Rogers 2014 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2014 Rogers annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

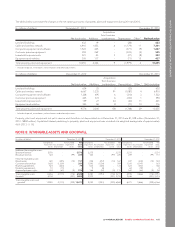

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

Finite useful lives

We amortize intangible assets with finite useful lives into depreciation

and amortization in the Consolidated Statements of Income on a

straight-line basis over their estimated useful lives as noted in the table

below. We review their useful lives, residual values and the

amortization methods at least once a year.

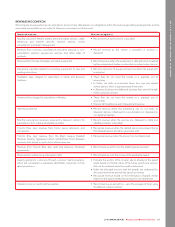

Intangible asset Estimated useful life

Brand names 7 to 20 years

Customer relationships 3 to 10 years

Roaming agreements 12 years

Marketing agreements 3 years

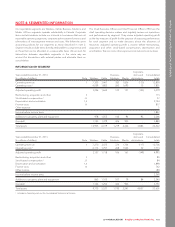

See note 8 for more information about our intangible assets.

Acquired program rights

Program rights are contractual rights we acquire from third parties to

broadcast television and sports programs. We record them at cost less

accumulated amortization and accumulated impairment losses. We

capitalize program rights on the Consolidated Statements of Financial

Position when the licence period begins and the program is available

for use, and amortize them to other external purchases in operating

costs in the Consolidated Statements of Income over the expected

exhibition period. If programs are not scheduled, we consider the

related program rights to be impaired and write them off. Otherwise,

we test them for impairment as intangible assets with finite useful lives.

Program rights for multi-year sports programming arrangements are

expensed when the games are aired. The cost for multi-year sports

broadcast rights agreements are amortized to operating expenses

during the applicable seasons based on the pattern in which the rights’

economic benefits are expected to be consumed with reference to our

projections of advertising and subscriber revenues. If the annual

contractual payments related to each season approximate the pattern

of expected future economic benefits consumption, we expense these

contractual payments during the applicable season.

To the extent that prepayments are made at the commencement of a

multi-year contract towards future years’ rights fees, these

prepayments are recorded as intangible assets and amortized to

operating expenses over the contract term. To the extent that

prepayments are made for annual contractual fees within a season,

they are included in other current assets – prepaid expenses in our

Consolidated Statement of Financial Position as the rights will be

consumed within the next twelve months.

GOODWILL

We record goodwill arising from business combinations when the fair

value of the separately identifiable assets we acquired and liabilities we

assumed is lower than the consideration we paid (including the

recognized amount of the non-controlling interest, if any). If the fair

value of the consideration transferred is lower than that of the

separately identified assets and liabilities, we immediately record the

difference as a gain in net income.

See note 8 for more information about our goodwill.

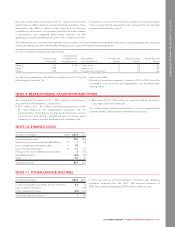

IMPAIRMENT

Financial assets

We consider a financial asset to be impaired if there is objective

evidence that one or more events has had a negative effect on its

estimated future cash flows and the effect can be reliably estimated.

Financial assets that are significant in value are tested for impairment

individually. All other financial assets are assessed collectively based on

thenatureofeachasset.

We measure impairment for financial assets as follows:

•loans and receivables –wemeasuretheexcessofthecarrying

amountoftheassetoverthepresentvalueoffuturecashflowswe

expect to derive from it, if any. The difference is allocated to an

allowance for doubtful accounts, and recognized as a loss in net

income.

•available-for-sale financial assets –wemeasuretheexcessofthecost

to acquire the asset (less any impairment loss we have previously

recognized), over its current fair value, if any. The difference is

reclassified from the available-for-sale reserve in equity to net

income.

Investments in associates and joint arrangements

At the end of each reporting period, we assess whether there is

objective evidence that impairment exists in our investments in

associates and joint arrangements. If objective evidence exists, we

compare the carrying amount of the investment to its recoverable

amount and recognize the excess over the recoverable amount, if any,

as a loss in net income (see Recognition of Impairment Charge,below).

Indefinite-life intangible assets and goodwill

We test indefinite-life intangible assets and goodwill for impairment

once a year, or more frequently if we identify indicators of impairment.

Goodwill is allocated to cash generating units (or groups of cash

generating units) based on the level at which management monitors

goodwill, which cannot be higher than an operating segment. The

allocation involves considerable management judgement, and is made

to cash generating units (or groups of cash generating units) that are

expected to benefit from the synergies of the business combination

from which the goodwill arose.

A cash generating unit is the smallest identifiable group of assets that

generates cash inflows largely independent of the cash inflows from

other assets or groups of assets.

Non-financial assets with finite useful lives

Our non-financial assets with finite useful lives include property, plant

and equipment, and intangible assets. We test these assets for

impairment whenever an event or change in circumstances indicates

that their carrying amounts may not be recoverable. The asset is

impaired if the recoverable amount is less than the carrying amount. If

we cannot estimate the recoverable amount of an individual asset

because it does not generate independent cash inflows, we test the

entire cash generating unit for impairment.

Recognition of impairment charge

The recoverable amount of a cash generating unit or asset is the higher

of its:

• fair value less costs to sell; and

• value in use.

We estimate an asset’s or cash generating unit’s fair value less costs to

sell using the best information available to estimate the amount we

could obtain from disposing the asset in an arm’s length transaction,

less the estimated cost of disposal.

We estimate value in use by discounting estimated future cash flows

from a cash generating unit or asset to their present value using a

2014 ANNUAL REPORT ROGERS COMMUNICATIONS INC. 97