Pizza Hut 2011 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2011 Pizza Hut annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

|

|

16MAR201218540977

time by the Committee for competitiveness. When last reviewed by the Committee, its independent

consultant indicated that these benefits generally fall below the average for companies of our size and,

therefore, fall within (and arguably under) the competitive norm. As noted above, the Committee believes

the benefits provided in case of a change in control are appropriate and are consistent with the policy of

attracting and retaining highly qualified employees.

In analyzing the reasonableness of these change in control benefits, the Committee chose not to

consider wealth accumulation of the NEOs (although this information was provided to the Committee) in

determining whether these benefits should be provided. This is because, if properly designed, the

Committee believes a change in control program protects shareholder interests by enhancing employee

focus during rumored or actual change in control activity through:

• incentives to remain with the Company despite uncertainties while a transaction is under

consideration or pending

• assurance of severance and benefits for terminated employees

• access to equity components of total compensation after a change in control.

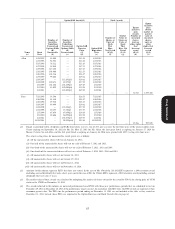

Future Severance Agreement Policy

As recommended by shareholders in 2007, the Committee approved a new policy in 2007 to limit

future severance agreements with NEOs or our other executives. The Committee adopted a policy under

which the Company will seek shareholder approval for future severance payments to an NEO if such

payments would exceed 2.99 times the sum of (a) the NEO’s annual base salary as in effect immediately

prior to termination of employment; and (b) the highest annual bonus awarded to the NEO by the

Company in any of the Company’s three full fiscal years immediately preceding the fiscal year in which

termination of employment occurs or, if higher, the executive’s target bonus. Certain types of payments are

excluded from this policy, such as amounts payable under arrangements that apply to classes of employees

other than the NEOs or that predate the implementation of the policy, as well as any payment that the

Committee determines is a reasonable settlement of a claim that could be made by the NEO.

Proxy Statement

Compensation Recovery Policy

The Committee has adopted a Compensation Recovery Policy for stock awards and annual bonuses

awarded after 2008. Pursuant to this policy, executive officers (including the NEOs) may be required to

return compensation paid based on financial results that were later restated. This policy applies only if the

executive officers engaged in knowing misconduct that contributed to the need for a material restatement,

or contributed to the use of inaccurate metrics in the calculation of incentive compensation. Under this

policy, when the Board determines in its sole discretion that recovery of compensation is appropriate, the

Company could require repayment of all or a portion of any bonus, incentive payment, equity-based award

or other compensation, to the fullest extent permitted by law.

Deductibility of Executive Compensation

The provisions of Section 162(m) of the Internal Revenue Code limits the tax deduction for

compensation in excess of one million dollars paid to certain NEOs. However, performance-based

compensation is excluded from the limit so long as it meets certain requirements. The Committee believes

that the annual bonus, stock option, stock appreciation rights, RSU and PSU grants satisfy the

requirements for exemption under Internal Revenue Code Section 162(m). Payments made under these

plans qualify as performance-based compensation.

For 2011, the annual salary paid to Mr. Novak exceeded one million dollars. The Committee sets

Mr. Novak’s salary as described above under the heading ‘‘Compensation of Our Chief Executive Officer.’’

The other NEOs were in each case paid salaries of one million dollars or less, except for Mr. Su’s whose

54