MasterCard 2008 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2008 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

the common stock of MasterCard Incorporated was owned by principal members of MasterCard International.

For more information about our capital structure, voting rights of our common stock, repurchases of our Class A

common stock and conversions of shares of our Class B common stock into shares of our voting Class A

common stock, see Note 14 (Stockholders’ Equity) to the consolidated financial statements included in Item 8 of

this Report.

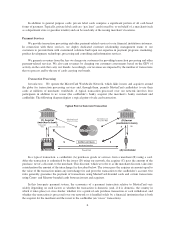

Our Industry

We operate in the global payments industry, which consists of all forms of payment including:

• Paper—cash, personal checks, money orders, official checks, travelers checks and other paper-based

means of transferring value;

• Cards—credit cards, charge cards, debit cards (including Automated Teller Machine (“ATM”) cards),

pre-paid cards and other types of cards; and

• Other Electronic and Emerging—wire transfers, electronic benefits transfers, bill payments, Automated

Clearing House payments and mobile devices, among others.

The most common card-based forms of payment are general purpose cards, which are payment cards

carrying logos that permit widespread usage of the cards within countries, regions or around the world. General

purpose cards have different attributes depending on the type of accounts to which they are linked:

• “pay later” cards, such as credit or charge cards, typically access a credit account that either requires

payment of the full balance within a specified period (a charge card) or that permits the cardholder to

carry a balance in a revolving credit account (a credit card);

• “pay now” cards, such as debit cards, typically access a demand deposit or current account maintained

by the cardholder; and

• “pay before” cards, such as prepaid or electronic purse cards, typically access a pool of value previously

funded.

The primary general purpose card brands include MasterCard, Maestro, Visa®, American Express®, JCB®,

Diners Club®and Discover®. Historically, these brands—including MasterCard—were principally associated

with “pay later” (credit or charge) cards in the United States and other major international markets. Today,

MasterCard (and Visa) cards may be issued in any of the “pay later,” “pay now” or “pay before” categories.

“Pay Now” cards may be further categorized into several sub-segments:

• Signature-based debit cards are cards where the primary means of cardholder validation at the point of

sale (“POS”) is for the cardholder to sign a sales receipt. MasterCard and Visa-branded cards constitute

the majority of signature-based debit cards.

• PIN-based debit cards are cards with which cardholders generally enter a personal identification number

(“PIN”) at a POS terminal for validation. PIN-based debit card brands include our Maestro brand and

Visa’s Electron®and Interlink®brands. The MasterCard brand also functions as a PIN-based debit

brand in the United States.

• Cash access cards, such as our Cirrus-branded cards, are cards which permit cardholders to obtain cash

principally at ATMs by entering a PIN. In addition to Cirrus, the primary global cash access card brand

is Visa’s Plus®brand.

Regional and domestic/local PIN-based debit brands are the primary brands in many countries. In these

markets, issuers have historically relied on the Maestro and Cirrus brands (and other brands) to enable cross-

border transactions, which typically constitute a small portion of the overall number of transactions.

5