MasterCard 2008 Annual Report Download - page 26

Download and view the complete annual report

Please find page 26 of the 2008 MasterCard annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

Acceptance Initiatives

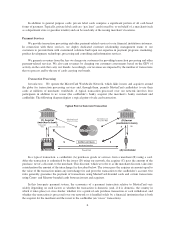

We estimate that, as of December 31, 2008, cards carrying the MasterCard brand were accepted at more

than 28.5 million acceptance locations, including 1.5 million ATMs, as well as other locations where cash may

be obtained. Information on ATM and manual cash access locations is reported by our customers and is partly

based on publicly-available reports of payment industry associations, government agencies and independent

market analysts in Canada and the United States. Cards bearing the Maestro brand mark are accepted at many of

these same locations.

Merchants are an important constituency in the MasterCard payment system and we are working to further

develop our relationships with them. We believe that consolidation in the retail industry is producing a set of

larger merchants with increasingly global scope. These merchants are having a significant impact on all

participants in the global payments industry, including MasterCard. We believe that the growing role of

merchants in the payments system represents both an opportunity and a challenge for MasterCard. Large

merchants are supporting many of the legal, legislative and regulatory challenges to interchange fees that

MasterCard is now defending, since interchange fees represent a significant component of the costs that

merchants pay to accept payment cards. See “Risk Factors—Legal and Regulatory Risks” and “Risk Factors—

Business Risks—Merchants are increasingly focused on the costs of accepting card-based forms of payment,

which may lead to additional litigation and regulatory proceedings and may increase the costs of our incentive

programs, which could materially and adversely affect our profitability” in Item 1A of this Report. We may be

required to increase the amount and scope of incentives that we provide to merchants to encourage the

acceptance and usage of our cards, which may adversely affect our business. Nevertheless, we believe many

opportunities exist to enhance our relationships with merchants and to continue to expand acceptance of our

cards. In 2004, we made available directly to merchants our rules that apply to card acceptance and related

activities, thereby increasing the level of transparency and predictability of our payment system for merchants. In

2006, we published the interchange rates applicable to merchants in the United States and in 2007, we introduced

a cap on interchange fees on fuel purchases at petroleum retailers. In 2008, we published our entire set of

operating rules on our website. As an additional example, we have an advisory group which brings together

merchants, acquirers, issuers and processors twice a year to examine payments innovation at the point of

interaction, and to seek to enhance the experience for merchants and consumers at the point of sale or in an

online shopping environment for a retail sales transaction. Furthermore, we also hold meetings with merchant

advisory groups that have been established in key global markets including the United States, Canada, South

Africa and Australia, and we continue to strengthen our acquirer and merchant sales teams around the world.

We seek to maintain unsurpassed acceptance of MasterCard-branded programs by focusing on three core

initiatives. First, we seek to increase the categories of merchants that accept cards carrying our brands. We are

focused on expanding acceptance in electronic and mobile commerce environments, in fast throughput

businesses, such as fast food restaurants, in transportation and in public sector payments, such as those involving

taxes, fees, fines and tolls, among other categories. Second, we seek to increase the number of payment channels

in which MasterCard programs are accepted, such as by introducing MasterCard acceptance in connection with

bill payment applications. We are working with customers to encourage consumers to make bill payments in a

variety of categories—including rent, utilities and insurance—with their MasterCard-branded cards. Third, we

seek to increase usage of our programs at selected merchants by sponsoring a wide range of promotional

programs on a global basis. We also enter into arrangements with selected merchants under which these

merchants receive performance incentives for the increased use of MasterCard-branded programs or indicate a

preference for MasterCard-branded programs when accepting payments from consumers.

We also support technical initiatives designed to make MasterCard card acceptance more attractive for

specific merchants, such as our Quick Payment Service for fast food restaurants and other merchants where rapid

transactions are required. In addition, MasterCard PayPass appeals to merchants in fast throughput businesses

because it reduces transaction times.

16