MasterCard 2008 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2008 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

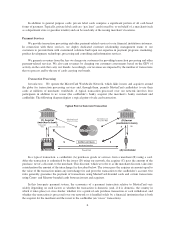

Clearing refers to the exchange of financial transaction information between issuers and acquirers after a

transaction has been completed. MasterCard clears transactions among customers through our central and

regional processing systems. Credit and offline debit transactions using MasterCard-branded cards are generally

cleared via centralized processing through GCMS, and the related information is typically routed among

customers via the MasterCard Worldwide Network. GCMS has helped us to improve our time-to-market in

introducing new programs and services. More importantly, using GCMS, we can partner with our customers to

provide value-added services to merchants and cardholders. For example, issuers can use GCMS to develop

marketing promotions for segments of their card portfolios without investing in their own systems development.

We believe that GCMS and our other recent system enhancements position us well to pursue incremental

processing opportunities. For online debit transactions, the Single Message System (or MDS) performs clearing

between customers and other debit transaction processing networks. Since 2004, MasterCard has worked with

issuers and acquirers to increase the routing priority of our systems for the processing of PIN point-of-sale

transactions, and has begun to establish direct processing connections to major U.S. merchants.

Once transactions have been authorized and cleared, MasterCard provides services in connection with the

settlement of the transactions—that is, the exchange of funds along with associated fees. Settlement for credit,

offline debit and online debit transactions is provided through the MasterCard Worldwide Network. Once

clearing is completed, a daily reconciliation is provided to each customer involved in settlement, detailing the net

amounts by clearing cycle and a final settlement position. The actual exchange of funds takes place between a

clearing bank chosen by the customer and approved by MasterCard, and a settlement bank chosen by

MasterCard. Customer settlement occurs in U.S. dollars or in a limited number of other currencies in accordance

with our established rules.

MasterCard Integrated Processing Solutions (IPS). In April 2008, we introduced MasterCard Integrated

Processing Solutions (“IPS”), a MasterCard-engineered debit processing platform. IPS is designed to provide an

issuing financial institution with a complete processing solution to help create differentiated products and

services and allow quick deployment of payments portfolios across banking channels. Through a single

connection, the IPS platform is designed to provide customers with an integrated suite of branded debit network

and card issuer processing services in support of PIN-based and signature debit payments, prepaid payment cards

and ATM driving as well as real-time card management and back-office processing services. The proprietary

MasterCard Portfolio Viewer feature of IPS, a user-friendly customer interface, can deliver aggregate cardholder

intelligence across accounts and product lines, providing issuers a view of information that can help them

customize their products and programs. In 2008, we announced our first customer to implement IPS for complete

branded debit network and issuer processing. We also announced in 2008 the first financial institution to take

advantage of the global prepaid transaction processing capabilities of IPS. We continue to develop opportunities

to further enhance our IPS offerings.

Regional Transaction Processing. We provide transaction processing (authorization, clearing and

settlement) services for customers in our Europe region through our subsidiary, MasterCard Europe sprl

(“MasterCard Europe”). These services allow European customers to facilitate payment transactions between

cardholders and merchants throughout Europe. Recently, we substantially completed a multi-year technical

convergence project to integrate our European systems into our global processing systems. In Australia, we

operate a processing facility that manages a majority of MasterCard-branded transaction volumes for Australia

and New Zealand.

Outside of the United States and a select number of other countries, most intra-country (as opposed to cross-

border) transaction activity conducted with MasterCard, Maestro and Cirrus cards is authorized, cleared and/or

settled by our customers or other processors without the involvement of our central processing systems. We do

not earn transaction processing fees for such activity. Accordingly, we derive a significant portion of our

non-U.S. revenues from processing cross-border transactions. As part of our strategy, we are developing and

promoting domestic processing solutions (such as IPS) for our customers that are designed to capitalize on our

significant investments the MasterCard Worldwide Network.

8