MasterCard 2008 Annual Report Download - page 20

Download and view the complete annual report

Please find page 20 of the 2008 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

subject to revision and amendment by MasterCard’s customers subsequent to the date of its release, which

revisions and amendments may be material.

(2) Local currency growth eliminates the impact of currency fluctuations and represents local market

performance.

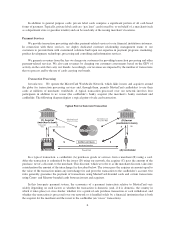

MasterCard Revenue Sources. MasterCard generates revenues by charging transaction processing and

related fees and GDV-based and card-based assessments to both issuers and acquirers. We generally process the

majority of MasterCard-branded domestic transactions in the United States, the United Kingdom, Canada, Brazil

and Australia, and we process substantially all cross-border transactions related to MasterCard, Maestro and

Cirrus-branded cards. The allocation of our revenues varies among issuers and acquirers across our regions.

Typical transaction-based fees include those associated with authorization, clearing and settlement and other

value-added network products. We also charge cross-border and currency conversion fees, and other fees, such as

those associated with acceptance development fees, cardholder services, compliance, penalties, holograms and

user-pay fees for a variety of account and transaction enhancement services and manuals and publications.

Assessments are primarily based on a customer’s GDV for a specific time period and the rates vary depending on

the nature of the transactions that generate GDV and by region. Rebates and incentives, which are paid to

customers and merchants to encourage issuance, usage and acceptance of our cards, are recorded as contra-

revenues in accordance with Accounting Principles Generally Accepted in the United States of America

(“GAAP”). See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—

Revenues” in Item 7 of this Report.

Our gross revenues from transactions, cross border and currency conversion fees, assessments and other

fees, vary by region and are dependent on the nature of the transactions and GDV generated from those

transactions. Pricing is determined based on the combination of transaction characteristics, including whether the

transaction is domestic or cross-border, credit, online debit, offline debit, tiered pricing, geographic region or

country, retail purchase or cash withdrawal. Cross-border transactions generate greater revenue than domestic

transactions due to higher fees for settlement, authorization and switch, and are also subject to cross-border and

currency conversion fees. In addition, higher fees are charged on credit and off-line debit transactions than on

online debit transactions.

On a global scale, we have the ability to process transactions denominated in more than 160 currencies. For

example, we may process a transaction in a merchant’s local currency; however the charge for the transaction

would appear on the cardholder’s statement in the cardholder’s home currency. MasterCard generally uses a

wholesale rate increased by a certain percentage, or a government-mandated rate, to convert transactions in other

currencies into U.S. dollars. Revenues from processing cross-border and currency conversion transactions

fluctuate with cross-border travel. See “Risk Factors—Business Risks—A significant portion of the revenue we

earn outside the United States is generated from cross-border transactions, and a decline in cross-border business

and leisure travel could adversely affect our revenues and profitability” in Item 1A of this Report.

Customer Relationship Management

We are committed to providing our customers with coordinated services through integrated, dedicated

account teams in a manner that allows us to take advantage of our expertise in payment programs, marketing,

product development, technology, processing and consulting and information services. We have implemented an

internal process to manage our relationships with our customers on a global and regional basis to ensure that their

priorities are consistently identified and incorporated into our project, brand, processing, technology and related

strategies.

We also seek to enter into business agreements pursuant to which we offer to customers financial incentives

and other support benefits to issue and promote MasterCard-branded cards. Financial incentives may be based on

GDV or other performance-based criteria, such as issuance of new cards, launch of new programs or execution of

marketing initiatives. We believe that our business agreements with customers have contributed to our strong

volume and revenue growth in recent years.

10