MasterCard 2008 Annual Report Download - page 24

Download and view the complete annual report

Please find page 24 of the 2008 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

While MasterCard has capabilities in all prepaid segments, MasterCard’s strategy focuses on three key

segments with respect to prepaid—public sector, corporate and consumer reloadable. MasterCard has

successfully leveraged its global public sector prepaid platform to introduce government benefits programs

around the world. In particular, in 2008, we partnered with government agencies to introduce the largest public

sector benefits prepaid program awarded in the United States and Europe. MasterCard continues to work with

corporate clients on a global basis to realize cost savings and efficiencies from prepaid solutions. In 2008, we had

continued success with our consumer reloadable programs around the world, which provide access to millions of

underserved individuals who are not traditional users of credit or debit cards. Also in 2008, we expanded our

U.S. reload network (referred to as rePower®). As a result of this expansion, consumers using MasterCard and

Maestro prepaid cards enrolled in the network can reload these cards at the point of sale at nearly 50,000

locations. Moreover, in 2008, as discussed above, MasterCard introduced IPS, which is designed to provide

customers with, among other things, a suite of branded debit network and issuer services in support of various

cards, including prepaid cards. In particular, in 2008 MasterCard announced its first customer to take advantage

of the global prepaid transaction processing capability of IPS to include foreign currency and chip-enabled

technology.

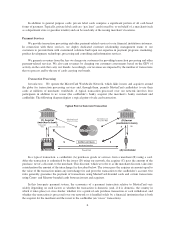

Contactless Payment Solutions

MasterCard PayPass is a “contactless” payment solution that enables consumers simply to tap or wave their

payment card or other payment device, such as a phone, key fob or wristband, on a specially equipped terminal.

PayPass utilizes radio frequency technology to securely transmit payment details wirelessly to the payment card

terminals for processing through our network. Our PayPass program targets purchases of $25 and under and is

designed to help our customers further expand their businesses by capturing a portion of transactions that were

previously cash-based, resulting in increased card activity. PayPass also reduces transaction times, which appeals

to merchants in fast through-put businesses and allows us to expand the number of locations that accept our

cards. PayPass programs expanded in 2008 to include customers and merchants in 28 countries as of

December 31, 2008, an increase from 22 countries as of December 31, 2007. As of December 31, 2008, more

than 50 million PayPass cards and devices were issued globally with acceptance at more than 141,000 merchant

locations worldwide.

Emerging Technologies

MasterCard contributes to innovation in the payments industry through numerous initiatives, including

developments in the areas of electronic commerce, smart cards, mobile commerce, person-to-person payments,

corporate electronic payments, transit and emerging technologies. MasterCard encourages new initiatives in the

area of electronic commerce by researching and developing a range of technologies designed to offer business

opportunities to MasterCard and our customers. MasterCard manages smart card development by working with

our customers to help them replace traditional payment cards relying solely on magnetic stripe technology with

chip-enabled payment cards that offer additional point-of-sale functionality and the ability to provide value-

added services to the cardholder. We are also involved in a number of organizations that facilitate the

development and use of smart cards globally, including a smart cards standards organization with other

participants in the industry that maintains standards and specifications designed to ensure interoperability and

acceptance of chip-based payment applications on a worldwide basis. MasterCard also encourages new initiatives

in the area of mobile commerce and wireless payment development such as contactless payment solutions,

mobile payment and payment-related information services and person-to-person transfers by working with

customers and leading technology companies. In the area of corporate payments between buyers and suppliers,

MasterCard offers a payment processing platform supporting card and electronic funds transfer payments. We

have also developed an innovative transit platform solution that leverages the contactless functionality in cards

and other devices to enable MasterCard acceptance in low value, high volume merchant environments. Finally,

MasterCard is working to develop standards and programs that will allow consumers to conduct their financial

transactions securely using a variety of new point-of-interaction devices.

14