidated Statements

of Income. Included in noninterest income are realized and unreal-

ized gains and losses resulting from such market value adjustments

of trading account securities and from recording the results of sales.

LOANS HELD FOR SALE

Loans held for sale that are not documented as the hedged item

in a fair value hedge are carried at the lower of aggregate cost or

market value. Adjustments to reflect market value and realized

gains and losses upon ultimate sale of the loans are classified as

other noninterest income.

Loans held for sale that are documented as the hedged item

in a fair value hedge are carried at fair value. Fair value is based

on the contract prices at which the loan will be sold, or if the

loan is not committed for sale, the current market price.

The Company classifies certain residential mortgage loans

and student loans as loans held for sale. Upon transfer to loans

held for sale, any losses are recorded through the allowance for

loan losses with subsequent losses recorded as a component of

noninterest expense.

LOANS

Interest income on all types of loans is accrued based upon the

outstanding principal amounts, except those classified as nonac-

crual loans. Interest accrual is discontinued when it appears that

future collection of principal or interest according to the contrac-

tual terms may be doubtful. Interest income on nonaccrual loans

is recognized on a cash basis if there is no longer doubt of future

collection of principal. Loans classified as nonaccrual, except for

smaller balance homogenous loans, which include consumer and

residential loans, meet the criteria to be considered impaired

loans. The Company classifies a loan as nonaccrual with the

occurrence of one of the following events: (i) interest or principal

has been in default 90 days or more, unless the loan is well-

secured and in the process of collection; (ii) collection of recorded

interest or principal is not anticipated; or (iii) income for the loan

is recognized on a cash basis due to the deterioration in the finan-

cial condition of the debtor. Consumer and residential mortgage

loans are typically placed on nonaccrual when payments have

been in default for 90 and 125 days or more, respectively. (See

Allowance for Loan Losses section of this Note for further discus-

sion of impaired loans.)

Fees and incremental direct costs associated with the loan

origination and pricing process are deferred and amortized as

level yield adjustments over the respective loan terms. Fees

received for providing loan commitments and letter of credit

facilities that result in loans are deferred and then recognized

over the term of the loan as an adjustment of the yield. Fees on

commitments and letters of credit that are not expected to be

funded are amortized into noninterest income using the straight-

line method over the commitment period.

ALLOWANCE FOR LOAN LOSSES

The Company’s allowance for loan losses is that amount consid-

ered adequate to absorb losses in the portfolio based on

management’s evaluations of the size and current risk character-

istics of the loan portfolio. Such evaluations consider the level of

problem loans, prior loan loss experience, as well as the impact

of current economic conditions, portfolio concentrations and

other risk factors. Specific allowances for loan losses are estab-

lished for individual impaired loans as required per SFAS Nos.

114 and 118. The specific allowance established for these loans

is based on a thorough analysis of the most probable source of

repayment, including the present value of the loan’s expected

future cash flow, the loan’s estimated market value or the esti-

mated fair value of the underlying collateral. General allowances

are established for loans that can be grouped into pools based on

similar characteristics as outlined in SFAS No. 5. In this process,

general allowance factors are based on the results of a statistical

loss migration analysis and other analyses of recent and historical

charge-off experience and are typically applied to the portfolio in

terms of loan type and internal credit risk ratings. Economic