MasterCard 2008 Annual Report Download - page 80

Download and view the complete annual report

Please find page 80 of the 2008 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

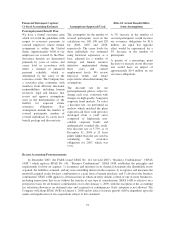

Financial Statement Caption/

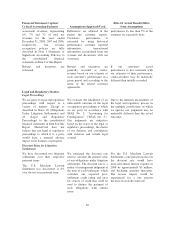

Critical Accounting Estimate Assumptions/Approach Used

Effect if Actual Results Differ

from Assumptions

The American Express Settlement

was discounted at 5.75% over the

three-year payment term.

For the American Express

Settlement, a one percent increase in

the discount rate would have

decreased the litigation settlement

expense for 2008 by approximately

$24 million. A one percent decrease

in the discount rate would produce

the opposite impact.

For the American Express

Settlement, a one percent increase in

the discount rate would have

increased interest expense for 2008

by approximately $7 million. A one

percent decrease in the discount rate

would produce the opposite impact.

Income Taxes

In calculating our effective tax rate,

we need to make decisions

regarding certain tax positions,

including the timing and amount of

deductions and allocation of income

among various tax jurisdictions.

We have various tax filing

positions, including the timing and

amount of deductions,

establishment of reserves for

credits and audit matters and the

allocation of income among

various tax jurisdictions.

Although we believe that our

estimates and judgments discussed

herein are reasonable, actual results

may differ by a material amount.

We record a valuation allowance to

reduce our deferred tax assets to the

amount that is more likely than not

to be realized.

We considered projected future

taxable income and ongoing tax

planning strategies in assessing the

need for the valuation allowance.

If we realize a deferred tax asset

subject to a valuation allowance in

excess of the deferred tax asset net

of that valuation allowance or if we

were unable to realize such a net

deferred tax asset; an adjustment to

the deferred tax asset would

increase or decrease earnings,

respectively, in the period.

We record tax liabilities for

uncertain tax positions taken or to

be taken on tax returns that may not

be sustained or would only partially

be sustained, upon examination by

the relevant taxing authorities.

We considered all relevant facts

and current authorities in the tax

law in assessing whether an

uncertain tax position was more

likely than not to be sustained.

If upon examination, we realize a

tax benefit which is not fully

sustained or is more favorably

sustained this would decrease or

increase earnings, in the period. In

certain situations, the Company will

have offsetting tax deductions or tax

credits.

We do not record U.S. income tax

expense for foreign earnings which

we plan to reinvest to expand our

international operations.

We considered business plans,

planning opportunities, and

expected future outcomes in

assessing the needs for future

expansion and support of our

international operations.

If our business plans change or our

future outcomes differ from our

expectations, additional U.S.

income tax expense would have to

be recorded which would increase

our effective tax rate in that period.

70