Konica Minolta 2015 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2015 Konica Minolta annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

|

|

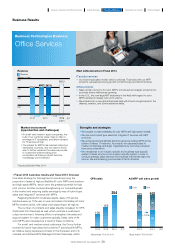

• Growth strategies

Earnings from color MFP print volume is the engine currently

driving growth in this segment (see market forecasts in the figure

below). The goal from Phase 0 through Phase 1 is to achieve

reliable and continued growth by maximizing this color print

volume. Phase 2 will focus on establishing growth independent of

color PV.

The first step in Phase 0 will be promoting genre-top

strategies aimed at putting Konica Minolta at the top of the color

MFP segment. Growth will be driven by the evolution of our current

business, which will involve introducing new A3 color models as

new growth engines and establishing a customer-centric sale style

that enables us to provide solutions for different industries and

business types. We will also strengthen GMA initiatives (business

targeting major accounts with a global presence) for OPS, which

optimize customers’ printing environments.

Phase 1 will focus on further enhancing added value through

efforts including adding MCS to our list of services. These efforts

are aimed at further upgrading the hybrid-type sales system that

incorporates our IT services, which have been enhanced through

M&As conducted in recent years. By managing customers’

business processes themselves and helping to improve and

upgrade these processes while solving problems, we aim to

become a trusted and essential business partner for our

Business Results

Business Technologies Business (Office Services)

customers. These efforts will enable us to differentiate ourselves

from competitors and disengage from price competition.

In Phase 2, we will focus on further merging MFPs and IT

services with a view to the more distant future. The end goal is to

transition MFPs from being considered office automation

equipment to being platforms that serve as information network

hubs for offices in an effort to achieve growth that avoids reliance

on print volume.

Roadmap for growth

Unit shipment trends and forecasts in the office A3 MFP market

Phase 0

OPS/GMA Penetrate hybrid-type

sales

Start providing

MCS globally

Solutions by industry

type and business

category

A3 color

next-generation engine

New-generation

office/platform

Phase 2Phase 1

Maximize color PV Growth not

dependent on PV

Japan

North America

Europe

China

(Thousands of units)

1,000

750

500

250

02012 2013 2014 2015

(forecast)

2016

(forecast)

2017

(forecast)

78%78% 80%

80% 81%

81% 81%81% 82%

82% 82%

82%

(Thousands of units)

1,000

750

500

250

02012 2013 2014 2015

(forecast)

2016

(forecast)

2017

(forecast)

43%43% 45%45% 46%

46% 51%

51% 53%

53% 55%

(Thousands of units)

1,000

750

500

250

02012 2013 2014 2015

(forecast)

2016

(forecast)

2017

(forecast)

59%59% 62%

62%

67%

67% 74%

74% 77%

77% 82%

82%

(Thousands of units)

1,000

750

500

250

02012 2013 2014 2015

(forecast)

2016

(forecast)

2017

(forecast)

9% 11% 12% 13% 15% 16%

(CY

)

(CY) (CY

)

(CY)

Color B/W Color ratio

* Konica Minolta estimate

41

KONICA MINOLTA, INC. Annual Report 2015

Foundation for GrowthBusiness StrategiesGrowth StrategyCompany Overview and Characteristics Financial Report