Rogers 2014 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2014 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

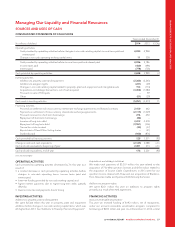

MANAGEMENT’S DISCUSSION AND ANALYSIS

Credit ratings are not recommendations for investors to purchase, hold

or sell the rated securities, nor are they a comment on market price or

investor suitability. There is no assurance that a rating will remain in

effect for a given period of time, or that a rating will not be revised or

withdrawn entirely by a rating agency if it believes circumstances

warrant it. The ratings on our senior debt provided by Standard &

Poor’s, Fitch and Moody’s are investment grade ratings.

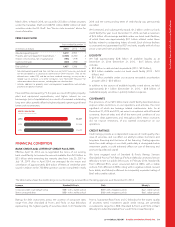

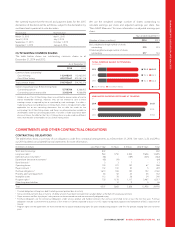

PENSION OBLIGATIONS

Our retiree pension plans had a funding deficit of approximately $307

million (2013 – $172 million). During 2014, our funding deficit

increased by $135 million primarily as a result of a decrease in the

discount rate we used to measure these obligations.

We made a total of $106 million (2013 – $101 million) of contributions

to our pension plans. We expect our total estimated funding

requirements to be $117 million in 2015 and to be adjusted annually

thereafter, based on various market factors such as interest rates and

expected returns and staffing assumptions.

Changes in factors such as the discount rate, participation rates,

increase in compensation and the expected return on plan assets can

affect the accrued benefit obligation, pension expense and the

deficiency of plan assets over accrued obligations in the future. See

Critical accounting estimates for more information.

Purchase of annuities

From time to time we have made additional lump-sum contributions to

our pension plans, and the pension plans have purchased annuities

from insurance companies to fund the pension benefit obligations for

certain groups of retired employees in the plans. Purchasing the

annuities relieves us of our primary responsibility for that portion of the

accrued benefit obligations for the retiredemployeesandeliminates

the significant risk associated with the obligations.

We did not make any additional lump-sum contributions to our

pension plans in 2014 or 2013, and the pension plans did not

purchase additional annuities.

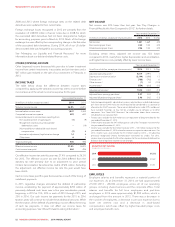

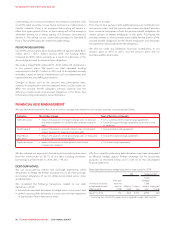

FINANCIAL RISK MANAGEMENT

We use derivative instruments from time to time to manage risks related to our business activities, summarized as follows:

Derivative The risk they manage Types of derivative instruments

Debt derivatives • Impact of fluctuations in foreign exchange rates on principal

and interest payments for US dollar-denominated long-term

debt

• Cross-currency interest rate exchange agreements

• Forward foreign exchange agreements (from time to time

as necessary)

Bond forwards • Impact of fluctuations in market interest rates on forecasted

interest payments for expected long-term debt

• Forward interest rate agreements

Expenditure

derivatives

• Impact of fluctuations in foreign exchange rates on forecasted

US dollar-denominated expenditures

• Forward foreign exchange agreements

Equity derivatives • Impact of fluctuations in share price on stock-based

compensation expense

• Total return swap agreements

We also manage our exposure to fluctuating interest rates and we have

fixed the interest rate on 92.7% of our debt including short-term

borrowings as at December 31, 2014 (2013 – 95.3%).

DEBT DERIVATIVES

We use cross-currency interest rate exchange agreements (debt

derivatives), to hedge the foreign exchange risk on all of the principal

and interest obligations of our US dollar-denominated senior notes

and debentures.

We completed the following transactions related to our debt

derivatives in 2014:

• entered into new debt derivatives to hedge senior notes issued; and

• settled maturing debt derivatives in conjunction with the repayment

or repurchase of the related senior notes.

All of our currently outstanding debt derivatives have been designated

as effective hedges against foreign exchange risk for accounting

purposes as described below and in note 16 to the consolidated

financial statements.

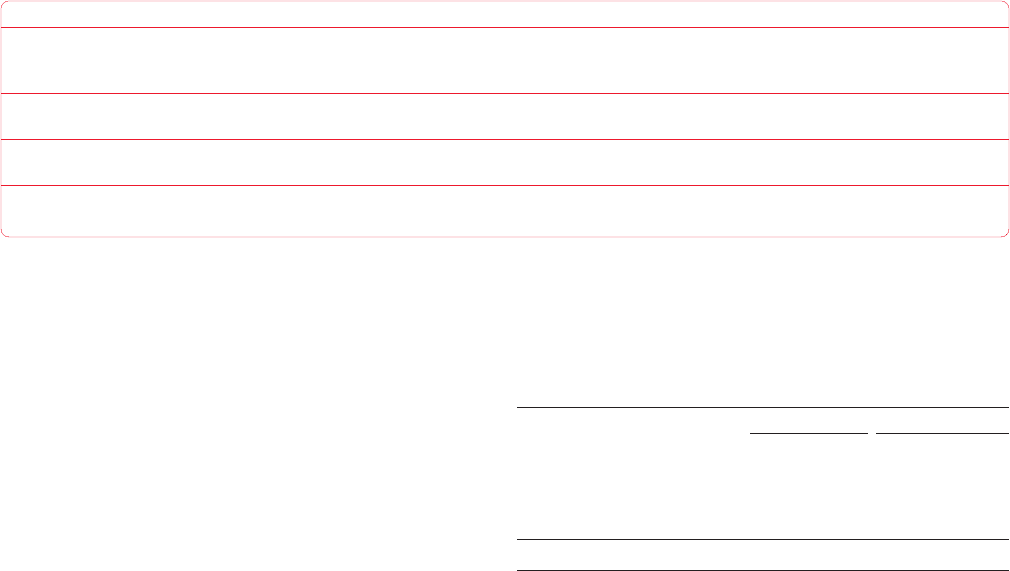

New debt derivatives to hedge new senior notes issued in 2014

(In millions of dollars,

except interest rates)

Effective date

US$ Hedging effect

Principal/

Notional

amount

(US$)

Maturity

date

Coupon

rate

Fixed

hedged

Cdn$

interest

rate 1

Equivalent

(Cdn$)

March 10, 2014 750 2044 5.00% 4.99% 832

1Converting from a fixed US$ coupon rate to a weighted average Cdn$ fixed rate.

60 ROGERS COMMUNICATIONS INC. 2014 ANNUAL REPORT