Rogers 2014 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2014 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

debt securities. The remaining $8 million, net of income taxes of

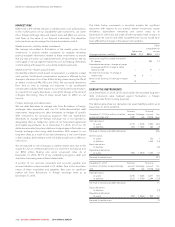

$1 million, will remain in the hedging reserve until such time as the

related debt is settled.

Repayment of senior notes and related derivative settlements

During 2014, we repaid or repurchased our US$750 million

($834 million) and US$350 million ($387 million) senior notes due

2014, totalling $1,221 million (see note 30). In addition, the debt

derivatives related to these senior notes matured in March 2014.

Upon the repayment or repurchase of these senior notes, a $29 million

loss, which was deferred in the hedging reserve in the prior years, was

recognizedinnetincome(seenote10).Thislossrelatestotransactions

in 2008 and 2013 where contractual foreign exchange rates on the

related debt derivatives were renegotiated to then current rates.

As at December 31, 2014 we have US$6.0 billion (2013 –

US$6.4 billion) of US dollar-denominated senior notes and

debentures, all of which have been hedged using debt derivatives

(2013 – 100 %).

In June 2013, when we repaid or repurchased our US$350 million

($356 million) senior notes due 2013, the associated debt derivatives

were settled at maturity, resulting in total payments of approximately

$104 million. The settlements of these debt derivatives did not impact

net income for the year ended December 31, 2014.

Bond forwards

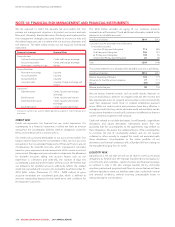

We use bond forward derivatives (bond forwards) to hedge interest

rate risk on the senior notes we expect to issue in the future. We use

bond forwards for risk-management purposes only.

During 2014, we entered into bond forwards to hedge the underlying

Government of Canada (GoC) interest rate risk that will comprise a

portion of the interest rate risk associated with our anticipated future

debt issuances. As a result of these bond forwards, we have hedged

the underlying GoC 10-year rate on $1.5 billion notional amount for

anticipated future debt issuances from 2015 to 2018 and the

underlying GoC 30-year rate on $0.4 billion notional amount for

December 31, 2018. The bond forwards are effective from December

2014. There was no bond forward activity or balances in 2013.

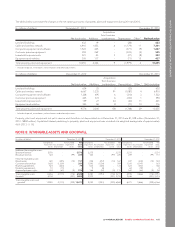

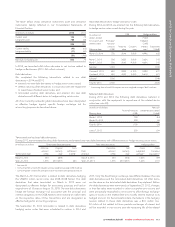

(In millions of dollars, except interest rates)

GoC term (years) Maturity date 1

Initial GoC

Interest rate 1Notional amount

10 Dec 31, 2015 2.05% 500

10 Dec 31, 2016 2.04% 500

10 Apr 30, 2018 2.07% 500

30 Dec 31, 2018 2.41% 400

Total 1,900

1Bond forwards with maturity dates beyond December 31, 2015 are subject to GoC

rate re-setting from time to time.

Expenditure derivatives

We use foreign currency forward contracts (expenditure derivatives) to

hedge the foreign exchange risk on the notional amount of certain

forecasted expenditures. We use expenditure derivatives for risk-

management purposes only.

We entered into expenditure derivatives to manage foreign exchange

risk on certain forecasted expenditures as follows:

(In millions of dollars, except exchange rates)

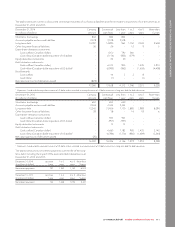

Notional

Trade date Maturity dates

Notional

amount

(US$)

Exchange

Rate

Converted

amount

(Cdn$)

February 2014 January 2015 to

April 2015 200 1.1100 222

May 2014 May 2015 to

December 2015 232 1.0948 254

June 2014 January 2015 to

December 2015 288 1.0903 314

July 2014 January 2016 to

December 2016 240 1.0833 260

Total as at December 31, 2014 960 1.0940 1,050

July 2011 January 2014 to

July 2014 140 0.9643 135

September 2013 January 2014 to

December 2014 760 1.0368 788

Total as at December 31, 2013 900 1.0256 923

The expenditure derivatives noted above have been designated as

hedges for accounting purposes. In the year ended December 31,

2014, we settled US$900 million (2013 — US$435 million) of

expenditure derivatives for $923 million (2013 — $430 million). All of

our currently outstanding expenditure derivatives have been

designated as effective hedges against foreign exchange risk for

accounting purposes.

Equity derivatives

We use stock-based compensation derivatives (equity derivatives) to

hedge the market price appreciation risk of the RCI Class B shares

granted under our stock-based compensation programs. We use

equity derivatives for risk-management purposes only.

In 2013, we entered into equity derivatives to hedge market price

appreciation risk associated of 5.7 million RCI Class B Non-Voting

shares that have been granted under our stock-based compensation

programs for stock options, restricted share units (RSUs) and deferred

share units (DSUs) (see note 25). The equity derivatives were entered

into at a weighted average price of $50.37 with original terms to

maturity of one year, extendible for further one year periods with the

consent of the hedge counterparties. In 2014, we executed extension

agreements for each of our equity derivative contracts under

substantially the same committed terms and conditions with revised

expiry dates to April 2015 (from April 2014). The equity derivatives

have not been designated as hedges for accounting purposes.

During 2014, we recognized an expense, net of interest receipts of

$10 million (2013 — $8 million), in stock-based compensation expense

related to the change in fair value of our equity derivative contracts net

of received payments. As of December 31, 2014, the fair value of the

equity derivatives was a liability of $30 million (December 31, 2013 —

$13 million), which is included in the current portion of derivative

instruments liabilities.

114 ROGERS COMMUNICATIONS INC. 2014 ANNUAL REPORT